Brokers Digest: Local Equities - Swift Haulage Bhd, Carlsberg Brewery Malaysia Bhd, SFP Tech Holdings Bhd, Ranhill Utilities Bhd

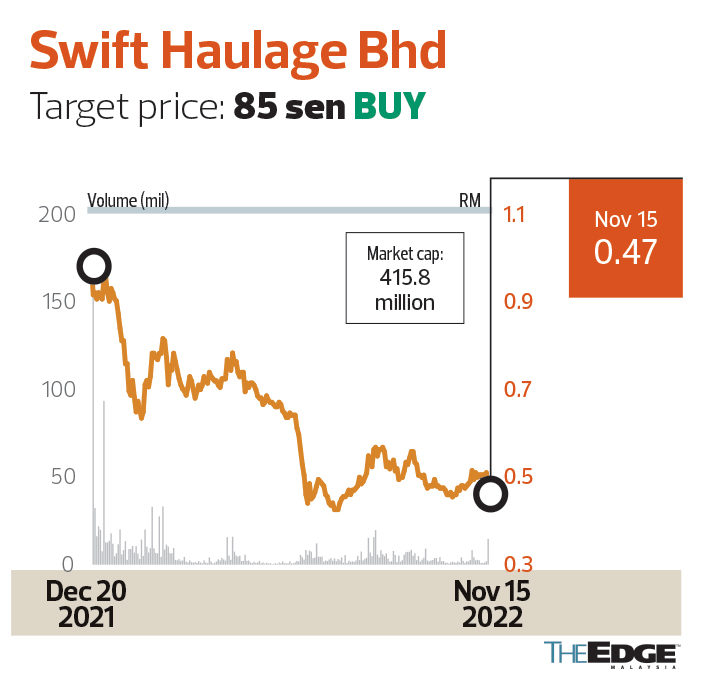

Swift Haulage Bhd

Target price: 85 sen BUY

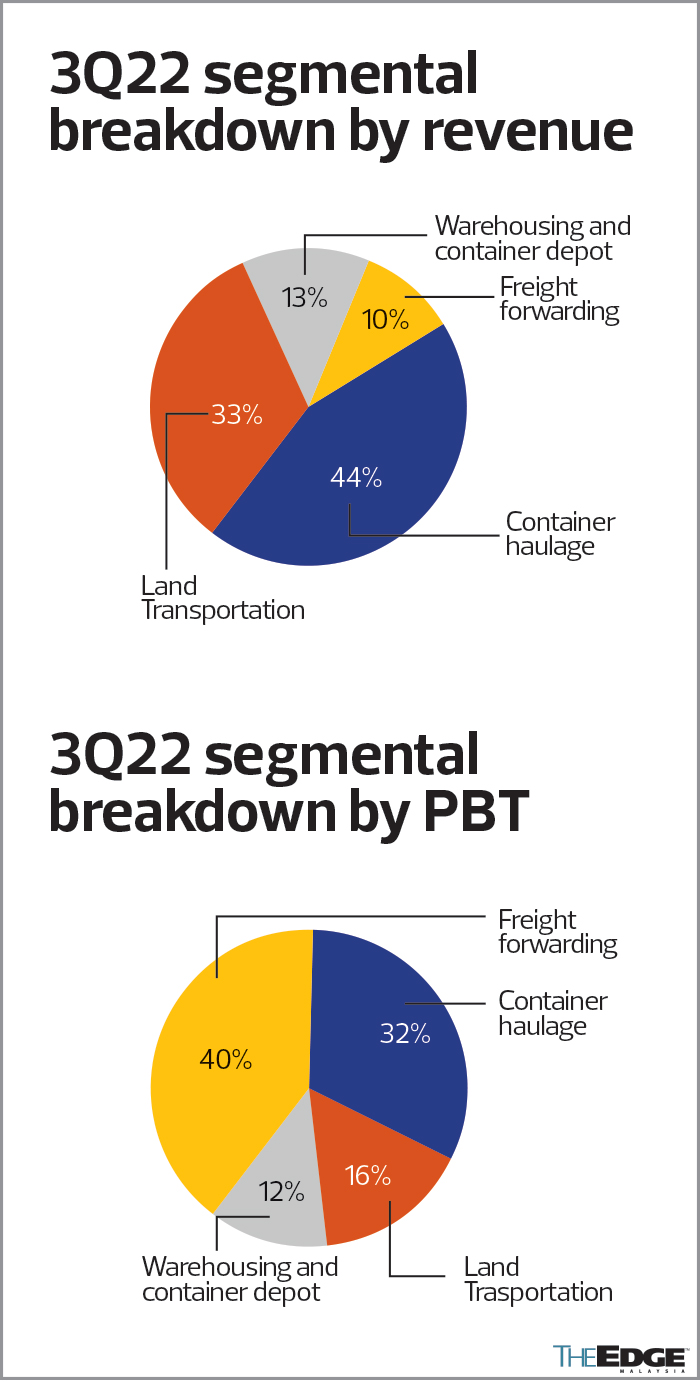

APEX SECURITIES (NOV 15): Swift’s 9M22 earnings missed expectations as the 9M Patami only accounted for 66% of our and 69% of the consensus full-year earnings forecast. The sluggish performance was mainly due to lower business volume from land transportation and freight forwarding. However, we are expecting 4Q22 to have a better performance due to the seasonal effect of the peak festive season. Container haulage accounted for 44% of total revenue, while the freight forwarding business contributed 40% of the group’s total profit.

The warehouse and container depot segment accounted for 11% of 9M22’s total earnings contribution. We are optimistic that the segment will become the main driver of the group’s earnings growth, underpinned by a gradual ramp-up and expanded warehouse capacity in Seberang Prai, Tebrau and Port Klang Free Zone.

The management is planning to expand its capacity by another 50% in FY23-FY24 in Sabah (cold chain), Penang and Shah Alam. The warehousing expansion could provide synergy effects and benefit other segments. Elevated crude oil prices prompted Petronas Refinery & Petrochemical Corp Sdn Bhd (PRPC) to ramp up production, benefitting Swift. Although higher crude oil prices dented Swift’s margin of operation, on the flip side, the group benefitted from the higher demand for transportation for Petroliam Nasional Bhd Group’s petrochemical products.

The recent share buyback activities by the management in the RM0.480-RM0.505 range have provided a level of support to the company from short-term price fluctuations. Downside risks persist as the global supply chain disruption is deteriorating due to external headwinds such as geopolitical conflict and a global economic slowdown as a result of tightening monetary policy to tame inflationary pressure. Other downside risks include a shortage of drivers and the global freight rate dropping deeper than expected.

We maintained our “buy” call on Swift, with a lower target price of 85 sen, from 87 sen previously, due to an earnings forecast downgrade. The target price is pegged at a PER of 13 times as industry peers are currently trading at 12-15 times one-year forward PER. Our target price renders 67% upside against the current share price of 51 sen.

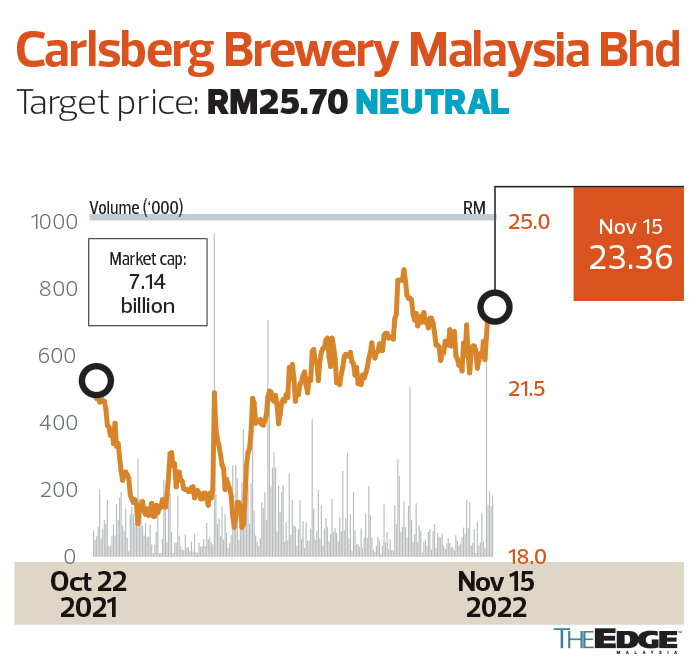

Carlsberg Brewery Malaysia Bhd

Target price: RM25.70 NEUTRAL

RHB INVESTMENT BANK (NOV 14): Carlsberg’s 9M22 results beat estimates on stronger-than-expected sales momentum. Looking ahead, we believe earnings will be sustained by average selling price (ASP) adjustments and intensified marketing initiatives. That said, we believe its current valuation is fair, reflecting the recovery prospects, and do not see a compelling reason to stretch our valuation. We prefer Heineken Malaysia (HEIM) for its cheaper valuation (trading at about a 10% discount to Carlsberg).

Post-results, we raise FY22-23 earnings by 5%-8%. Correspondingly, the target price rises to RM25.70, implying 22 times PER FY23, which is on par with the implied valuation ascribed to its peer, HEIM. We believe this is justified, taking into account HEIM’s market leadership in Malaysia, which is balanced by Carlsberg’s diversified earnings base.

Management expects Carlsberg’s outlook to remain challenging, given the global inflationary pressures, supply chain disruptions and further cost pressure. We also believe that a slowdown in global economies will also be a major risk, dampening consumer sentiment and spending. To mitigate the challenges, Carlsberg may ramp up marketing efforts to engage with consumers and defend its market share.

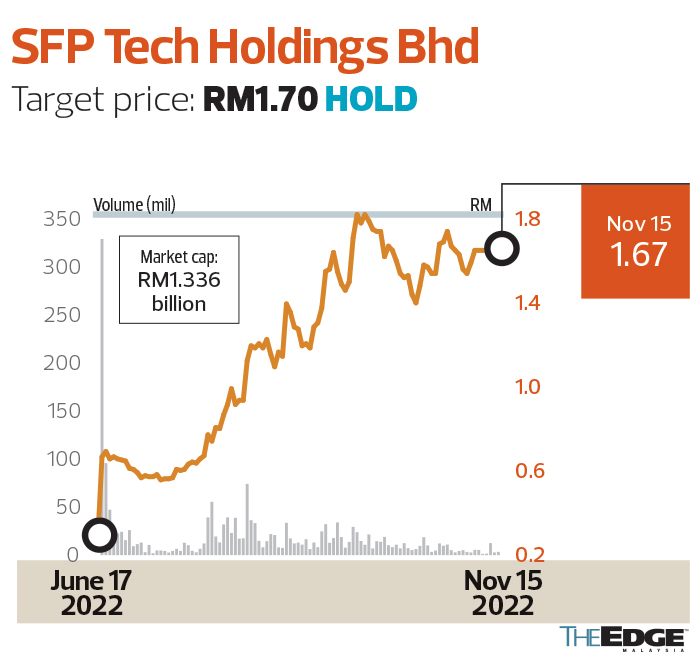

SFP Tech Holdings Bhd

Target price: RM1.70 HOLD

UOB KayHian (NOV14): SFP reported a solid 3Q22 core net profit of RM9.4 million, bringing 9M22 core net profit to RM25.2 million, which made up 84%-86% of our and the consensus’ full-year expectations. Note that year-to-date core net profit has already exceeded 2021’s record-high net profit by 33%. The positive deviation was due to the higher-than-expected job intakes from metal-sheet fabrication and computer numerical control machining segments, thanks to the US-China trade tensions and strategic exposure in the high-growth segments.

SFP plans to venture into the semiconductor back-end inspection industry by manufacturing vision inspection equipment handler platforms installed with camera imaging and electronics systems to be embedded into its automation solution provision. We understand that the unit has gotten good indications from one of its electronics manufacturing services customers about the potential loadings for its auto-screwing machines, with total addressable markets over 20 times its past production volume in a blue-sky scenario.

We increase our 2022-23 earnings forecasts by 9%-14%. Downgrade to “hold”, with a higher target price of RM1.70, based on 30 times 2023 PER.

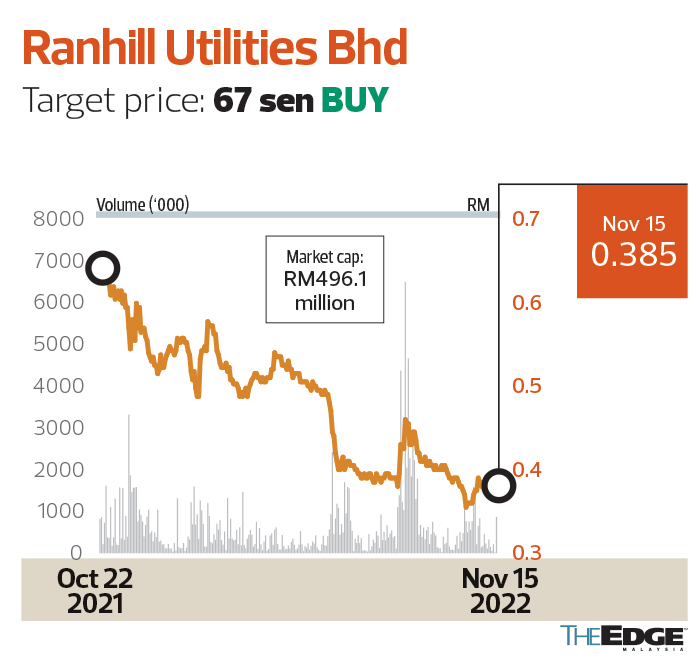

Ranhill Utilities Bhd

Target price: 67 sen BUY

MIDF RESEARCH (NOV 15): Via 51%-owned Ranhill Worley Sdn Bhd (RWSB), Ranhill announced a sizeable contract win from SembCorp Marine Integrated Yard Pte Ltd. The contract is for the detailed engineering design of a new P-82 floating production, storage and offloading (FPSO) vessel for a contract sum of US$27 million (RM124 million) over a 14-month period. We estimate RWSB’s order book will expand to RM278 million (slightly more than a year’s worth of its annual revenue), the bulk of which comprises this latest project.

The bulk of the project is expected to be completed in FY23. We estimate around RM106 million revenue contribution in FY23 and another RM17 million contribution in FY24. At an estimated project margin of 9% to 10% and based on Ranhill’s 51% stake in RWSB, we estimate the project to contribute RM4.9 million to Ranhill’s net profit, or 11% of FY23 earnings. As this forms part of our order book replenishment assumption for RWSB, we keep our projections unchanged at this juncture. Nonetheless, this is a positive development in sustaining RWSB’s contribution to the group.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments