Brokers Digest: Local Equities - Coastal Contracts Bhd, Nestlé (Malaysia) Bhd, Panasonic Manufacturing Malaysia Bhd, 7-Eleven Malaysia Holdings Bhd

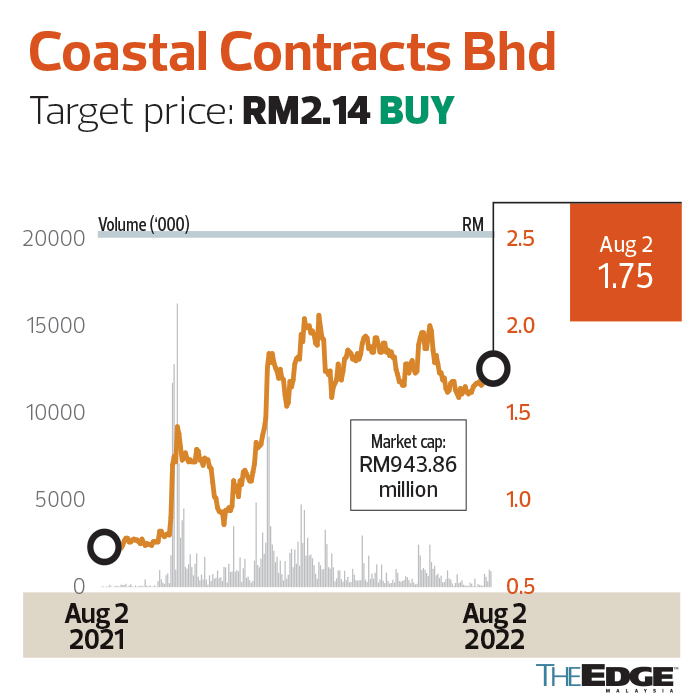

Coastal Contracts Bhd

Target price: RM2.14 BUY

RHB RESEARCH (AUG 1): We are upbeat on this stock on the basis of its long-term recurring income business model and Coastal establishing itself as a gas processing player, which could lead to more contract wins.

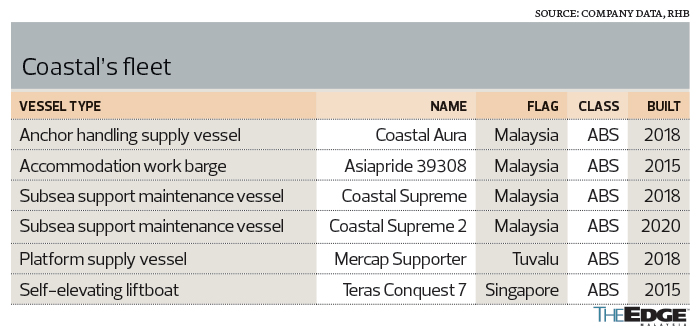

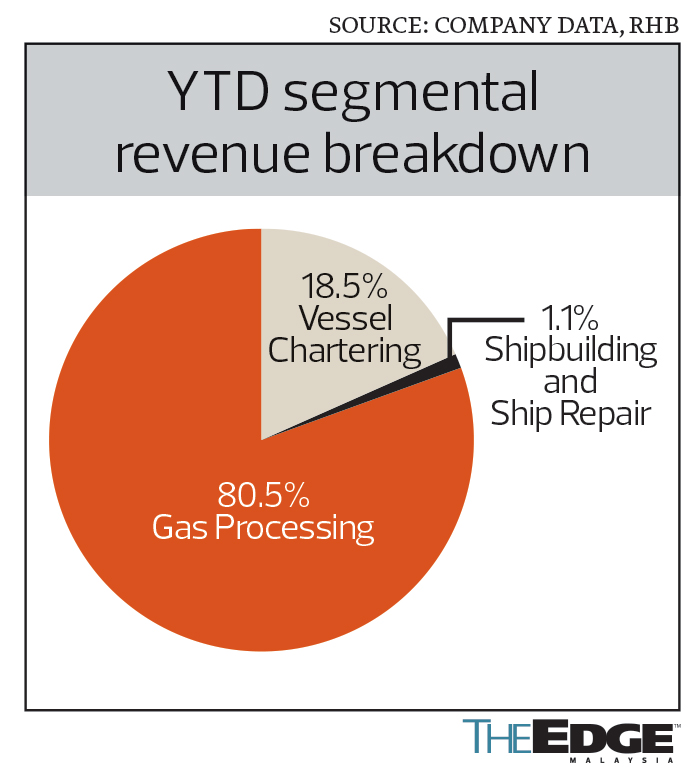

Coastal’s game plan in building a recurring income stream through its gas division started with the acquisition of a jack-up gas compression service unit (JUGCSU), which is currently the major contributor to group revenue and earnings with an annual top line of RM130 million. Although the unit’s contract is set to expire in November 2023, there is a good chance of it being extended due to its consistent production rate, along with Pemex (Mexican national oil company) requiring eight JUGCSUs.

Coastal’s venture into the liftboat business in 2021 has helped its chartering division, delivering RM41 million top line per year, making it the main contributor. The contract has been extended, with an upward revision in its charter rate for a firm period of two years with two-year annual extension options (set to commence in September 2022).

We forecast an earnings increase of 9.7% year on year for FY2023, mainly driven by income from its EMC Papan plant which is split into 10:90 for FY2022 and FY2023 as it is recognised on a milestone basis. Profit for FY2024 will decrease, due to the absence of engineering, procurement and construction (EPC) earnings coupled with the assumption of a downside charter rate upon the JUGCSU’s contract extension. FY2024 will be anchored by gas processing earnings — a strong indicator of Coastal’s effective recurrent income strategy.

The group has a healthy balance sheet with a net cash position of RM142.9 million (27 sen per share) as of Q32022. Total borrowings significantly increased to RM243.5 million from FY2021’s RM92.3 million. Under management’s guidance, borrowings are expected to increase in the upcoming two quarters to facilitate the EPC of the Papan plant. Even so, the rise in borrowings is cushioned by the increase of cash and cash balances which stand at RM371.4 million, supportive of new projects and expansion. The group’s return on equity (ROE) has also improved from 1% in 9MFY2021 to 6% in 9MFY2022, and is expected to increase in the following quarters.

Key downside risks include contract terminations by Pemex, significantly lower-than-expected oil prices that could limit client spending, as well as higher-than-expected operating costs.

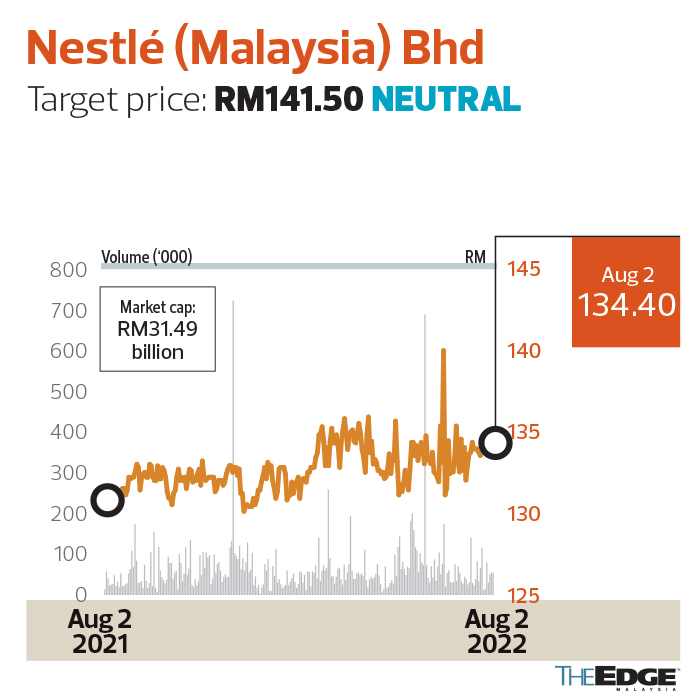

Nestlé (Malaysia) Bhd

Target price: RM141.50 NEUTRAL

MIDF RESEARCH (AUG 1): The group believes that the multiple headwinds will persist in 2HFY2022. The still-high commodity and material prices, currency fluctuations, supply disruption, and the increase in minimum wage will have a significant influence on product costs, which might lead to a decline in profit margins. The group hedged against the US dollar to reduce the effects of a weakening ringgit because the raw materials were bought in US dollars. The final effort to mitigate the impact of margin erosion, according to management, will be an increase in selling price.

We expect the group to continue experiencing margin compression due to its inability to fully pass on the higher input costs to the consumer amid the inelastic demand for its products.

Nevertheless, Nestlé’s long-term prospects are positive, supported by its strong balance sheet and high inventories, which could provide a cushion towards any downside risk.

The downside risks are: (i) a significant depreciation of the ringgit against the US dollar; and (ii) a further increase in commodity prices, which will add pressure on the margins.

Post-analyst briefing, we kept our earnings forecast as we had previously factored in the higher input costs when making our forecast.

Panasonic Manufacturing Malaysia Bhd

Target price: RM22.33 SELL

HLIB RESEARCH (AUG 2): We expect challenges from muted sales, rising raw materials and higher operating expenses to persist for the remainder of the year. The group is expecting to incur 6% to 7% revenue impact from the termination of rice cooker and kitchen appliance products.

We gathered that there was a restructuring cost incurred amounting to RM12.2 million for the termination of the rice cooker products, which have been suffering losses for the past years due to the high raw material costs which eroded profit margins. Additionally, some kitchen appliance products will also be terminated in FY2023 on the back of the realignment of global production for the Panasonic Group. Based on management’s guidance, the termination of rice cooker and kitchen appliance products will impact its revenue by 6% and 7%, respectively.

We gathered that the company was able to resume full operations from March 2022 after the December 2021 floods that hit its SA2 plant in Shah Alam. Despite that, the group had incurred substantial losses from damaged inventories and facilities, coupled with the absence of sales from the operation disruption in FY2022. Total losses amounted to approximately RM24.7 million and we understand that the insurance claimed so far only covers 49% of the total loss with the remaining amount still under review.

Currently, the utilisation rate for the fan segment is running at 85% while for the vacuum cleaner segment, it is at 90%.

7-Eleven Malaysia Holdings Bhd

Target price: RM1.85 OUTPERFORM

KENANGA RESEARCH (AUG 2): We visited and were impressed by 7-Eleven’s second flagship 7CAFé store in Puchong, Selangor (one of the only two there for now). Leveraging on the ability of its collaborators to draw in and retain traffic, the store commands a higher ticket size/customer. We believe the company will put more 7CAFé stores onto the market, which will improve the operational efficiency of its food processing operation with higher volumes and stock keeping units (SKUs).

We maintain FY2022 forecast based on the unchanged assumption of a net addition of 100 stores and same-store sales growth (SSSG) of 4%. We raise our FY2023 earnings by 17% based on an assumption of net addition of 110 stores (from 50 stores) and SSSG of 4% (from -1.9%) to impute better product mix and sustained consumer spending. We like 7-Eleven for: (i) being a reopening play (manifested in its weekend traffic having already returned to the pre-pandemic level of about 300 customers/day, and poised for further growth); (ii) its long-term growth potential driven by 7CAfé stores; and (iii) efficiency gains from in-sourcing of product distribution (such as chilled products) as well as improved operating leverage at its food processing unit.

Key risks to our call include: (i) the return of movement restrictions, hurting traffic to the stores; (ii) the playing field getting more crowded with new entrants or aggressive expansion by exisitng competitors; and (iii) long-term implications from the generational tobacco ban.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments