The Edge Best Call Awards 2019

THE selection of winners this year was tough, with many good calls received from 16 research houses for the 14th edition of The Edge Best Call Awards 2019. Out of 118 nominations received for 84 stocks, we long-listed as many as 33 calls that proved right in 2019, but selected only 12 best calls.

This year, we received the highest number of submissions since 2015, the first year nominations were open to not only the heads of sell-side research outfits but also the general investing public — readers of The Edge, fund managers, private investors and equity analysts themselves for the best ‘buy’ or ‘sell’ call, or even a contrarian ‘hold’ call, that proved correct in 2019.

Last year, 82 nominations were received from 14 research outfits for 67 stocks compared with 90 recommendations for 66 stocks in 2017 and 86 nominations for 75 stocks in 2016. The highest was 139 submissions for 102 stocks in 2015.

This year’s winners include those who rightly stuck their neck out by calling an outright “sell” or “buy” against consensus and were proven right. A number of our winners this year were alone when they first made their “buy” or “sell” call. Like last year, we made some allowances for calls made in 2018 that proved right in 2019.

The awards are our best-effort attempt to recognise good fundamental stock analysis and its importance in making informed investment decisions. They are not meant to influence year-end appraisals or annual bonuses. Feedback is welcome at [email protected].

With that, here are this year’s winners — selected based on submissions and publicly available data — in no particular order. Congratulations to the winners. To the good stock pickers not recognised here, keep up the good work. Here’s wishing everyone a Happy New Year and a better 2020 ahead!

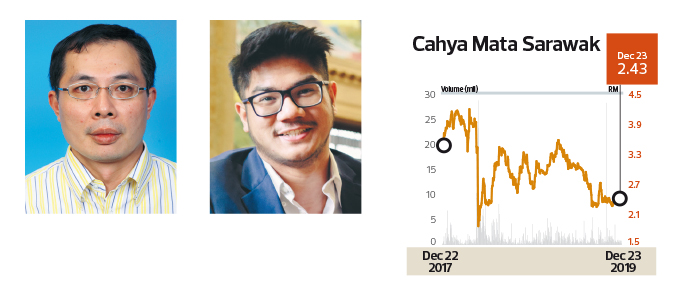

AmInvestment Bank Research head Joshua Ng and analyst Azfar Kamarudin’s call on Cahya Mata Sarawak Bhd

The analysts from AmInvestment Bank stuck out like a sore thumb when they downgraded Cahya Mata Sarawak (CMS) to “underweight” from “buy” with a 36.6% lower target price of RM2.48 on Feb 12 this year. Not only was their valuation 15.6% below CMS’ stock price of RM2.94 at the time, all six other houses tracking the stock were unanimously bullish — the second lowest target price of RM4 implied 36% upside potential, Bloomberg data shows. CMS shares had also recovered 59% from as low as RM1.92 on May 21, 2018, after the 14th general election (GE14).

Given that CMS shares did climb 22% to reach as high as RM3.596 on April 11, the downgrade seemed a tad early. Yet, their warning on potential earnings dampeners arising from the change in competitive landscape post-GE14 probably cautioned some investors to take profit before CMS shares tumbled 37.2% to reach as low as RM2.26 on Sept 17. It was only in end-August that the street went from an overwhelming “buy” to four “hold” calls. A second “sell” recommendation only appeared on Nov 29.

At the time of writing, there were three “buy” calls, valuing CMS at a minimum of RM2.83 a share, even as AmInvestment Bank remained the most bearish, with its RM2.03 target price some 18% below what the stock fetched on the open market. Will they again be vindicated?

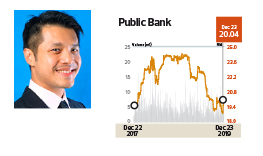

Credit Suisse head of research Danny Goh’s call on Public Bank Bhd

Just a year ago, not many would believe that Public Bank Bhd would actually give up more than RM20 billion in market capitalisation. At least six analysts had target prices that implied a steady ascent past the RM100 billion mark.

Yet Credit Suisse’s Danny Goh audaciously downgraded his recommendation to “underperform” from “neutral” on Feb 21 this year, trimming his target price by RM1 to RM21.80 when Public Bank shares were fetching RM24.24. At least seven other analysts valued the stock above RM26 apiece, with the most bullish as high as RM29.10.

While Goh had in the past underestimated Public Bank’s allure to investors, his downgrade this year was spot-on, with Public Bank shares skidding as much as 22.8% to RM18.84 on Dec 16, from their peak of RM24.41 on Jan 22 this year. It is no surprise, though, that the stock continues to command a premium valuation over its peers despite the decline. At the time of writing, Goh kept his “underperform” call, with a target price of RM19.20.

A notable mention goes to TA Research’s Wong Li Hsia, who downgraded the index heavyweight to “sell” on Oct 16, 2018, trimmed her target price to RM23.40 on Feb 21, 2019, and currently also has a target price of RM19.20.

UOB Kay Hian Research analyst Keith Wee Teck Keong’s call on Bursa Malaysia Bhd

Investors who sold when UOB Kay Hian’s Keith Wee downgraded Bursa Malaysia from “hold” to “sell” on July 23, 2018, would have been spared the heartache of the 21% price slide to as low as RM5.82 on May 28 this year.

While the downgrade was on an unchanged target price of RM6.72, his was the first “sell” call on the exchange operator. Wee only trimmed his target price to RM6.50 on July 31, after cutting earnings forecasts when 2Q2018 earnings came in below expectations owing to lower listing revenue and higher staff costs.

The RM7.39 stock price when he cut his recommendation to “sell” was only 2.7% shy of the RM7.588 reached on Oct 1 this year, before it skidded back to RM6.11 at the time of writing.

A notable mention also goes to TA Research’s Wong Li Hsia, who cut her call to “sell” from “buy” on July 31, 2018, with a target price of RM8.07 when the stock was fetching RM7.36. Theirs were the only two “sell” recommendations at the time, with seven analysts having a “buy” while five others said “hold”.

Wee is now among four analysts with a “sell” call on Bursa. His target price is no longer the most bearish, despite being trimmed to RM5.64 on Oct 30 this year. Nine houses have a “hold” call while three say “buy”.

CIMB Research analyst Walter Aw’s call on Carlsberg Brewery Malaysia Bhd

Carlsberg’s “premiumisation” strategy seems to be working wonders in more ways than one, with its stock price up 46% year to date, after climbing 36% in 2018, 16% in 2017 and 26% in 2016.

The stronger sales volumes, especially in the premium segment (Asahi, 1664 Blanc), which offer better margins relative to mainstream beers, were the reason for the optimistic stance taken by CIMB Research’s Walter Aw. He upgraded Carlsberg from “hold” to “add” with a higher target price of RM24.30 on Feb 14 this year — implying 16.2% upside potential from the RM20.91 it fetched back then.

Of 10 analysts tracking the stock, Aw was one of two to have a “buy” call. The implied returns of 37% from Aw’s recommendation were at least twice as much as those of his peers, according to Bloomberg data. His target price was upgraded to RM31.30 on Nov 27, the most bullish on the street until HSBC started coverage with a “buy” call and RM31.60 target price on Dec 13.

A notable mention goes to Hong Leong Investment Bank Research’s Gan Huan Wen, who already had a “buy” recommendation when Aw upgraded his call but, with hindsight, saw implied returns erode following a downgrade to “hold” on Feb 15.

Macquarie Research analyst Ben Shane Lim’s call on MISC Bhd

There was a sea of “hold” recommendations and one “sell” call when Macquarie Research’s Ben Shane Lim initiated coverage on MISC with an “outperform” call on October 24, 2018.

His argument: Petroleum tanker charter rates had bottomed out and were headed for an inflection point in 2019. A tighter supply of tankers will rerate the Petroliam Nasional Bhd-controlled shipping company. MISC was also among the cheaper FBM KLCI components, having underperformed the benchmark by 25% back then.

“Most importantly, it offers the fourth best dividend yield and is the cheapest FBM KLCI constituent on a price-to-book basis. We believe there is pressure for MISC to sustain dividend payouts given Petronas’ increased payout to the government,” Lim wrote in the initiation note when the stock price was RM5.58, implying 25.4% upside potential versus 10.4% downside risk with a RM5 bear-case valuation.

While Deutsche Bank had a “buy” call earlier, coverage was dropped in December 2018, Bloomberg data shows. By the time a third “buy” call emerged on Nov 2, 2018, MISC shares had gained 14% over the seven market days since Macquarie presented its investment thesis. The shares gained another 29% by Oct 11, 2019, when the number of “buy” calls reached seven, the same number as “hold” calls. Now, the number of “buy” calls has increased to eight and Macquarie’s RM8.80 target price is no longer the most bullish, with at least four houses valuing MISC at over RM9 apiece.

Affin Hwang Research analysts Lester Siew and Chow Wei Nien’s call on QL Resources Bhd

Affin Hwang Research’s “buy” call had been the sole one on QL Resources Bhd since it upgraded its recommendation on Oct 17, 2018 as it turned more upbeat on the company’s sustainable growth drivers, which include the rapidly expanding Family Mart convenience stores.

It was also the only research house to tell investors the stock was worth at least RM8 apiece at a time when the share price was RM6.91. QL shares did rise 7.5% to RM7.43 by Nov 8, 2018, but did not remain above the RM7 mark for long as consensus thought valuations rich.

When Lester Siew raised the target price to RM8.50 on Aug 29 this year, the stock was still hovering around RM6.86. The stock price was hovering at RM7 levels on Dec 2 when Chow Wei Nien joined Siew in maintaining a “buy” call on QL, with a target price of RM8.50. It was only on Dec 19 that the stock closed above the RM8 mark, closing as high as RM8.35 on Dec 20. [Chow is now solely responsible for covering the stock following Siew’s recent resignation.]

While it remains to be seen if the stock will be able to better retain the price gains, the analysts won a spot on our list this year for their steadfast non-consensus conviction that QL shares could fetch over RM8 apiece even with the consensus target price at RM7.01 and peers making seven “hold” calls and six “sell” recommendations.

Credit Suisse analyst Ang Jae Han’s call on Econpile Holdings Bhd

Four other houses were already tracking Econpile when Credit Suisse’s Ang Jae Han started coverage on March 20 with a 74 sen target price, implying a 61% upside potential. Declaring that “the worst appears over with early signs of recovery”, his was the only “buy” recommendation while those earlier than him were split between “hold” and “sell”.

Ang justified the contrarian call and higher valuation for the largest listed piling specialist with its 38% revenue market share and superior profitability relative to its construction peers, the segment’s high barriers to entry and relatively lower payment risks, and Econpile being one of only a handful of pure-play contractors. Moreover, the share price had fallen 63% from its peak and was trading at only 8.3 times FY2020 earnings — which effectively meant zero order-book replenishment had been priced in.

Econpile shares had gained over 75% in less than four months to 82.5 sen by the time he raised his target price to RM1.03 on July 10, making his valuation the highest among peers — one of whom had since mid-June upgraded the stock to “outperform” when the share price was at 72 sen. While Econpile shares had yet to breach RM1 at the time of writing, the stellar gains on the contrarian call earned it a spot on our list this year.

RHB Research analyst Lee Meng Horng’s call on Datasonic Group Bhd and JHM Consolidation Bhd

That Datasonic shares gained some 200% this year made the only two analysts tracking the stock natural contenders for the best call awards. By Oct 23, RHB Research’s Lee Meng Horng had the only “buy” call in town for the IT-based security solutions provider, which in 2010 had clinched the national identification cards (MyKad) contract.

Investors familiar with Datasonic would remember that its share price had languished in the second half of last year, but Lee rightly flagged a turnaround after the company bagged an extension of its preventive maintenance services at the National Registration Department. Those who followed the “buy” call on June 4 this year when Datasonic shares were at 44 sen would have enjoyed capital gains of more than 160% as the stock closed at RM1.30 on Dec 23 — and that does not include the more than 4% yield from the 1.75 sen in dividend paid in May, August and October.

Lee’s 98 sen target price set on Sept 3 was exceeded by late October but he maintained his “buy” call on Dec 2 with a higher target price of RM1.21, which had also been breached as The Edge went to print. It would be interesting to see if the stock has further surprises in store after the magnificent run.

JHM Consolidation’s market capitalisation was only RM898 million when the stock closed at RM1.61 on Dec 18, making it among the smaller capitalised stocks of this year’s 12 best calls. Nonetheless, the stock had gained nearly 90% year to date at the time of writing.

While RHB Research’s Lee Meng Horng was not the analyst who started coverage on the stock in early 2018, he earned a spot on our list for maintaining the sole coverage on the stock, which had a market capitalisation of only RM474 million when it ended 2018 at 83.6 sen.

JHM was Lee’s top pick for the technology sector and in his Feb 28 note titled “The comeback kid”, he wrote that the company was expected to see a strong growth trajectory in FY2019 after a blip in FY2018. This was on the back of higher contributions from its automotive segment coupled with maiden contributions from new business segments, such as life sciences and aerospace.

It was only on Oct 30, 2019, when the stock price was RM1.31, that Nomura Research initiated coverage with a “neutral” recommendation and RM1.51 target price. The price target was revised to RM1.40 on Nov 28.

RHB, meanwhile, further raised its target price for JHM to RM1.60 when reiterating a “buy” call on Dec 3. It remains to be seen if a downgrade is in order or if it still sees substantial upside from current levels.

Hong Leong Investment Bank Research analyst Tan J Young’s call on Frontken Corp Bhd

With Frontken’s share price up over 230% this year, investors who paid attention when Hong Leong Investment Bank Research’s Tan J Young started coverage with a “buy” on Aug 7 last year would have enjoyed outsized capital gains even without the 1.8 sen interim dividend per share paid in February and August this year.

While Tan was not the first to recommend a “buy” on Frontken, his target price of 84 sen on initiation was 33% above the only other peer coverage at the time and had also implied a 33% upside potential from the then prevailing share price. In fact, Frontken had been introduced to clients via a “non-rated” call in July 2017 when the share price was only 33 sen. [Non-rated calls are not counted for the purpose of these awards.]

At the time of writing, Tan is no longer the most bullish on Frontken, having cut his recommendation to “hold” on Nov 6 this year with a RM1.94 target price when the shares were priced at RM1.92. In hindsight, we know the downgrade was a tad premature, given that Frontken’s share price gained another 24% from Nov 6 to close as high as RM2.39 on Dec 17. We acknowledge the 273% total return that investors would have had enjoyed over 15 months, even if they had already locked in their profits.

UOB Kay Hian Research analyst Kong Ho Meng’s call on Uzma Bhd

Making a right call on oil and gas (O&G) stocks has not been easy with the industry in a rough patch since 2015. Analyst Kong Ho Meng’s recommendation was selected as one of the best calls for 2019 mainly because of the timing of his call throughout the year. It was also a non-consensus call.

Over the course of one year, Kong revised his calls three times, each tracking the share price closely. In short, those who followed his recommendation would have benefited from his prescient timing — buy low, sell high.

As Uzma’s share price halved from RM1.40 to around 60 sen in December last year, Kong made a brave call, recommending the O&G stock to clients at a time the world was unsettled by an abrupt fall in oil prices in 4Q2018.

As he had expected, Uzma staged a strong rebound to RM1.07 in mid-March. He then revised his call to “sell” from “buy”. Investors who took profit then would be grinning now as the stock dropped to 58 sen from its peak.

Again, Kong upgraded the counter when it was below 60 sen in August. Uzma then reversed its downward trend, climbing to the year’s high of RM1.11 in October. Since then, he has maintained a “hold” call on the counter to continue riding the improved sentiment in the O&G industry.

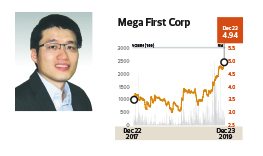

Public Investment Bank Research analyst Chong Hoe Leong’s call on Mega First Corp Bhd

Public Investment Bank Research’s Chong Hoe Leong told clients that Mega First’s share price was worth RM4.74 in January when the stock was trading at the RM3.20 level — an upside of 47%.

Many may opine that a hydropower plant project in Laos, a developing nation, is a high-risk venture with uncertainties on many fronts. Furthermore, a number of other Malaysian companies have had unpleasant overseas experiences, some involving power plant projects.

However, Chong held on to his view for years. He expects the Don Sahong hydropower project to be a money minting machine for Mega First and anticipates that the company will declare a dividend per share of 30 sen once the project commences, with an annual profit of RM200 million to RM260 million generated from Laos.

As the year went on, the market began to notice the hidden value of Mega First. Its share price escalated from around the RM3 level to RM4.93 — a 59% gain for the year.

Investors who took Chong’s advice would have seen their investment returns outperforming the broader market. He initiated coverage on Mega First in 2014 when the stock was trading at about RM1.80.

A notable mention goes to Maybank Investment Bank Research analyst Adrian Wong, who has recommended the stock since June last year.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| BURSA | 7.380 |

| CARLSBG | 18.540 |

| CIMB | 6.530 |

| CMSB | 1.040 |

| DSONIC | 0.435 |

| ECONBHD | 0.470 |

| FRONTKN | 3.890 |

| JHM | 0.565 |

| MFCB | 4.370 |

| MISC | 7.800 |

| PBBANK | 4.150 |

| QL | 6.180 |

| UZMA | 1.220 |

Comments