Brokers Digest: Local Equities - Kotra Industries Bhd, Uzma Bhd, Magni-Tech Industries Bhd, Bermaz Auto Bhd

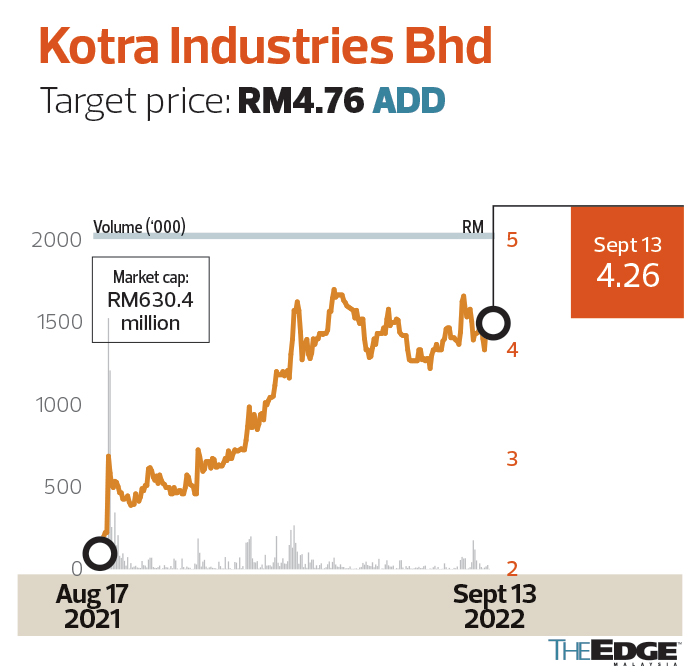

Kotra Industries Bhd

Target price: RM4.76 ADD

CGS-CIMB RESEARCH (SEPT 12): We estimate that Main Market-listed Kotra is the second-largest locally listed manufacturer of over-the-counter (OTC) pharmaceutical products by CY21 revenue. OTC products, mainly represented by its Appeton brand, form the lion’s share of its business, accounting for 60% to 65% of FY6/21 total revenue. It also produces a wide range of generic ethical (prescription) drugs in various dosage forms, under the Axcel and Vaxcel brands, which form the remaining 35% to 40% of revenue. Kotra derived 71% of its FY22 total revenue locally, with the remaining 29% contributed by export sales. Currently, it operates two manufacturing plants in Cheng Industrial Estate in Melaka.

Out-of-pocket spending at private pharmacies in Malaysia should rise further due to improving affluence and health awareness. Local generic ethical drug sales may also continue to grow, as generics made up only 45% to 50% of total ethical sales at end-2018 and are priced three times lower than foreign originators on average. Kotra is a key beneficiary, with its good brand and production capacity utilisation of only 35% to 40%.

Kotra aims to deepen its presence in existing export markets, particularly Asean and Africa, by expanding its product portfolio and bidding for more government contracts. We see the gradual reopening of borders and easing of supply chain/logistical issues sequentially lifting export sales in FY23F, aided slightly by the weak ringgit against the US dollar.

We believe Kotra’s competitive advantage lies in its strong Appeton OTC brand, built via: (i) sizeable, sustained and strategic advertising and promotion investments, and (ii) use of analytics capabilities to plan/evaluate marketing campaigns. This has allowed it to garner better pricing power, with its products priced at a 5% to 89% premium to comparable products by peers, as per our channel checks. We think this has led to its superior ROE (CY23F: 20.9%) versus the Malaysian pharmaceutical sector (average: 14.6%; includes Apex Healthcare Bhd).

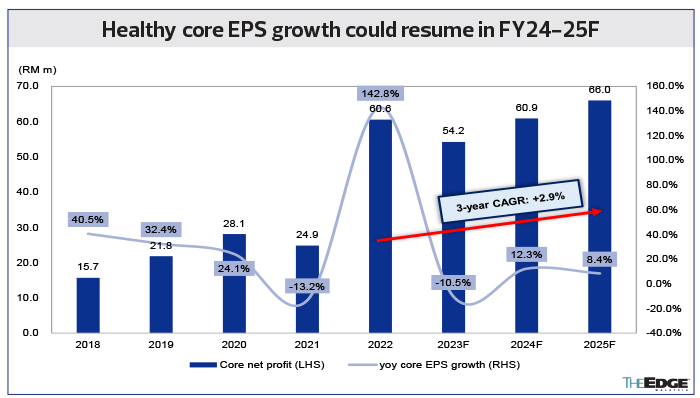

We advise investors to look past the FY23F EPS blip and accumulate the stock for its strong brand recognition, industry-leading ROE, balance sheet strength (end-FY22 net cash: 56 sen per share) and management quality. Kotra’s CY23F PER is also the lowest in the local pharma sector — 1.0 standard deviation (SD) below sector mean — with decent FY23F to FY25F yields of 3.9% to 4.8% per year.

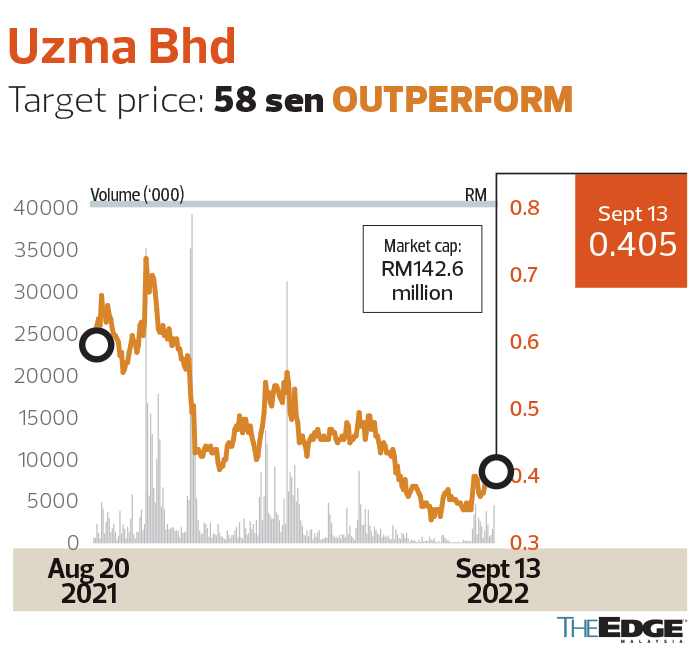

Uzma Bhd

Target price: 58 sen OUTPERFORM

KENANGA RESEARCH (SEPT 13): Uzma has been awarded a RM17 million contract by Petronas Carigali Sdn Bhd for the provision of a lightweight hydraulic workover unit. The campaign will be for two wells, with work expected to commence in September and be completed in October. The award of the contract ties in with Petroliam Nasional Bhd’s guidance for a surge in well decommissioning activities in the coming two to three years, as outlined in its activity outlook report.

The contract value represents less than 1% replenishment towards its current oil and gas order book totalling RM2.15 billion. We expect the contract to fetch a gross margin of about 40% — in line with its current average.

We made no changes to our FY23F and FY24F forecasts (implying earnings growth of 28% to 33%), as the earnings contribution from the contract is immaterial.

We like Uzma for: (i) being a good proxy to elevated oil prices given its focus on the brownfield segment, providing a wide range of services such as well services, oil production enhancement and optimisation, as well as late-life operation and maintenance, and (ii) its diversification into the solar energy space, which will help future-proof its longer-term prospects.

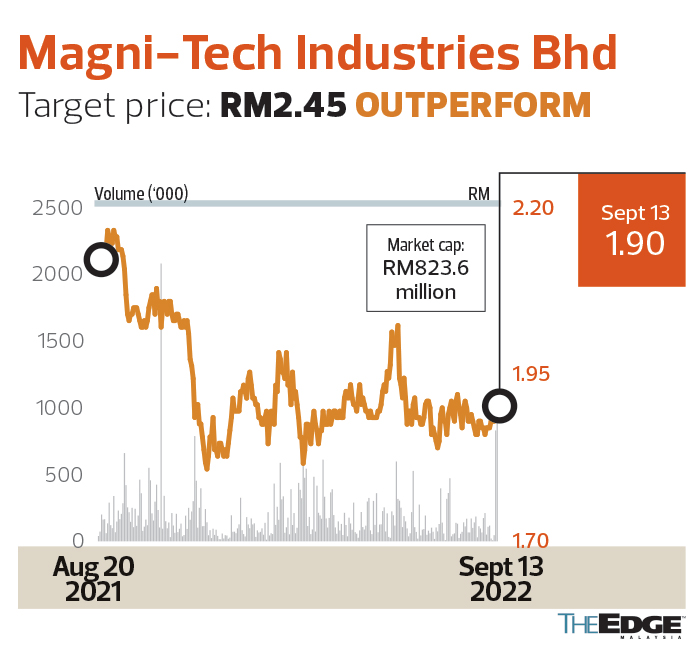

Magni-Tech Industries Bhd

Target price: RM2.45 OUTPERFORM

PUBLICINVEST RESEARCH (SEPT 13): Magni’s 1QFY23 net profit grew 14.2% year on year to RM24 million, driven by stronger sales orders from the packaging and garment segments. After stripping out non-core items, the company’s core net profit came in at RM23 million. Its results were in line with our expectations, accounting for 21% of our full-year forecast. We tweak our numbers for FY23F to FY25F by 2% to 3% due to housekeeping changes.

We expect Magni to post stronger earnings going forward, on the back of robust demand for sports apparel given the change in consumer trends. In addition, we believe the decline in sales from China due to strict lockdown measures will be mitigated by the growth in sales from North America, Europe and Asia-Pacific. We think Magni’s major client’s growth strategy, which focuses more on digital, and its consumer direct acceleration strategy will enable it to build deeper relationships with consumers, thereby leading to a greater demand from consumers. Meanwhile, we opine that the company’s current stock valuation looks attractive, as it is trading at a forward PER of about seven times, which is near -1SD of its three-year historical average.

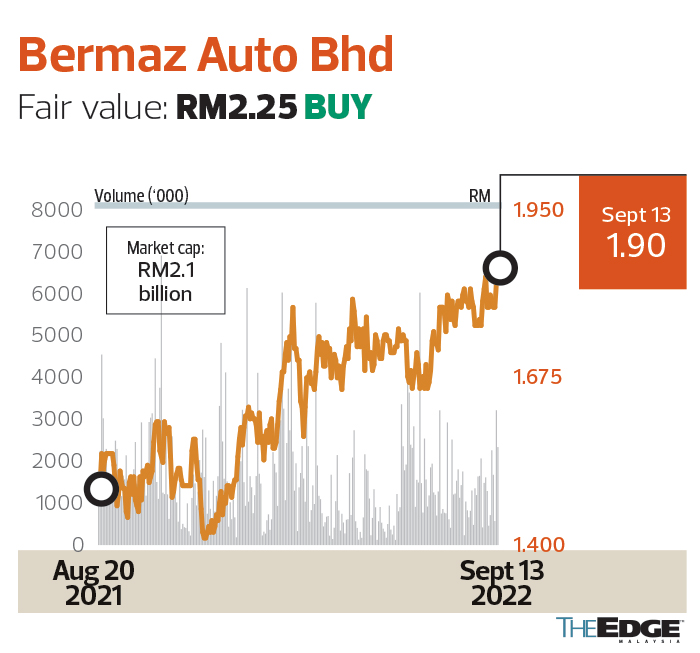

Bermaz Auto Bhd

Fair value: RM2.25 BUY

AMBANK RESEARCH (SEPT 13): We make no changes to our earnings estimate as BAuto’s 1QFY23 net earnings of RM50 million (-36% quarter on quarter, 3.9 times y-o-y) were largely in line with our expectation. The core net profit accounted for 25% of our forecast and 28% of consensus projection compared with historical 1Q, which had contributed 19% to 35% of full-year earnings in FY17 to FY19.

BAuto’s outstanding order book doubled q-o-q to 11,900 units — (i) Mazda 10,000 units, (ii) Kia 1,300 units, and (iii) Peugeot 600 units — as at mid-August. This is sufficient to fuel its sales for at least the next six to seven months.

In addition, the group’s booking rate remains healthy post-Sales and Service Tax (SST) exemption period, with 900 orders in July versus 1,100 to 1,200 during a normal period. This is mainly attributed to BAuto’s exercise of absorbing 50% of the SST hike for new bookings from July to December this year.

Another key earnings rerating catalyst for the company is the introduction of the locally assembled CX-30, in our view. With the production line currently being set up at the Inokom plant in Kulim, Kedah, the completely knocked down programme is set to materialise soon. With the strong sales visibility and earnings catalysts still intact, the company is trading at an undemanding FY23F PER of 10.6 times versus its five-year historical average of 13 times.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments