CYL’s share price surges despite management warning of margin erosion

KUALA LUMPUR (Sept 22): Plastic packaging firm CYL Corp Bhd's shares continued to surge on Thursday despite reporting a net loss in its latest quarterly result and the management's warning of margin erosion going forward.

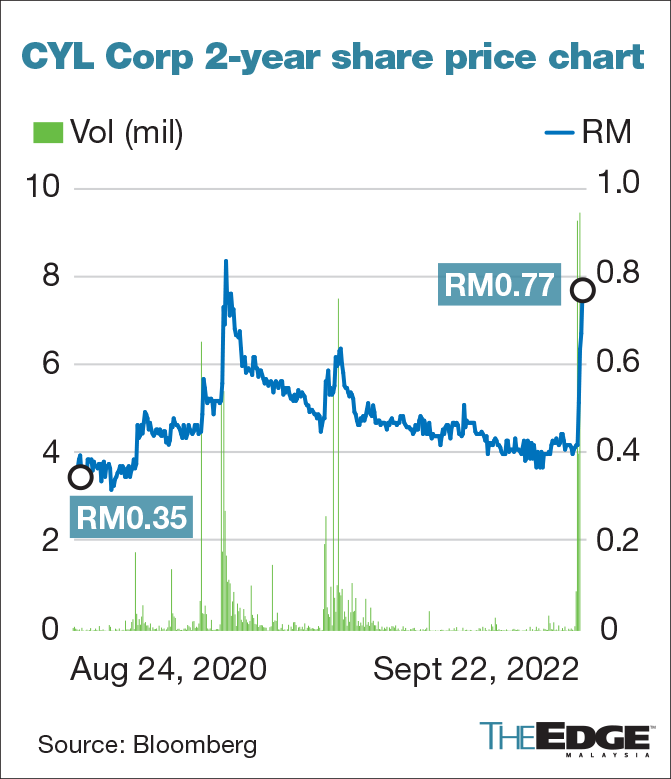

The stock, which has been climbing since Monday, rose by as much as 19% on Thursday before paring gains to close 9.5 sen or 14% higher at 76.5 sen.

With this, this counter has jumped 82% over the last four days, against last week's closing price of 42 sen.

Trading volume was high as well, rising above 500,000 shares on Monday for the first time since August last year. On Thursday, volume shot up to 9.45 million shares, the highest since November 2003.

CYL is mainly involved in the plastics packaging industry through its wholly-owned subsidiary, Perusahaan Jaya Plastik (M) Sdn Bhd (PJP), which was founded by its 81-year-old managing director Chen Yat Lee, who has the largest stake of 34.8% in the group.

Another 19.8% stake in PJP is held by his son and executive director Chen Teck Shin while PJP chairman and former attorney-general Tan Sri Abu Talib Othman, 83, owns 15.6%.

Another son of Yat Lee and alternate director, Chen Teck Sun, 47, was recently appointed to CYL’s boardroom as executive director, effective Monday.

Teck Sun joined PJP in 2000, and was appointed as the general manager in 2014, primarily responsible for the group's manufacturing operations, product development and sales division.

Apart from Teck Sun and Teck Shin, Yat Lee’s daughter Chen Wai Ling, 48, also sits on the board as executive director.

For the second quarter ended July 31, 2022 (2QFY23), the group's net loss narrowed by 68% to RM287,000 from RM888,000 reported a year earlier while revenue dropped 4.5% to RM10.68 million from RM11.19 million.

The earnings performance was however weaker compared to 1QFY23, when the group posted a net profit of RM535,000 on revenue of RM13.78 million.

CYL said the weaker performance was attributable to lower sales volume and higher expenses.

The group expects FY23 to remain challenging due to higher input costs driven by more expensive resins amid stronger crude oil prices and increase in minimum wage.

"These two cost push factors, effecting the major cost drivers, will be a precursor to margin erosion for the group,” it said in its stock exchange filing on Monday.

“The group will be taking steps to maintain sufficient liquidity to enable it to meet its liabilities as and when they fall due. Against this backdrop, the board will continue to focus on improving productivity and efficiency to enable the company to continue to improve its performance,” it added.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| CYL | 0.565 |

Comments