The Edge | Klang Valley High-Rise Residential Property Monitor (3Q2020): Slight improvement with visible market activity, sturdy interest

The overall residential property market appears to have improved slightly in 3Q2020, says Savills Malaysia director of research and consultancy Amy Wong in presenting The Edge/Savills Klang Valley High-Rise Residential Property Monitor for 3Q2020.

“During the quarter under review, the total amount of loan applications and approvals for the purchase of residential property in the country have doubled compared with the previous quarter,” she says. The total amount of loan applications increased to RM88.21 billion in 3Q2020 from RM42.55 billion in 2Q2020, whereas the total amount of loan approvals increased to RM29.74 billion from RM12.16 billion in the same period. Wong says this signals that interest in property buying remains sturdy in the market.

Further, the Recovery Movement Control Order (RMCO) announced in June, which has since been extended, saw containment measures lifted and most businesses allowed to resume. “For the property sector, property sales galleries reopened while adhering to SOPs (standard operating procedures), whereas for the construction sector, sitework progress resumed and developers sought for an extension of time for ongoing housing projects to avoid liquidated ascertained damages due to the prolonged construction period affected by the MCO in March.

“Borders, however, remained closed during the RMCO, causing a strain on sales for some ongoing luxury residential projects that target foreign buyers,” says Wong.

Although Bank Negara Malaysia was expected to make a final cut of 25 basis points (bps) to its overnight policy rate (OPR) last September due to the anticipation of relentless economic conditions resulting from the virus outbreak, the OPR was maintained at 1.75% as concluded in the monetary policy committee’s final meeting for 2020 — a result of the easing of various containment measures as well as strong policy support introduced by the government, says Wong.

“The total reduction of 125bps in the OPR — adjusted four times in 2020 — will continue to provide stimulus to the economic recovery. The historically low OPR at 1.75% and perks offered by developers continue to be the main driving factor for residential property demand. Hence, the residential property market was seen to be the better-performing property sector in the third quarter, after the industrial property sector,” she adds.

“Although the capital values of residential properties, particularly high-rise ones, were under pressure from the economic slowdown, market activity remained — though not as active as pre-MCO levels. During the review period, some new residential projects were launched in Kuala Lumpur and Selangor. This shows that there is still confidence among property developers for the residential property to perform despite the economic slowdown.”

Meanwhile, the latest Budget 2021 announcement has further brought stimulus to the property market, says Wong. Residential properties priced RM500,000 and below will be entitled to stamp duty waiver on the instrument of transfer and loan agreement from Jan 1, 2021, to Dec 31, 2025, for first-time homebuyers and existing collaborations with financial institutions for the Rent-To-Own housing scheme involving a total of 5,000 PR1MA housing units worth RM1 billion under the budget will be further extended to 2022. Also, notable transport infrastructure developments such as the Mass Rapid Transit (MRT) Line 3 in the Klang Valley and the Johor Baru-Singapore Rapid Transit System (RTS) have been confirmed to proceed, says Wong.

Following the latest surge in Covid-19 cases in the country, the government has reinstated the MCO in the states of Penang, Selangor, Melaka, Johor and Sabah as well as the federal territories of KL, Putrajaya and Labuan starting Jan 13. Meanwhile, a state of emergency has been declared by the palace on Jan 12 to control the spread of the virus until Aug 1, which may be ended earlier if the number of daily positive Covid-19 cases can be brought under control. “Given such uncertainties brought about by the health crisis, we will be expected to adapt to the new norms. We also anticipate that such uncertainties will cause the property market’s performance to remain tight,” says Wong.

During the quarter under review, the residential property market in prime areas of KL — specifically KLCC, Bangsar and Mont’Kiara — saw a further drop in capital values, a continued downtrend since several quarters ago. According to Wong, the average capital values in these prime areas adjusted down by about 1% compared with 2Q2020, following the slack in the market. “Although the average asking prices for the selected 2-bedroom units sampled have increased in certain areas, the capital values are unlikely to also increase at the moment.”

In Selangor, Tropicana Temokin Sdn Bhd launched Tropicana Miyu, which will add 271 condominium units to the Petaling Jaya market. In the secondary market, the number of transactional activities turned positive, says Wong. “Through our inquiries with local agents, the permission granted to conduct sales and purchase for properties during the RMCO also saw increased property viewings. However, based on our observation, high-rise residential schemes in Subang Jaya, Bandar Sunway, Petaling Jaya and Shah Alam saw a continued decrease in asking prices in 3Q2020. Similarly, the capital values of most of the selected schemes saw an expected reduction amid the Covid-19 outbreak,” she adds.

Soft capital growth in KL

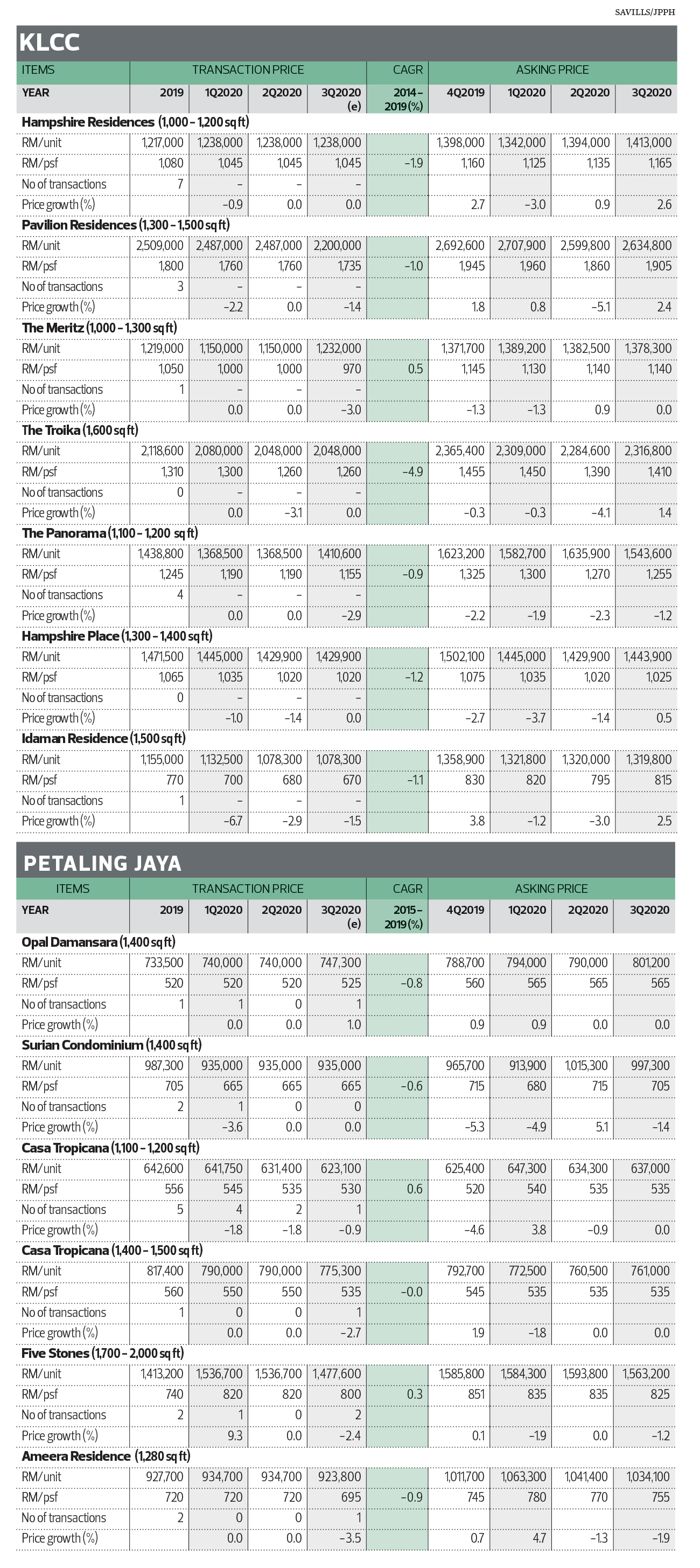

During the quarter under review, the high-rise residential property market in KLCC was the most affected compared with Bangsar and Mont’Kiara, especially in terms of the primary market. “As sales of high-rise residential properties rely heavily on foreign buyers, the border closures have deterred the sales of ongoing projects,” says Wong.

The average sales rate for the high-rise residential projects in KLCC increased 2% during the quarter compared with 1Q2020, which was prior to the nationwide lockdown and closure of the country’s borders. “Although certain high-rise residential projects that were marketed overseas managed to obtain some bookings, sales were not as bustling as before,” she notes.

The average capital value in KLCC dipped marginally by 1.3% compared with the previous quarter, from RM1,135 psf in 2Q2020 to RM1,120 psf in 3Q2020. On a year-on-year (y-o-y) basis, the average capital value of the 2-bedroom units sampled had decreased 4%. Conversely, the average asking price increased 1.2% during the period under review to RM1,245 psf from RM1,230 psf in 2Q2020.

In Bangsar, the selected 2-bedroom units sampled saw stable capital values, with the average value down less than 1% quarter on quarter (q-o-q) to RM905 psf, from RM915 psf in 2Q2020. On a y-o-y basis, the average capital value was 2% lower, compared with 3Q2019.

In contrast, the average asking price for similar properties was higher during the quarter, at RM1,005 psf from RM980 in 2Q2020. This translates into a 2.1% increase q-o-q.

In Mont’Kiara, the capital values of high-rise residential properties during the period under review generally remained soft. The average capital value of the selected 2-bedroom units sampled was about 1% lower than the previous quarter, at RM615 psf from RM620 psf in 2Q2020.

On a y-o-y basis, Mont’Kiara’s average capital value dropped about 4%. The average asking price of the selected units has been adjusted downwards by about 2.5% q-o-q to RM690 psf, from RM705 psf in 2Q2020.

Despite the current economic conditions, Mont’Kiara saw a newly launched high-rise residential project, Allevia, by UEM Sunrise. The project, with selling prices above RM900 psf, will add another 294 units to the high-rise residential supply in the area.

According to Wong, the developer is taking advantage of the Home Ownership Campaign 2020, which offers an opportunity for homebuyers and investors to purchase properties at a low-entry cost. “The project is understood to have received overwhelming interest from the market, with hundreds of inquiries reported in just one week upon its unveiling,” she notes.

Values relatively stable in Selangor, with more activity in PJ

In Subang Jaya, the average capital value of the selected 2- and 3-bedroom units sampled was relatively stable during the period under review, at RM538 psf compared with RM540 psf in 2Q2020.

The average transacted price for Olives Residence’s 3-bedroom units saw a 3.1% drop from RM485 psf in 2Q2020 to RM470 psf in 3Q2020. Wong says this is also due to the property’s lowered asking price from RM530 psf to RM520 psf, or -1.9%.

Conversely, Subang Avenue recorded a 1.8% q-o-q increase in the transacted price, from RM550 psf in 2Q2020 to RM560 psf in 3Q2020. Such a marginal increase, however, is not in tandem with the property’s decreased transacted value from RM635 psf in 3Q2019 to RM560 psf in 3Q2020, or an 11.8% drop y-o-y, says Wong.

Similar to Subang Jaya, Bandar Sunway’s average capital value of the 2- and 3-bedroom units sampled remained stable at RM597 psf compared with the preceding quarter. Wong observes that homeowners in general have toned down their asking prices, from RM625 psf in 2Q2020 to RM613 psf in 3Q2020, a 1.9% drop q-o-q.

In 3Q2020, the average transacted price at Nautica Lake Suites and Sunway Lagoon View was stable compared with pre-Covid days, at RM530 psf and RM550 psf respectively.

At Nadayu 28, the average transacted price decreased 0.6% y-o-y, from RM785 psf in 3Q2019 to RM780 psf in 3Q2020. At LaCosta, it decreased 2.2% from RM675 psf to RM660 psf during the period.

Petaling Jaya saw more transactional activity during the quarter compared with other areas in Selangor. The average transacted price for the selected 2- and 3-bedroom units sampled exhibited greater fluctuation when compared y-o-y, says Wong. For instance, Surian Condominium recorded a 6.3% drop in capital value, from an average transacted price of RM710 psf in 3Q2019 to RM665 psf in 3Q2020.

Casa Tropicana’s 2-bedroom units, ranging from 1,100 to 1,200 sq ft, experienced a drop of 5.4% y-o-y, from RM560 psf to RM530 psf. The transacted price of its 3-bedroom units, with built-ups of between 1,400 and 1,500 sq ft, decreased 4.5% y-o-y to RM535 psf from RM560 psf.

At Five Stones in central Petaling Jaya, the average transacted value appreciated 8.8% y-o-y, from RM735 psf in 3Q2019 to RM800 psf in 3Q2020. However, the average transacted price saw a marginal drop of 2.4% q-o-q from RM820 psf in 2Q2020.

A positive price movement amid the pandemic was recorded at Opal Damansara, where the average transacted price increased 1% on both a y-o-y and q-o-q basis, from RM520 psf to RM525 psf.

In general, the average capital value of the selected units in Petaling Jaya stood at RM625 psf. This was due to asking prices being 0.9% lower to RM653 psf during the quarter from RM659 psf in 2Q2020, says Wong.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments