The Edge Best Call Awards 2022

THE 17th edition of The Edge Best Call Awards received 73 recommendations for 53 stocks from 13 research outfits. This is about the same as 71 recommendations for 58 stocks from 16 outfits in the 16th edition in 2021 but still noticeably lower than the record high of 131 recommendations for 90 stocks from 19 research houses in 2020. That is not entirely a surprise, with both the bellwether FBM KLCI and broader FBM Emas Index likely to close lower year on year for a second year running in 2022.

Absolute return is a consideration but not the only factor when choosing which call to acknowledge. Other factors considered include the timing of the call, with brownie points given to contrarian calls, strong views and insights proven right.

This year, because of heightened market volatility, it is no surprise that most submissions were not perfect, but a number did come out more decently relative to peers.

It so happens that a number of “sell” calls are acknowledged in our list of winners, some more prescient than others. Timely “sell” calls stand out, as we know there have been analysts who have been excluded from briefings by companies that do not recognise the value of professional critique.

Recommendations for several strong performing initial public offerings (IPOs), as well as stocks that enjoyed a short but steep run, were also shortlisted but failed to make the final cut.

In evaluating submissions against peers, we did come across other calls that were not submitted for consideration. Where possible, attempts would be made to verify these unsubmitted calls for notable mention.

Started in 2005 (we skipped one year but brought it back by popular demand), the awards are our best-effort attempt to recognise good fundamental stock analysis and its importance in making informed investment decisions. They are not meant to influence year-end appraisals or annual bonuses.

The advertisement calling for submissions for 2023 should be out in The Edge and the CEO Morning Brief by November next year. Feedback and early submissions with the relevant research notes are welcomed at [email protected].

Here are this year’s winners — selected based on submissions and publicly available data — in no particular order. Congratulations to all winners. To the unsung stellar stock pickers, keep up the good work.

Merry Christmas and Happy New Year 2023!

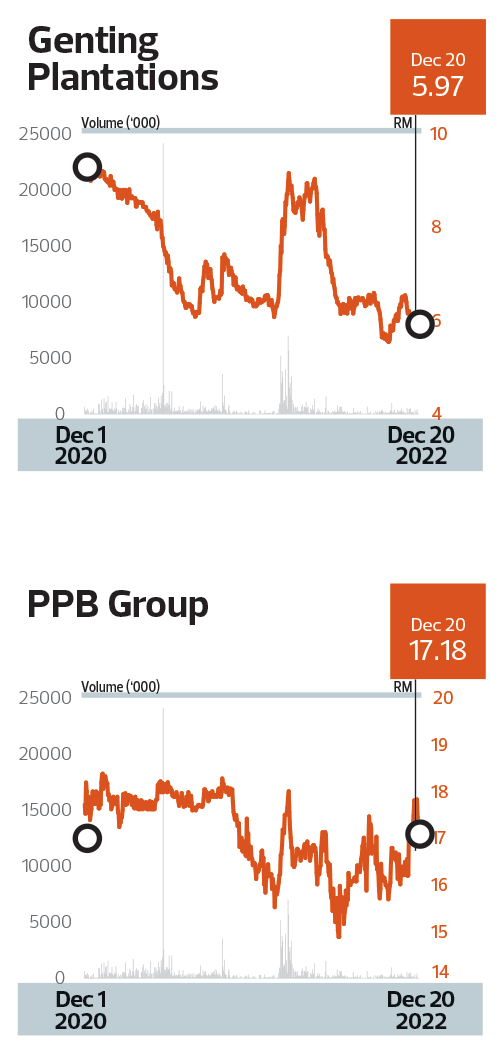

UOB Kay Hian Research analysts Leow Huey Chuen and Jacquelyn Yow’s call on Genting Plantations Bhd and PPB Group Bhd

The “Gordon Gekkos” of the world may live by the mantra “greed is good”, but knowing when to take profit is also key when it comes to investing.

“Take profit” was precisely what UOB Kay Hian Research’s plantation analysts Leow Huey Chuen and Jacquelyn Yow recommended that clients do after Genting Plantations’ share price soared 30% within a fortnight in February this year, telling them that “the potential earnings growth from high CPO [crude palm oil] prices” was already factored in the price after the planter’s 4QFY2021 results came in above expectations from higher average selling prices on the back of high CPO prices.

Investors who took profit when the duo downgraded their recommendation to a “sell” may have sold before the stock soared past the RM9 mark in early March this year — as CPO prices topped RM8,000 per tonne for the first time amid fears of tightness in sunflower oil, following the Russia-Ukraine war — but would have also been spared a precipitous share price plunge when CPO prices retreated.

UOB Kay Hian was one of two houses that downgraded Genting Plantations to a “sell” on Feb 24 this year, Bloomberg data shows, but won brownie points over the other call for also rightly going against the grain in recommending a “sell” in April 2021, ahead of a 26% fall within three months. Most peers had either a “hold” or “buy” call back then.

Notable mention also goes to AmInvestment Bank Research’s Gan Huey Ling, who downgraded Genting Plantations to a “sell” on Feb 24. Both UOB Kay Hian and AmInvestment had “hold” recommendations on Genting Plantations at the time of writing.

Separately, UOB Kay Hian’s Leow and Yow are also acknowledged for being the first to downgrade PPB Group Bhd to a “sell”, with a target price of RM15.60 on March 1 this year after a strong 4QFY2021 earnings release, when the stock price closed at RM17.66 — a timely recommendation that allowed clients to reap profit near the stock’s highest close year to date of RM18.01 on March 3, 2022.

Flagging a “tough environment for PPB”, the duo acknowledged strong contributions from the company’s Singapore-listed associate Wilmar International Ltd but told clients that PPB’s own core business “still faces a tough environment” amid a highly volatile environment for commodity prices that made hedging tough. In addition, PPB’s unit FFM, which faced higher raw material costs, “will not be able to raise prices, as most of their goods are staple products”.

PPB’s share price fell more than 15% from early March to close as low as RM14.89 on June 24. An upgrade at this point would have proved prescient.

Investors who purchased PPB shares — when Leow and Yow upgraded their recommendation from a “sell” to a “buy” on Aug 9 this year, with a target price of RM18.55 when PPB’s share price closed at RM16.28 — would already be sitting on decent portfolio gains, with PPB shares closing at RM17.84 on Dec 16. On top of strong contributions from Wilmar, the two analysts also told clients to buy PPB on margin recovery for its grains and agribusiness segment as well as the anticipation of its film exhibition and distribution segment returning to the black. Bloomberg data also ranks the UOB Kay Hian analysts tops, with a 24% one-year return.

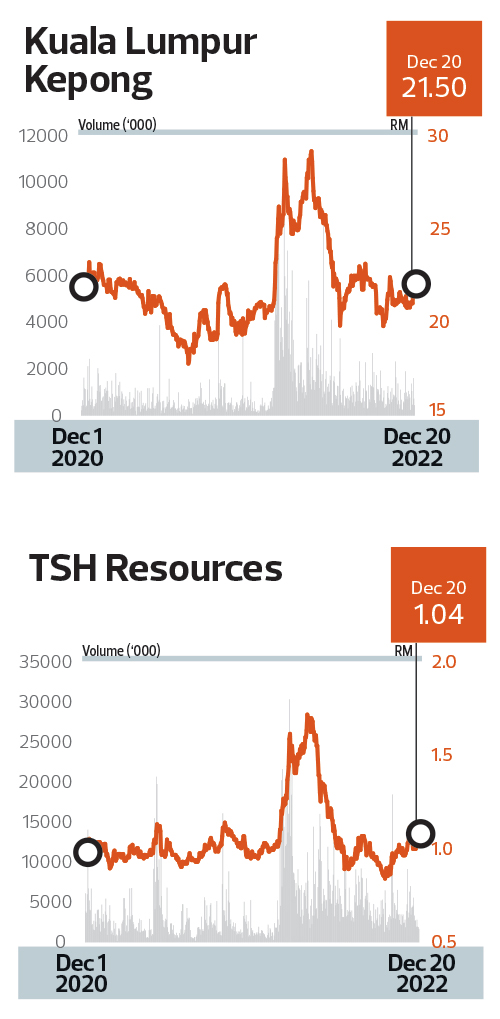

AmInvestment Bank Research analyst Gan Huey Ling’s call on Kuala Lumpur Kepong Bhd and TSH Resources Bhd

Plantation stocks naturally rallied in anticipation of stronger earnings as CPO prices shot past never-before-seen levels of RM8,000 per tonne in early March this year on the back of supply shortage fears, following Russia’s attack on Ukraine in February.

Gan Huey Ling, AmInvestment Bank Research’s veteran plantation analyst, knew investors were already sitting on good gains. Stock prices of both Kuala Lumpur Kepong Bhd (KLK) and TSH Resources Bhd shares had run ahead of what she thought was fair value at the time.

As Gan believed CPO prices were already near their peak, she stuck her neck out and told clients that “with CPO close to RM6,000 per tonne, there is more downside than upside” and recommended profit-taking on the plantations sector.

It takes conviction to make a “sell” call and Gan’s call was contrarian — she was the only one on the street to call a “sell” on KLK on Feb 17 (when the stock price was RM25.55 versus her fair value of RM23.30) and TSH on March 11 (when the stock price was RM1.50, just ahead of her fair value of RM1.40), Bloomberg data shows.

While, with hindsight, we know KLK shares went on to briefly hit RM28 in March and closed above RM29 on April 29 — 10% to 15% more than the RM25.55 that KLK shares closed at when Gan made her “sell” call — the downside was steeper, at more than 22%, when KLK’s stock price dipped below the RM20 mark in July. Since Nov 11, Gan has upgraded her call on KLK to a “hold”, with a target price of RM21.75, a call that was maintained on Dec 14 this year.

Similarly, TSH shares closed as high as RM1.719 on April 11 this year, about 15% more than the RM1.497 when Gan cut her recommendation to a “sell”, but the downside is more than 40%, if measured from the lowest point in July as well as October this year. Gan had cut her target price for TSH to 85 sen on July 13 this year when the stock price was 92 sen. It remains to be seen whether she continues to prove correct. TSH’s share price had inched higher to RM1.03 on Dec 14 this year when Gan maintained a “sell” call with the same target price of 85 sen.

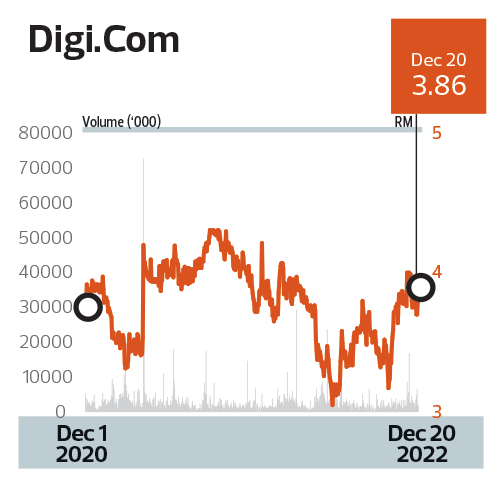

Macquarie Research analyst Izzati Hakim’s call on Digi.Com Bhd

If timing is everything, shares in Digi.Com Bhd were at their lowest year to date on June 13 this year — the day Macquarie’s Izzati Hakim upgraded the stock to “outperform”, with a 6% higher target price of RM3.80.

At the time, Digi’s stock price had already fallen 20% year to date, steeper than the FBM KLCI’s -5%. The consensus view was overwhelmingly lukewarm — four “buys” versus 14 “holds” and two “sells” — Bloomberg data shows, not entirely a surprise, given the sector overhang over downside risks and costs related to the adoption of the 5G single wholesale network (SWN) model.

But Izzati saw opportunity in borders reopening, telling clients in a June 13 note that Digi was its “mobile top pick”, owing to potential earnings upside from incremental prepaid service revenue as migrant workers returned. Izzati told clients that Digi could see about 510,000 additional prepaid subscribers in FY2023, assuming 70% of one million to 1.4 million migrant workers who left the country return by FY2023, with Digi enjoying 70% market share.

To be sure, Izzati’s call is not without flaws, given that Digi shares did plunge 16% between mid-August and mid-October before moving higher. Still, investors who bought the stock on June 13 would have benefited, as Digi climbed just over 31% from RM3.10 to RM4 by late November, with annualised returns at 89% over the five-month period.

With Digi’s share price off its recent high at the time of writing, there is no certainty that Izzati will continue to be right even as the enlarged Digi works to derive synergies after the completion of its merger with Celcom Axiata Bhd on Nov 30. For now, however, her recommendation is the highest-ranked among peers, with one-year return at 23.52%, Bloomberg data shows.

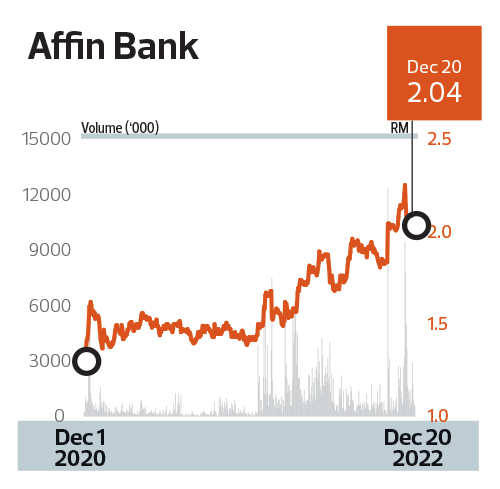

Hong Leong Investment Bank Research Chan Jit Hoong and TA Securities Investment Research Wong Li Hsia’s call on Affin Bank Bhd

Affin Bank Bhd, the country’s smallest bank by asset size, is a dark horse in terms of both share price and earnings performance this year. It is the third-best-performing banking stock on Bursa Malaysia, with a 37% climb for the year until Dec 20.

HLIB’s Chan and TA’s Wong deserve a pat on their backs for recommending Affin Bank, which has been off the radar of many investors for years — possibly as far back as the 1997/98 Asian financial crisis – owing to concerns over asset quality. Indeed, a low price-to-book value ratio is an indicator of weak investing interest. Few would disagree that it is a contrarian call.

The duo were the first to draw investors’ attention to Affin Bank, believing that the banking group would be unlocking asset values.

HLIB’s Chan upgraded Affin Bank to a “buy” in April 2021 when its share price was RM1.52. Investors would have gained more than 40%, as the share price reached RM2.25 in November.

“We were the first to highlight the potential of value unlocking exercises sooner rather than later and the case for special dividends. All these came to fruition … The market generally didn’t talk and highlight these until much later into 2022,” writes Chan in his submission.

To recap, Affin Bank sealed a deal in June 2021 to sell a 21% stake in AXA Affin Life Insurance, along with a 3% stake in AXA Affin General Insurance, to Generali — a move to form a 30:70 joint venture with the Italian insurer.

Seven months later, the bank sold its 63% stake in Affin Hwang Asset Management Bhd, now known as AHAM Asset Management Bhd, for RM1.42 billion cash. Subsequently, it declared a special dividend of 18.09 sen per share.

For 2022, the timing of the “buy” call made by TA’s Wong is just right for investors to ride the upward trend driven by asset sales and improved earnings performance. She reiterated her “buy” call in November 2021, with a target price of RM2, when the stock was RM1.44.

It is worth noting that Kenanga Investment Bank Research’s Clement Chua also upgraded Affin Bank to a “buy” in March after the share price started to rise.

Kenanga Investment Bank Research analyst Lum Joe Shen’s call on S P Setia Bhd

Investors who took profit when Kenanga Research’s Lum Joe Shen downgraded S P Setia Bhd to “underperform” on Nov 24, 2021, after 9MFY2021 earnings missed expectations, would have been able to exit at a decent price and been spared steep paper losses when the stock price tumbled about 70% over 11 months to as low as 41.5 sen on Oct 21, 2022.

The street was largely “neutral” back then — 58.8%, or 10 out of 17 calls being “neutral”, versus two “sells” and five “buys” — with the real estate developer facing oversupply and affordability issues. Sentiment took another hit in May 2022 when S P Setia announced a RM1.18 billion cash call by issuing a new class C renounceable rights issue of Islamic convertible preference shares (RCPS-i C) to refinance existing debt.

Lum was one of only two analysts who had cut their recommendations to a “sell” just over a year ago (when there were 10 “holds” and five “buys”, telling clients that S P Setia’s share price rallied “despite the lack of convincing rerating catalysts [such as] indication of stronger demand data-wise”. His target price was trimmed from RM1.19 on Nov 24 last year to 58 sen by Aug 19 this year.

One year since his call downgrade, Lum is still one of two analysts saying “sell”. Consensus view remains largely neutral but the number of “buys” had increased by two to seven.

Lum’s target price had been cut to 38 sen on Nov 21 this year but S P Setia’s share price had moved up from 55 sen to 71 sen on Dec 5, before giving up some of those gains to close at 64.5 sen on Dec 20. Whether Lum continues to prove correct in the coming weeks and months, Bloomberg data shows his recommendation garnering a 46% one-year return, ranking his call above most peers at the time of writing.

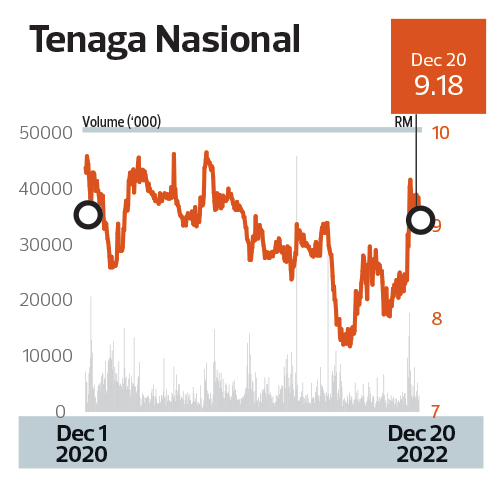

Macquarie Research analyst Max Koh’s call on Tenaga Nasional Bhd

Tenaga Nasional Bhd has been out of favour for quite some time as environmental, social and governance (ESG) principles are growing in importance, especially in the past three years. With coal making up nearly half of its fuel mix to generate electricity, Tenaga is certainly not on the radar of environment-conscious investors.

Among the submissions, Macquarie’s Koh’s “sell” call on Tenaga stands out.

He highlighted, however, the bigger problem that the utility group is facing — ballooning receivables that soared to a record high.

The big rise in receivables is mainly because Tenaga has not been able to promptly receive outstanding payment under the Imbalance Cost Pass-Through (ICPT) mechanism.

Worse still, fuel costs were escalating while the government at the time had kept electricity tariffs unchanged. As a result, Tenaga suffered from tight cash flow, as it paid more for fuels; it needed to raise debt to sustain operations.

For that reason, Koh downgraded Tenaga to a “sell” call, with a target price of RM7.60 on June 9, when most investment analysts were recommending a “hold” or “buy” on the utility stock.

After the downgrade, it tumbled to a near-seven-year low of RM7.07 on July 19, from the RM8.50 level. Nonetheless, Tenaga has regained lost ground, as the new government decided to impose targeted electricity subsidies by raising surcharges on selected groups.

Credit Suisse analyst Joanna Cheah is a notable mention, as she spotted the growing receivables before Koh did and downgraded the stock to a “sell” in April.

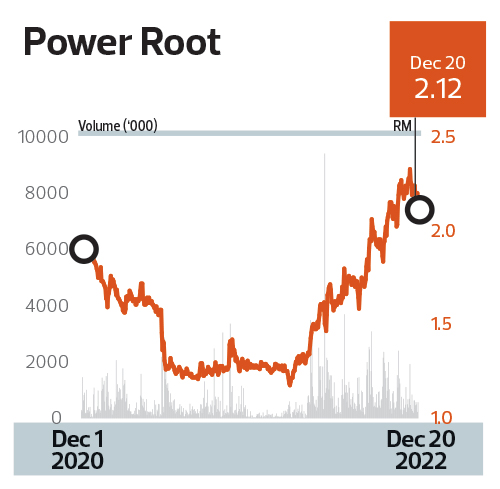

RHB Research analyst Soong Wei Siang’s call on Power Root Bhd

In hindsight, the timing of Soong’s “buy” call on Power Root Bhd could have been better if it had happened two months earlier. Still, it was better late than never. Soong upgraded the stock in late April, adding it to his “buy” list. It was the only such call then, according to Bloomberg. Soong subsequently raised his target price three times, with the last at RM2.60 in October.

Although the counter was already on an uptrend prior to Soong’s upgrade, the share price still soared another 39% to RM2.12 on Dec 20.

While consensus was unconvinced and did not think the worst was over for Power Root, Soong noticed the change in tide on the back of a recovery in key export markets, coupled with margin expansion from price hikes.

The instant coffee sachet maker’s quarterly net profit was on an upward trend for more than four consecutive financial quarters. It posted a net profit of RM15.6 million for the second quarter ended Sept 30 (2QFY2023) — the highest quarterly profit since 4QFY2022.

Furthermore, the improved earnings have brought with them higher dividends. For the first six-month period ended Sept 30, Power Root declared a total interim dividend of six sen per share, including a special dividend of two sen. The interim dividend declared exceeded total dividend per share of 5.4 sen for the financial year ended March 31, 2022.

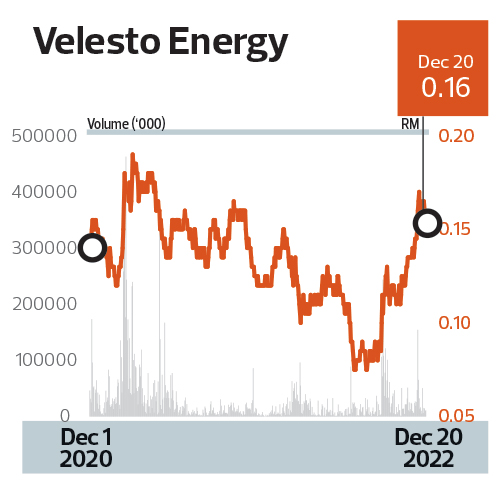

Kenanga Investment Bank Research analyst Steven Chan’s call on Velesto Energy Bhd

When crude oil prices are above US$90 per barrel, it is not that common for investment analysts to downgrade an oil and gas stock, unless the company has sunk deep into financial troubles.

In March, however, Kenanga’s Chan reiterated his “underperformance” call on Velesto that he had made in 2021. It was the only “underperform” recommendation back then, according to Bloomberg. The stock was trading at around 11 sen.

Velesto’s share price continued its downward trend in 2022 and slid to record low of 7.5 sen in mid-July.

Chan’s bearish view hinged on the sluggish demand for jack-up rigs during the earlier parts of the year. “Being the largest jack-up rig player in Malaysia, we felt that this would certainly translate into continued losses for Velesto, unless the group manages to improve its competitiveness and reduce its reliance on Petronas,” he explained in his submission.

In September, Chan upgraded the stock to “outperform” after Velesto rebounded from the trough to 10 sen and he pegged the target price at 16 sen. The stock became the “screaming buy”, as all analysts tracking it were recommending the counter.

Velesto’s share price hit a 20-month high of 19 sen on Dec 6.

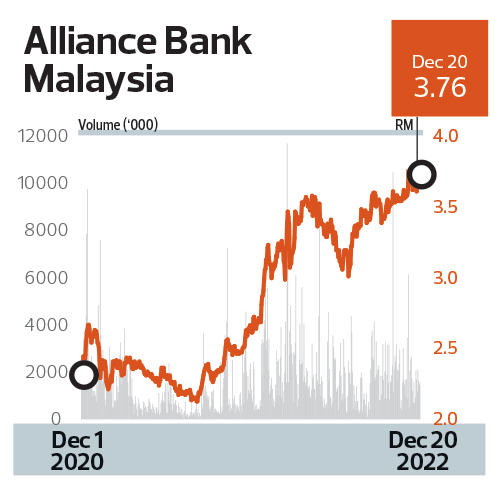

AmInvestment Bank Research analyst Kelvin Ong’s call on Alliance Bank Malaysia Bhd

Alliance Bank was already a “consensus buy” it at the start of 2022, but AmInvestment Bank’s Ong still deserves credit for being among the handful who saw the stock’s upside potential in early 2021.

When he upgraded his call to a “buy” on Feb 2, 2021, there were only four “buy” calls versus eight “holds” and three “sells”, Bloomberg data shows. Investors who bought back then would have seen a gain of 68% (32% annualised). Those who bought when he reiterated his “buy” call in November 2021 would have made a gain of 50%as the stock closed at RM3.76 on Dec 20 this year. His target price was RM3.60 back then.

Alliance Bank’s record earnings for the financial year ended March 31, 2022 (FY2022) helped fuel upward momentum of its share price, as did generous dividend paid in calendar year 2022.

Attractive valuation, better asset quality and normalising dividend payout with improved asset quality were the combination of factors that had Ong bullish about the banking group.

Notable mention also goes to Credit Suisse veteran banking analyst Danny Goh, who upgraded Alliance to “outperform” from “neutral”, with a target price of RM3.42 on Nov 22, 2021.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| ABMB | 3.800 |

| AFFIN | 2.500 |

| BURSA | 7.460 |

| CDB | 4.090 |

| FBMKLCI | 1570.290 |

| GENP | 6.050 |

| KENANGA | 1.080 |

| KLK | 22.920 |

| PPB | 15.920 |

| PWROOT-WA | 0.000 |

| SPSETIA-PA | 0.925 |

| TENAGA | 11.860 |

| TSH | 1.140 |

| VELESTO | 0.265 |

Comments