Higher CPO prices mitigate lower FFB yields for Kretam

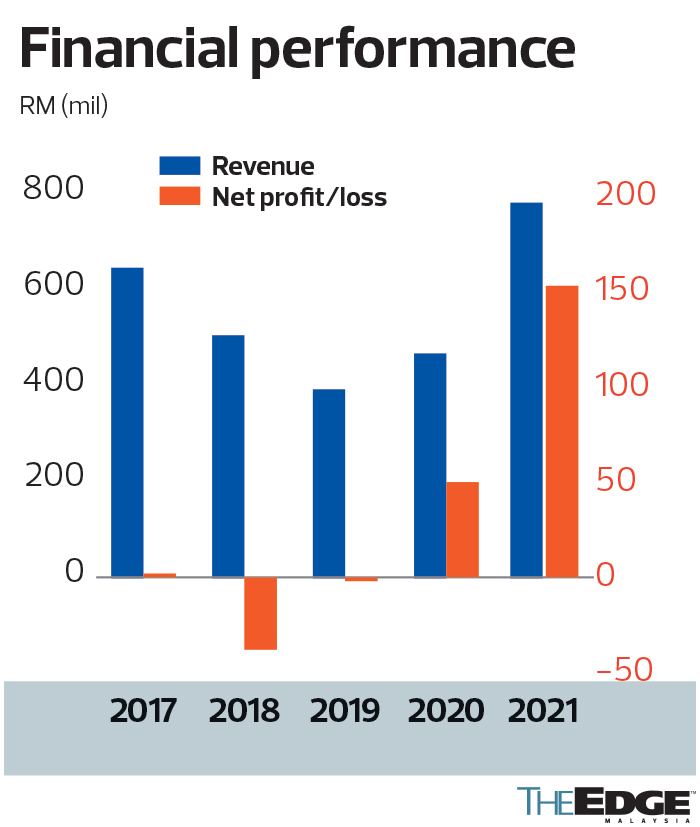

KRETAM Holdings Bhd reported a record profit of RM153.3 million in the financial year ended Dec 31, 2021 (FY2021), but the Sabah-based plantation group refuses to get overly excited.

Executive director and chief operating officer Gary Lim Tshung Yu acknowledges that although the company’s earnings performance was lifted by higher crude palm oil (CPO) prices, its fresh fruit bunch (FFB) yield has actually been on a downward trend.

According to him, Kretam’s production has dropped about 7% from pre-Covid levels due to factors such as seasonal weather conditions, travel restrictions and labour shortage. “Frankly, last year was a very bad one for us in terms of FFB yield, which was only about 17 tonnes per hectare. Fortunately, the higher CPO prices mitigated these negative factors,” he tells The Edge in an interview.

For perspective, Kretam’s FFB yield was in the range of 18.83 to 18.92 tonnes per hectare between FY2017 and FY2019, before declining to 17.61 tonnes per hectare in FY2020 and 17.71 tonnes per hectare in FY2021.

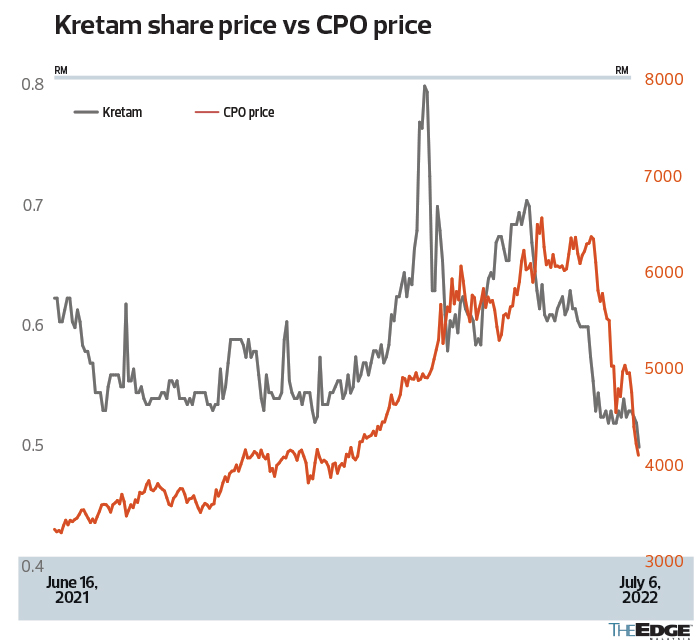

Over the past two years, CPO prices had climbed about 70%, from RM3,041 per tonne at end-2019 to RM5,159 per tonne at end-2021. Quite astonishingly, it hit the RM8,000 per tonne mark for the first time on March 1 this year before sliding to the RM5,000 per tonne level recently.

“Definitely, Kretam is riding the commodity boom and we are benefiting from the rising CPO prices. Our earnings speak for itself. But the fact is, we are still facing a difficult labour situation. Although travel restrictions have been lifted, we are still facing difficulties in bringing in foreign labour,” says Lim.

Kretam currently employs about 4,000 workers, of whom 3,200 are foreign workers. About 76% of the group’s foreign workers are from Indonesia, while the remaining 24% are from the Philippines.

Lim acknowledges that the labour shortage will continue to affect Kretam due to the loss of income from unharvested fruit. “Although we are not heavily impacted, we are still short of workers on the field. The introduction of the minimum wage for the plantation sector is actually a double-edged sword. On one hand, such an increase will raise production costs by 20% to 25%. But on the other hand, we are hopeful that such an increase will attract more foreign workers,” he explains.

To mitigate the impact of the labour shortage, Kretam has been trying to mechanise its operations. For instance, the group is working on mechanising its evacuation process.

“As a local plantation company, there is only so much we can do. We try to offer better wages and benefits to our workers, build better houses for them, provide them with better welfare,” says Lim, adding that the weaker ringgit is another issue because foreign workers will be less willing to work in Malaysia.

“And bear in mind that most foreign workers at plantation companies are from Indonesia, the largest CPO producer in the world. We can’t really stop them if they want to return to their home country,” he observes.

Lim, 30, was appointed to the board in December 2018. He is the son of Datuk Freddy Lim Nyuk Sang, CEO and controlling shareholder of Kretam with 66.89% equity interest. Its top 30 shareholders include Mingo Development Sdn Bhd, Morisem Consolidated Sdn Bhd and Akas Permai Sdn Bhd.

It is worth pointing out that Freddy is the largest shareholder of Sandakan-based timber firm Priceworth International Bhd, with a direct stake of 26.96%, where his brother Andrew Lim Nyuk Foh is managing director.

‘Our shares are undervalued’

Year to date, the share price of Main Market-listed Kretam had fallen 12% to close at 49.5 sen last Wednesday, giving the company a market capitalisation of RM1.15 billion. The counter is trading at a historical price-earnings ratio (PER) of 6.2 times, lower than the average 8.4 times for plantation stocks on Bursa Malaysia.

On its share price performance, Lim is of the view that Kretam is an undervalued stock. “We would like to think that investing in our stock will not go wrong for long-term investors. Theoretically, if our PER could revisit 12 to 15 times, which we think we deserve, our share price would easily go back to RM1,” he says.

Lim adds that Kretam will continue to perform well even when CPO prices normalise because it is an integrated plantation group with both upstream (plantation, mills and fertiliser plant) and downstream business (refinery and biodiesel).

In FY2021, the refinery segment generated revenue of RM707 million, while the plantation segment contributed revenue of RM520 million. But in terms of profit, the plantation segment contributed RM120 million in FY2021, which was higher than RM46 million generated by the refinery segment.

Lim highlights that Kretam’s plantation segment has a better profit margin than the refinery segment, as CPO and FFB prices have risen significantly. Hopefully, he says, the return of more foreign workers post-Covid will provide better management and yield to the group’s plantation segment.

Kretam has four estates in Sandakan, three in Lahad Datu and two in Tawau. In total, the estates measure 24,744ha, of which 20,090ha are plantable areas. The group also operates three oil mills in Sandakan, Lahad Datu and Tawau, with a combined capacity of 135 tonnes per hour.

Kretam operates an integrated refinery and biodiesel plant, which produces edible oils and biodiesel from palm oil, at the Sandakan Palm Oil Industrial Cluster. It has the capacity to process 1,500 tonnes of CPO and refine 300 tonnes of palm methyl ester (PME) per day.

On its earnings performance, Lim foresees that FY2022 will be another good year for Kretam. “Our net profit reached a record high of RM153.3 million in FY2021, when CPO prices were in the range of RM4,000 to RM5,000 per tonne. We expect CPO prices to remain strong at least until the end of this year. Against this backdrop, we expect to see profit growth in FY2022,” he says.

“But to be honest, it’s hard to predict our earnings performance beyond FY2022. Overall, we believe Kretam, like most plantation companies, will continue to register a healthy financial performance and grow steadily.”

Interestingly, in February 2018, Hap Seng Plantations Holdings Bhd had announced its intention to acquire a 55% stake in Kretam for RM1.18 billion, but the deal fell through about four months later. Hap Seng Plantations decided not to proceed with the deal after it found the results of its due diligence to be “unsatisfactory and unacceptable”.

When asked about what transpired then, Lim merely replied, “We are unable to answer this because we didn’t get an explanation from them. As to whether our stake is still up for sale, I think it is difficult to justify a good price at the moment. But at the current price, we are not interested in selling.”

After a two-year pause, Kretam resumed paying dividends in FY2020 (two sen per share) before reducing it to one sen per share in FY2021, which translates to a dividend yield of 2% based on its current share price.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments