Giving traditional TV audience the next-generation streaming experience

THE fact that Malaysia’s leading pay-TV operator Astro Malaysia Holdings Bhd has more than 200 channels may be inconsequential to digital natives used to streaming video-on-demand (SVOD). After all, TV channels and fixed programming time slots are irrelevant to the so-called “Netflix generation” and a growing number of people who no longer consume most of their video content via a cable TV subscription (let alone free-to-air broadcast).

Yet, it would seem that old TV-viewing habits are slow to change for a majority of Astro’s 5.7 million subscribers that make up 75% of Malaysian households, and Henry Tan, Astro’s group CEO, is not entirely surprised.

The more advanced (read: premium) users — which include football fans — are going for the 4K Ultra High Definition (UHD) TV experience, which is four times clearer than HD. Yet, many of Astro’s subscribers who have HD channels still watch the normal standard definition (SD) channels, says Tan.

Astro could free up more resources if it did not offer both SD and HD options.

The hurdle of getting more subscribers to upgrade to Astro’s Ultra Box (U-Box) experience — which gives users both the traditional TV channels as well as the option of on-demand video streaming — is relatively greater, despite the potential convenience of an over 50,000 on-demand library, free cloud recordings of multiple broadcasted content that are not on demand as well as the beauty of the broadband connection eliminating the “rain fade” disruptions faced by satellite dishes.

“We can remotely convert at least one million of our existing customers to the U-Box experience [without changing the physical set-up box], but we want to let them make the choice,” he says, adding that it is important that its customers are comfortable with the new U-Box platform, which essentially mirrors the experience on the Astro GO mobile app, which had over 1.4 million monthly active users as at end-July.

Over 100,000 of the U-Box, launched in November 2019 just months before Covid-19 hit, has been installed so far.

Third OTT platform in 2021

Astro is also mulling the introduction of another so-called over-the-top (OTT) mobile application, which cancels out the need for TV channels altogether. The thinking, Tan says, began with Astro’s desire to offer potential customers the option of an Astro subscription without the need to take a physical set-top box — which essentially costs money to both Astro and its customers.

Rather than allowing customers to just sign up for the Astro GO app without taking the TV set-top box, an entirely new OTT is in the works for introduction next year, to provide customers a pure streaming experience such as that offered by video streaming applications like Netflix, Viu (Hong Kong PCCW Media Group’s pan-regional OTT service) and iflix (Malaysian-grown Asian streaming company that was acquired in June by China’s Tencent Holdings Ltd, which also owns WeTV).

Astro’s new yet-to-be named OTT “super content aggregator” app also provides its content partners — which includes major entertainment companies like Warner Media LLC (which owns HBO, Cinemax, Warner TV and Cartoon Network), Disney and NBCUniversal that have launched or are launching their own OTT apps — an alternative platform to sell their content in Malaysia.

While pricing for this potential service has yet to be determined, it is likely that the starting monthly subscription price would be lower than that of Astro GO.

Rather than going head-to-head with streaming rivals, Tan says Astro is essentially offering an alternative channel to market content to its reach of 75% of households in Malaysia. “There will be many OTT options and being a standalone OTT may not be so attractive, so partnerships become important.”

The “win-win” situation would be lower content cost for Astro, and lower marketing as well as customer acquisition and retention costs for its partners. Content that are not exclusive cost lower than those that are.

While Malaysia has a 32.7 million population and one of the largest diaspora of overseas Chinese outside Taiwan, Tan says Malaysia is a “tough” market with “at least four 8% segments” — three Chinese (Cantonese, Mandarin and Hokkien) and one Indian — adding that the number of people who want purely Malay, purely English or purely sports content are “not big”. Yet, it is Astro’s experience catering for this diverse market and years of investment in multiple vernacular content generation that gives the group an edge over newer entrants, he says.

So far, Astro has been extending its long-standing content partnership with Hong Kong’s Television Broadcasts Ltd (TVB), which launched its TVBAnywhere OTT app in Singapore in 2018 but not in Malaysia.

In May and November 2019, Astro collaborated with HBO and iQIYI (Chinese search engine giant Baidu Inc’s video streaming affiliate) to offer its subscribers preferential pricing for their OTT service. Just as Astro has a dedicated iQIYI channel, some of Astro’s content is being shown on the iQIYI platform, a boon for local talent seeking exposure in the huge Chinese market.

In 2017, Astro sold rights to broadcast its animated comedy series Cam & Leon to Amazon, whose Prime service is a rival to Astro’s bread-and-butter paid subscription service. Astro’s other children intellectual property (IP) such as Didi & Friends and Omar & Hana are also being licensed abroad.

Even Netflix has bought content produced by Astro, which includes Astro First original drama series, Demon’s Path; Astro Shaw co-produced Malaysian Box Office hit Hantu Kak Limah and Polis Evo 2; as well as Jason’s Market Trails and Festive Foods, a heritage showcase of cultural festivals in Malaysia. (See “Harnessing the economic benefits of the creative content industry”.)

The thirst for interesting video content and the freedom to choose what to watch, whenever and wherever became even more relevant this year as the Covid-19 pandemic forced and encouraged more people to stay at home.

Netflix, the global streaming leader, added 25.86 million subscribers in the first half of 2020, 93% of the 27.83 million it added in the whole of 2019 (80% of whom are outside the US and Canada) — extraordinary numbers that the company itself warned would normalise after lockdowns ease. Some observers also reckon that most who would subscribe to Netflix or some form of streaming service would be likely to have done so during the lockdown.

Asia-Pacific accounts for 24.2% (6.26 million) of Netflix’s net additions in 1H2020 and 11.7% (22.5 million) of its 192.9 million global subscriber base as at end-June. Netflix does not provide a breakdown for Malaysia, which is among countries it offers lower-priced, mobile-only plans.

Obviously, many could not imagine being locked down without entertainment. Amid the pandemic, total video streaming consumption minutes on mobile soared 30% quarter-on-quarter in the first quarter (1Q2020) across four Southeast Asian (SEA) markets — Indonesia, the Philippines, Singapore and Thailand — and a further 19% q-o-q in 2Q2020 to reach 657 billion, according to a study by Media Partners Asia (MPA).

Google-owned YouTube’s share of the streaming minutes was 84% in 2Q2020, driven by free-to-air content, music and user-generated kids content, MPA said in a statement. Excluding YouTube, total streaming minutes grew 57% to reach 107 billion in 2Q2020 — up 57% from 68 billion in 1Q2020.

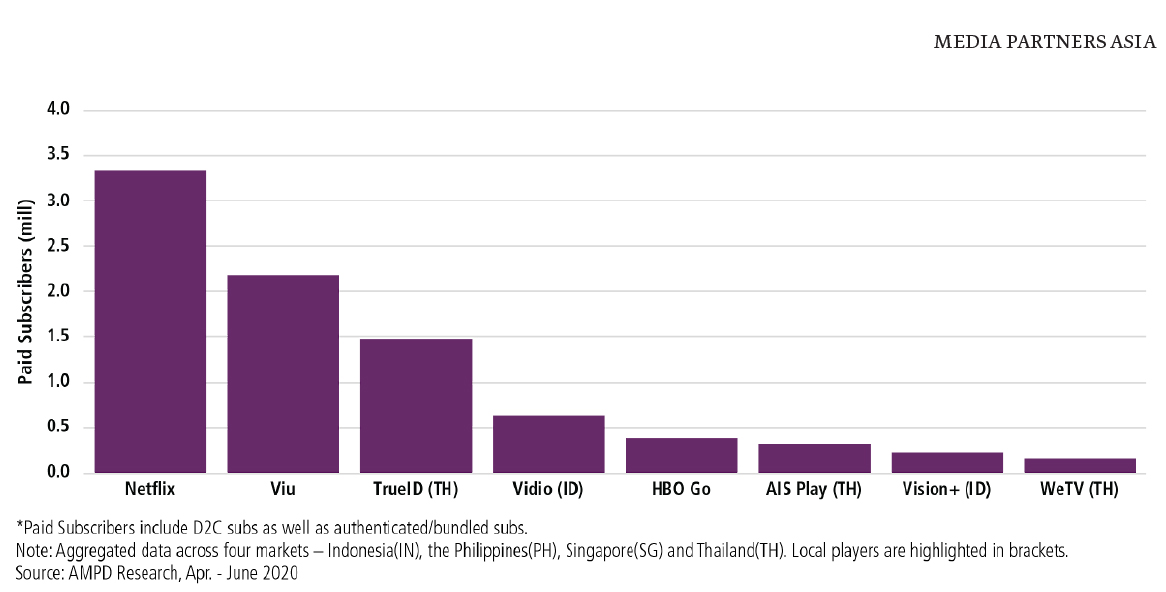

SVOD market leader Netflix had 39% share while leading regional freemium OTT player Viu had 17% share. “Netflix has grown significantly in 1H2020 on the back of mobile pricing and the popularity of its Korean content, International/US originals and local acquisitions. Much of the freemium operator Viu’s success is driven by its Korean day-and-date drama series as well as a handful of local acquisitions and originals in markets such as Thailand,” MPA said in a statement dated Sept 28.

Other notable players with material 20% share in aggregate of total streaming minutes (ex-YouTube) in the four markets “include Indonesia’s Vidio, China’s iQIYI, which is expanding slowly across Southeast Asia, WeTV and Line TV in Thailand and iflix (whose assets were acquired by Tencent, which also owns WeTV, in 2Q),” MPA notes. (See “Enhancing iQIYI’s global appeal with more than just great content”.)

Those four SEA markets (which does not include Malaysia) added three million net SVOD paying subscribers (unadjusted for overlapping subscriptions) in the second quarter this year, bringing the total paying online video or OTT customers to 10 million as at end-June, MPA’s study show.

“Online video consumption continued to soar through the pandemic in Southeast Asia during 1H2020. The growth of premium video services had been significant with a greater scale of consumers paying for online video in large emerging markets such as Indonesia, the Philippines and Thailand. Global, local and regional platforms are rolling out more affordable OTT plans, catering for large mobile broadband universe, while also investing in premium entertainment. It is only the beginning with plenty more work, investment and execution to be done to create sustained, recurring demand for paid legal SVOD services,” MPA executive director Vivek Couto said in the statement.

Bite-sized alternative

Although its third OTT option is still in the works for introduction next year, Astro did not really miss the boat as it already had the NJOI prepaid TV service when the Movement Control Order (MCO) was imposed in Malaysia in mid-March. NJOI charges a one-time installation fee of RM399 for the set-up box with free access to 28 TV channels and 20 radio channels and does not come with a monthly contract commitment. NJOI is also available as an OTT app.

NJOI users who are Hong Kong drama fans can already, for instance, pay RM45 a month to buy the TVB pack of seven channels instead of paying between RM61.32 (New Emperor) and RM204.95 (Super Pack Plus 3 + New Emperor + Star Chinese Channel) per month for more channels that include larger bundled content from China, Hong Kong, Taiwan and Singapore as well as sports and Korean channels.

Similarly, Astro subscribers can subscribe to the HBO Go app at a lower price of RM25 per month. NJOI is offering HBO HD and Cinemax at RM30 per month while non-Astro subscribers can just subscribe to HBO Go standalone directly at RM34.90 per month.

There are more than 60 relatively bite-sized NJOI prepaid individual and mini channel bundles that do not require more than a month’s commitment, with pricing ranging from RM7 to RM50 per month, according to NJOI’s webpage.

Tan declines to disclose the average revenue per user (ARPU) for NJOI except that it is still “small” relative to its premium Astro service but is “steadily growing”.

He also says the first quarter of this year is not the first time that the NJOI user base overtook the Astro subscriber base, but declined to elaborate as the information is not public.

The addition of a third OTT service from next year would complicate third-party or independent estimates of Astro’s original pay-TV subscriber base, without more disclosure on NJOI’s ARPU or user base. Astro no longer discloses the split between its NJOI and regular pay-TV customers since its financial year ended Jan 31, 2017 (FY2017).

Despite the impact of the rebate of RM20 per month to its Sports Pack customers in June and July this year, owing to the lack of live sports content during the pandemic, Astro’s residential pay-TV ARPU was RM98 per month as at the second quarter ended July 31, 2020 (2QFY2021), slipping from RM99.10 and RM100.40 per month in 1QFY2021 and 4QFY2020 respectively. Assuming zero revenue from NJOI, there would be about 2.8 million premium pay-TV Astro customers and 2.9 million NJOI customers as at end-July, our back-of-the-envelope calculations show.

Astro has spent RM1.4 billion to RM1.8 billion (US$336 million to US$432 million) per year or about a-third of its TV revenue on content in recent years, more so for years with more sporting events.

Astro’s content costs had dropped in the first half of this year, coming in at only RM589 million compared with RM718 million in the first half of last year. This was attributed to content renegotiations as well as a pause in local content production and live sports due to social distancing rules and movement restrictions to curb the pandemic. Live sports, another area of strength for Astro, has resumed.

There is no concern of Astro running out of content for “at least one to two years”, Tan says, adding that the pandemic has also drawn more local filmmakers to explore releasing their work on the Astro First platform. (See “Astro offers local filmmakers alternative monetisation platform”.)

What has yet to be fully monetised is Astro’s reach and relationship with the premium and middle-class professional household and user base that is targeted by advertisers and sellers of products and services. Astro, Tan says, will continue to find ways to deepen its relationship with customers to retain them as pay-TV subscribers as well as upsell more relevant products that better data analytics would help show.

There is some success so far on low hanging fruits, such as negotiating a good rate to upsell HD TV sets to customers who have HD channels. Avid watchers of Astro’s Tutor TV programmes, for instance, might also be interested in other types of educational and learning courses.

Helped by the addition of groceries and other basic necessities during the MCO, Astro’s TV home-shopping platform Go Shop made RM9.8 million in the second quarter, up from RM1.8 million in the first quarter, staging a significant turnaround after pre-tax losses totalling over RM79.3 million in the previous five financial years (FY2016-FY2020). The home-shopping segment — which started in 2014 in partnership with South Korea’s leading multimedia retailer GS Home Shopping Inc — booked a RM15.8 million pre-tax loss in FY2020.

It was also during the pandemic, when live sports were halted, that Astro utilised its reach to secure interviews with football players like Gary Neville to keep its subscribers engaged. These online events saw “about 100,000 to 150,000 subscribers” participating each time, Astro’s head of sports CK Lee told reporters in early September.

Yet, the battle to retain subscribers for the long haul is far from won. Tan admits as much, reiterating how piracy remains a huge threat to the small local content creators, not just established corporations like Astro. He is optimistic, though, that the plight of the creative content creation industry — which is suffering due to Covid-19 — would be heard by policymakers, especially with renewed realisation of the economic benefits the country stands to gain if the industry does well.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments