Investors look forward to post-election, window-dressing catalysts

THE formation of a unity government led by Pakatan Harapan (PH) sparked the highest gain in the FBM KLCI in over two years after the benchmark index leapt nearly 60 points or 4% to 1,501.88 points last Thursday.

Indeed, the swearing-in of Datuk Seri Anwar Ibrahim as Malaysia’s 10th prime minister was a strong catalyst for the local bourse as investors are hoping for a better outlook.

The FBM KLCI ended at 1,486.54 points last Friday after profit-taking emerged, paring the weekly gain to 2.6%.

Analysts are generally of the view that the positive sentiment in the local bourse will continue towards the end of the year, aided by the window-dressing effect.

“We have the usual December window-dressing effect, so we are a bit more positive on the local market. Externally, investors are anticipating that the Fed will slow down the pace of rate hikes,” the head of a bank-backed research house tells The Edge.

Since 2009, after the global financial crisis, the FBM KLCI has delivered positive returns in the month of December in 12 out of the past 13 years. While December 2014 recorded a negative 3.3% return, the window-dressing effect was evident in the second half of the month.

For 2023, the bank-backed research house head sees a risk to the earnings growth of Bursa Malaysia-listed companies on the possibility of the US and Europe falling into a recession.

Another research house head observes that many institutional investors have been sitting on big cash piles, owing to external and internal uncertainties. With the political uncertainty on the local front resolved, he sees a good chance of the bourse registering decent returns in December.

Victor Wan, head of research at Inter-Pacific Securities, does not rule out that the FBM KLCI may hit 1,600 points if market optimism persists.

“In the past few years, there hasn’t been much market confidence because of the fragmented political landscape. If the new government works well, I suppose there will be some legs for the market to move.

“Having said that, we have to keep an eye on a possible slowdown in global economic growth in 2023, even though the US Fed is looking at slower interest rate hikes,” he says.

MIDF Research head Imran Yassin Yusof opines that the external factor is much more prevalent for the local market, saying that last Thursday’s rally was partly attributed to the US Federal Reserve minutes indicating a switch to smaller rate hikes soon.

“The resolution of the political situation is not the only factor for the market rally. Throughout the years, the market was quite independent regardless of who the government was. It will be very positive for the local market if the US Fed slows down its rate hike pace,” he tells The Edge.

Although there will be pressure on earnings next year, Imran believes local corporates will still be able to register earnings growth, supported by robust domestic demand. He prefers banking stocks for dividends, as well as laggards such as oil and gas stocks, which may catch up next year as oil prices remain at high levels.

In view of the various forms of assistance promised in the PH manifesto, MIDF Research expects the consumer sector to be a clear winner as it benefits from the production and export incentives.

While the construction sector in Sarawak and Sabah is likely to be a beneficiary, the research house says a more prudent development expenditure could moderate the sector. It added that the telco sector might see prolonged uncertainty on 5G under the new administration.

MIDF raised its FBM KLCI year-end price-earnings (PE) valuation target from 14.9 to 15.2 times, and the index target from 1,520 to 1,550.

RHB Research expects the relief rally to be extended as equities play catch-up to build on the recent tentative shift in investor sentiment that is a result of rising hopes that the pace of monetary tightening will begin to ease and as the market looks ahead to a more pragmatic approach by China to contain Covid-19.

That said, it cautions investors not to get too carried away in the short term, given that the new unity government needs to prove its ability to work together as a team.

“We think subsidy and fiscal reforms will be the acid test. The presence of the Borneo bloc in the new administration will be positive for infrastructure programmes in East Malaysia. Another spike in markets should invite some short-term profit-taking but further out, investors ought to refocus on fundamentals with a preference for large-cap value stocks,” RHB Research says.

The end of the political gridlock has also prompted some research houses to upgrade their FBM KLCI year-end targets.

Kenanga Research has raised its target back to 1,500 points from 1,450 points, based on a 15.5 times 2022 earnings projection from 15 times previously.

“We continue to advocate that investors seek refuge in banks, telcos, auto makers/distributors, mid-market retailers and construction as we believe the ‘unity’ government will be supportive of domestic consumption,” it says in a Nov 24 note.

It notes that under the “power sharing” model, the most likely outcome is the continuation of prevailing policy inclinations at least over the immediate term, including pro-business; protectionism for local industries; business-as-usual for government-linked companies in the economy; strong fiscal support to the economy including cash handouts and fuel and food subsidies to cushion consumers from the rising cost of living; as well as pump-priming via the rollout of public infrastructure projects to shield the economy from an external slowdown and headwinds.

CGS-CIMB Research raised its end-2022 target for the FBM KLCI to 1,602 points from 1,484 points, based on 13.8 times forward PE.

“If the political instability concerns ease over time, there is potential for the FBM KLCI to rerate to its pre-GE14 valuations of 16.5 times, which is close to its three-year average mean PE of 16 times and values it at 1,855 points.”

The research house favours sectors such as consumer (Mr DIY Group (M) Bhd, QL Resources Bhd, Kawan Food Bhd); banking (RHB Bank Bhd, Hong Leong Bank Bhd and Public Bank Bhd); gaming (Genting Bhd, Genting Malaysia Bhd, Magnum Bhd and Sports Toto Bhd); as well as brewery (Carlsberg Brewery Malaysia Bhd and Heineken Malaysia Bhd).

It also expects construction (Gamuda Bhd and HSS Engineers Bhd), telco (Telekom Malaysia Bhd), utilities (Tenaga Nasional Bhd) and property (Sime Darby Property Bhd) to perform well in a more stable political environment.

“Healthcare stocks (pharmaceutical companies) should do well as the Pakatan Harapan manifesto mentioned an increase in healthcare expenditure to more than 5% of GDP, which will be positive for pharmaceutical companies.”

Hong Leong Investment Bank (HLIB) Research has reverted to its previous PE valuation to derive its end-2022 FBM KLCI target of 1,530 points from 1,470 points previously.

Budget 2023 to set market direction

On the re-tabling of Budget 2023, the bank-backed research house head does not think the new government will introduce unpopular measures such as new taxes and subsidy cuts.

“It’s a bit too early for the government to start throwing in these measures. The country has just come out from the political impasse. It’s a loose coalition and it will not be good for their popularity,” he says.

Another research house head points out that the new Budget 2023 will determine the market direction next year. “If people have confidence that it is a better-set-up government than previously, then it will be good for the market, which seeks stability and clarity. However, bear in mind that the new government needs to find new revenue sources to fund its lofty promises. So, there are worries about windfall taxes, high dividend payouts from Petronas and even the progressive tax, which charges the rich higher taxes.”

Roller-coaster ride for sin and politically linked stocks

A slew of politically linked stocks came under the limelight last week, after no single coalition managed to secure a simple majority in parliament.

Stocks that are perceived to be related to Datuk Seri Anwar Ibrahim, namely Advance Synergy Bhd, Malayan United Industries Bhd (MUIIND) and Pan Malaysia Holdings Bhd saw their share prices gain as much as 156%, 55.6% and 52.9% respectively during the week. On a weekly basis, the stocks increased 64%, 11.1% and 11.8%, based on their closing prices of 20.5 sen, 10 sen and 9.5 sen last Friday respectively.

Anwar’s sister Farizon Ibrahim is a director of MUIIND and Pan Malaysia Holdings.

Meanwhile, Tan Sri Muhyiddin Yassin-linked Eden Inc Bhd and Thriven Global Bhd rose as much as 61.8% and 37.9% early in the week after the Perikatan Nasional chairman said PN had secured enough support to form the next government.

However, a sell-off emerged after the palace refuted the party’s claim, resulting in the two counters declining as much as 29.4% and 24.1%, before closing at 17.6% and 17.2% lower on a weekly basis.

Eden and Thriven are said to be related to Muhyiddin’s son Datuk Fakhri Yassin Mahiaddi.

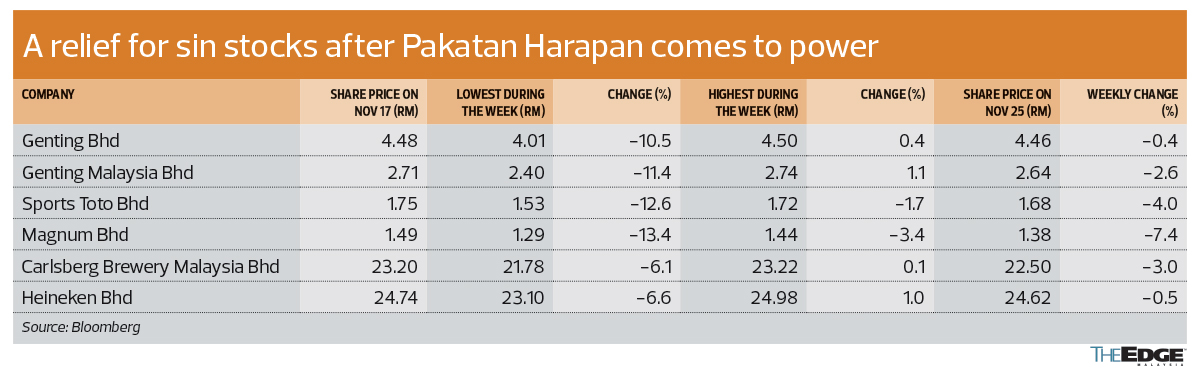

Meanwhile, sin stocks rebounded from a heavy sell-off after PH came into power, but were still below their pre-election levels after profit-taking last Friday.

Fears over a more conservative administration early last week wiped out some RM2.75 billion at the peak of the sell-off, with number forecast operators Magnum Bhd and Sports Toto Bhd suffering the most by falling 13.4% and 12.6%, followed by Genting Malaysia Bhd (-11.4%), Genting Bhd (-10.5%), Heineken Malaysia Bhd (-6.6%) and Carlsberg Brewery Malaysia Bhd (-6.1%).

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| ASB | 0.105 |

| BURSA | 7.460 |

| CARLSBG | 18.380 |

| CIMB | 6.670 |

| EDEN | 0.165 |

| FBMKLCI | 1571.480 |

| GAMUDA | 5.200 |

| GENM | 2.650 |

| GENTING | 4.580 |

| HEIM | 23.000 |

| HLBANK | 19.500 |

| HSSEB | 0.985 |

| KAWAN | 1.800 |

| MAGNUM | 1.150 |

| MRDIY | 1.520 |

| MUIIND | 0.060 |

| PBBANK | 4.250 |

| PMHLDG | 0.215 |

| QL | 6.350 |

| RHBBANK | 5.520 |

| SIMEPROP | 0.915 |

| SPTOTO | 1.390 |

| TENAGA | 11.860 |

| THRIVEN | 0.120 |

| TM | 6.130 |

Comments