Cover Story: Questions over FELDA’s plans for FGV

LAST Friday, market talk had it that the Federal Land Development Authority (FELDA) had secured the requisite funding to buy the stakes held by Kumpulan Wang Persaraan (Diperbadankan), or KWAP, and Urusharta Jamaah Sdn Bhd (UJSB) in FGV Holdings Bhd.

The funding included the amount needed to buy up all the shares not under FELDA and parties acting in concert with it. Details of the funding, however, were unavailable but one source familiar with the matter said that FELDA obtained the loan as it had assets in the form of land.

“I would think it’s a club deal (a consortium of banks), no single financial institution would take up such a loan … or it (the privatisation) could be government funded,” one source says.

However, it is not clear if the situation has changed since last Friday, as things have been pretty fluid at FELDA.

For instance, FGV, via a land lease agreement (LLA) with FELDA, controls and operates 350,733ha of plantations owned by FELDA, for a 99-year tenure starting from Nov 1, 2011. FGV on its own has 88,497ha of plantation land and 68 palm oil mills, parked under FGV Palm Industries Sdn Bhd.

Until recently, FELDA’s restructuring plan was hinged on the termination of the LLA with FGV, which would give FELDA back its plantations but also incur compensation costs, which could total RM5 billion to RM6 billion, depending on the price tag of FGV’s palm oil mills, which FELDA said it was interested in.

Now, the plans seem to have taken a drastic change, with no indication of FELDA’s direction.

A vague one pager on the government agency’s website, called FELDA’s New Model, Towards a Brighter Future, has 10 tenets, which include terminating the LLA with FGV, and more general ones such as changing the FELDA settlers’ mindset, a new oversight committee, strengthening management and settling the settlers’ debts.

How seriously these tenets will be adhered to is anyone’s guess.

To recap, early last week, FELDA, which has a stake of 33.66% in FGV, sought to acquire UJSB’s 7.78% stake for RM368.8 million and KWAP’s 6.1% holding for RM289.2 million, triggering a mandatory takeover offer.

FELDA, in a statement issued by Maybank Investment Bank Bhd, had said that with persons acting in concert, the government agency had amassed more than 50% of FGV’s shareholding. But who is partnering with FELDA is not known, and while most fingers point to Koperasi Permodalan Felda Malaysia Bhd — an entity which aims to assist Felda settlers — there are many other government-linked entities with shareholdings in FGV that would work with FELDA.

With more than 50%, FELDA is making a mandatory takeover offer for the remainder shares it does not own at RM1.30 apiece.

But it is not clear if FELDA intends to maintain FGV’s listing.

FELDA declined to answer emailed questions sent to it last week, while chairman Datuk Seri Idris Jusoh could not be contacted for comment.

Many are curious as to why KWAP and UJSB are accepting FELDA’s offer of RM1.30 per share, as it could be deemed on the low side, depending on how you view the transaction.

Minority Shareholders Watch Group’s (MSWG) CEO Devanesan Evanson says of the RM1.30 offer: “I suppose the question is whether the offer is reasonable and fair. The share price was RM1.27 before the offer was made. As such, there was a slight premium. The offer price of RM1.30 is well above the net asset per share of RM1.13 as at end-September.” (See “MSWG’s take on FELDA’s offer for FGV” on Page 62.)

It is also noteworthy that since the offer by FELDA, FGV’s share price has dipped, closing at RM1.19 last Thursday, translating into a market capitalisation of RM4.34 billion.

At RM1.30 per share, FELDA would have to fork out RM3.15 billion for the 66.34% it does not own in FGV.

A senior executive from FGV, meanwhile, deemed the RM1.30 offer as low. “I would have thought they (FELDA) would offer at least RM1.59 per share (FGV’s 52-week high, attained in early January this year),” he says.

Why are KWAP and UJSB accepting FELDA’s offer?

UJSB, owned by the Ministry of Finance (MoF), took over assets from the troubled and cash-strapped pilgrim fund, Lembaga Tabung Haji, in 2018. The assets included stakes in 106 listed companies, one unlisted plantation counter, and 29 properties, including four hotels, and a plot of land at Tun Razak Exchange. UJSB had paid RM19.9 billion for the assets, which had a net book value of RM10 billion. UJSB also issued sukuk to the tune of RM19.6 billion to facilitate the acquisition.

UJSB’s 10-year mandate is to not only protect the value of the assets it has, but to create and grow the value of its portfolio, it had told The Edge in the past.

News reports have it that UJSB paid RM1.31 billion, or a 545% premium, for the 283.71 million shares or 7.78% stake in FGV it inherited from Lembaga Tabung Haji. The shares had a market value of RM202.85 million as at end-2018, when UJSB took over the assets of the pilgrim fund.

FELDA’s offer of RM1.30 amounts to RM368.8 million in cash.

In an email reply to The Edge, UJSB says, “With reference to UJSB’s disposal of its stake in FGV to FELDA, we would like to state that decisions such as this fall within the ordinary course of business of an asset management company.

“UJSB has executed a conditional share purchase agreement with FELDA which brings us into a contractual arrangement with them.

“From our perspective and internal assessment, we feel that the price that FELDA has offered is attractive. The proceeds raised will subsequently enable us to redeploy/reinvest capital and improve our returns. This forms part of UJSB’s mandate to manage our assets responsibly and improve the overall performance of our portfolio.”

KWAP, meanwhile, in response to questions from The Edge, says, “Given that KWAP is bound by a confidentiality agreement with FELDA subject to the conditional share purchase agreement, we are unable to provide further details in relation to this matter.

“However, if we may add, KWAP views achieving sustainable fund growth to be of utmost importance as it enables us to effectively manage our investments more diligently in the long term for the benefit of our stakeholders.”

KWAP first surfaced as a substantial shareholder in early July 2012 with 193.49 million shares or 5.3% equity interest, after accumulating shares on the open market.

Since then, KWAP has actively traded FGV’s stock, making it difficult to gauge its holding costs for its shareholding in FGV.

Nevertheless, from end-June 2012 — FGV’s stock hit an intra-day high of RM5.46 on its debut — to end-December the same year, its share price averaged RM4.08. Since its listing at end-June 2012, FGV’s stock has averaged RM2.15, which means the RM1.30 offer is a 39.53% discount to the average trading price of FGV over the last eight years.

What an analyst says

In a report released last week, CGS-CIMB’s plantation analyst Ivy Ng says, “The offer price of RM1.30 is at a 3% discount to our target price and only a 2% premium to FGV’s last closing price.

“However, this is probably a better option for FGV shareholders than having FGV’s share price being negatively impacted by concerns over the termination of the LLA or a dispute over compensation terms.

“The downside is that most long-term shareholders of FGV will have to realise a significant loss from FGV’s IPO price of RM4.55 per share and will not be able to enjoy the upside of higher fresh fruit bunch yields from its replanted estates or stronger crude palm oil (CPO) prices.

“On balance, the deal is probably more favourable to FELDA than FGV’s shareholders. However, the takeover offer provides an avenue for large FGV shareholders to exit their position.”

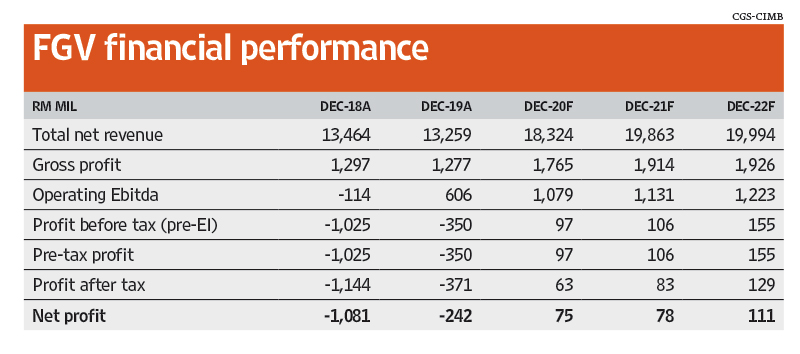

She sees FGV chalking up a net profit of RM75 million from RM18.32 billion in revenue for the financial year ending December 2020. She estimates that in FY2021, FGV will rake in a net profit of RM78 million from RM19.86 billion in turnover.

She has a target price of RM1.30 on FGV’s stock, down from RM1.34 previously.

For its nine months ended September, FGV registered a net profit of RM15.09 million from RM10.07 billion in sales. For the third quarter of FY2020, FGV posted a net profit of RM136.89 million from RM3.99 billion in revenue.

As at end-September this year, FGV had deposits, cash and bank balances of RM1.73 billion and short- and long-term debt of RM2.77 billion and RM854.1 million respectively. Meanwhile, accumulated losses totalled RM2.9 billion.

FGV’s net cash from operating activities as at end-September this year was RM1.29 billion.

On its prospects, FGV says, “The group expects CPO prices to remain strong until the end of the year. Improvements in yield achieved to date, however, are unlikely to be sustained due to weather uncertainties and the partial lockdown in Sabah. The board expects the overall business climate to remain uncertain and volatile.” This was for the financial period ended September.

Since early May this year, CPO futures have gained more than 70% to trade at RM3,347 per tonne last Friday. Analysts who cover CPO, however, peg their forecasts for 2021 at lower levels.

Hong Leong Investment Bank, for instance, has a CPO price assumption of RM2,700 per tonne for 2020-2022. In a report last week, the bank-backed research house says, “We believe CPO price will remain elevated (at above RM3,000 per tonne) until 1Q21. Beyond 1Q21, we anticipate CPO price to soften, on the back of better supply outlook for major edible oils (based on the assumptions that labour shortage in Malaysia will gradually ease from 2021 onwards and La Niña does not strengthen further), which will in turn result in more balanced demand-supply dynamics.”

Kenanga Investment bank, meanwhile, has an unchanged 2021 price forecast of RM2,600 per tonne.

The many blunders at FELDA and FGV

FELDA has announced that it is looking to raise RM9.9 billion in government-guaranteed sukuk but this is mainly to address RM10.6 billion in existing debt. There is little explanation as to what happened to the RM5.7 billion made from the listing of FGV in 2012, and the RM2.5 billion FGV says it has paid out to FELDA from 2012 to 2019 as part of the LLA, which requires it to pay RM248 million and 15% of the operating profit from LLA land.

The new management is led by politician Idris, who holds the chairman’s post, but will he be able to help FELDA emerge from the current quagmire?

FGV’s management, led by chairman Datuk Azhar Abdul Hamid and CEO Datuk Haris Haris Fadzilah Hassan, seem to have got their act together, but coming from a weak base, things have been difficult.

At the time of its listing, FGV’s plantation profile was not very good. FGV’s prospectus for its IPO in 2012 indicated that 36% of its plantations were between 21 and 25 years and 16.9% were over 25 years, or put another way, 52.9% of FGV’s plantations were regarded as old eight years ago.

Today, however, old trees are 32% of FGV’s profile as a result of a replanting exercise of 15,000ha year, which cost about RM300 million annually.

Acquisitions of companies post-IPO were to reduce the age profile of FGV’s trees, but this did not take place. FGV utilised a chunk of its RM4.9 billion proceeds from the issuance of shares to acquire plantation assets, some of which courted controversy.

In July 2013, a year after its flotation, FGV announced its plan to acquire Sabah-based Pontian United Plantations Bhd for RM1.2 billion, which was not met with much fanfare from the analyst fraternity. Pontian had about 16,000ha of oil palm plantation, among others assets.

Back then, BIMB Securities said FGV was paying too much for the plantation company and was “sceptical” about the acquisition, as the earnings contribution to FGV would be minimal.

FGV had also informed Bursa Malaysia that it could not ascertain key information pertaining to the plantation land held by Pontian group, including identification of real estate, age and profile of plantation, mill capacity and unplanted land area. Nevertheless, the acquisition was concluded in October the same year.

In June 2015, FGV announced the acquisition of four plantation companies and a parcel of oil palm land in Sabah measuring 836.1ha from Golden Land Bhd for RM655 million in cash. While this acquisition did not excite, it was not disparaged.

What raised many an eyebrow was the acquisition of Asian Plantations Ltd, which FGV concluded at end-October 2014 for RM628 million. It also assumed RM388 million in liabilities, meaning that it expended a little more than RM1 billion for the acquisition.

To recap, FGV acquired Singapore-incorporated but UK’s Alternative Investment Market listed Asian Plantations after a voluntary conditional cash offer of £2.20 per share, which was a premium of 294.7% over its net asset value per share as at Dec 31, 2013.

Asian Plantations owns 24,622ha of oil palm plantations through its five wholly-owned estates, namely Incosetia Estate, Grand Performance Estate, Fortune Estate, Kronos Estate and BJ Corp Estate, all located around Miri and Bintulu, in Sarawak.

However, as much as 40% of its 24,000ha land could not be cultivated, as about 7,300ha were unplantable and close to 2,600ha were encumbered with Native Customary Rights claims.

Among the major shareholders of Asian Plantations when FGV took over was Keresa Plantations Sdn Bhd, the vehicle of Tan Sri Leonard Linggi Jugah, which had 24.9% equity interest in the company. Other shareholders were Dennis Nicholas Melka and Graeme Iain Brown, who, with Linngi, controlled close to 60% of Asian Plantations.

The dispute over the acquisition is in court now.

It is also worth noting that FELDA is involved in arbitration proceedings from its acquisition of a 37% stake in Indonesia’s PT Eagle High Plantations TBK from the Rajawali group, the vehicle of businessman Tan Sri Peter Sondakh, for US$505.4 million (RM2.26 billion then). The acquisition price was 95.86% higher than the market value of the company’s shares.

The dispute between FELDA and Indonesia’s Rajawali group stems from the former’s decision to sell back its shares in Eagle High Plantations, exercising a put and call option which was part of the agreement, and importantly, at the original price of US$505.4 million. FELDA had filed a notice in April last year to sell back its 37% in Eagle High to the Rajawali group, which contested the exercise. Arbitration is ongoing at the Singapore International Arbitration Centre.

With all these issues occupying its time and attention, will FELDA be able to focus on running FGV well?

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments