Analysts prefer EMS firms with exposure to industrial electronic products

NEWLY listed stocks on the local bourse have drawn interest from the investing fraternity in recent months on the back of their stellar share price performance. Electronic manufacturing services (EMS) provider NationGate Holdings Bhd is one of them — its share price has jumped more than 200% since its listing on Jan 12.

Is the EMS sector worth a look, considering the improvement in the companies’ financial results after being affected by labour shortages and component disruption issues earlier?

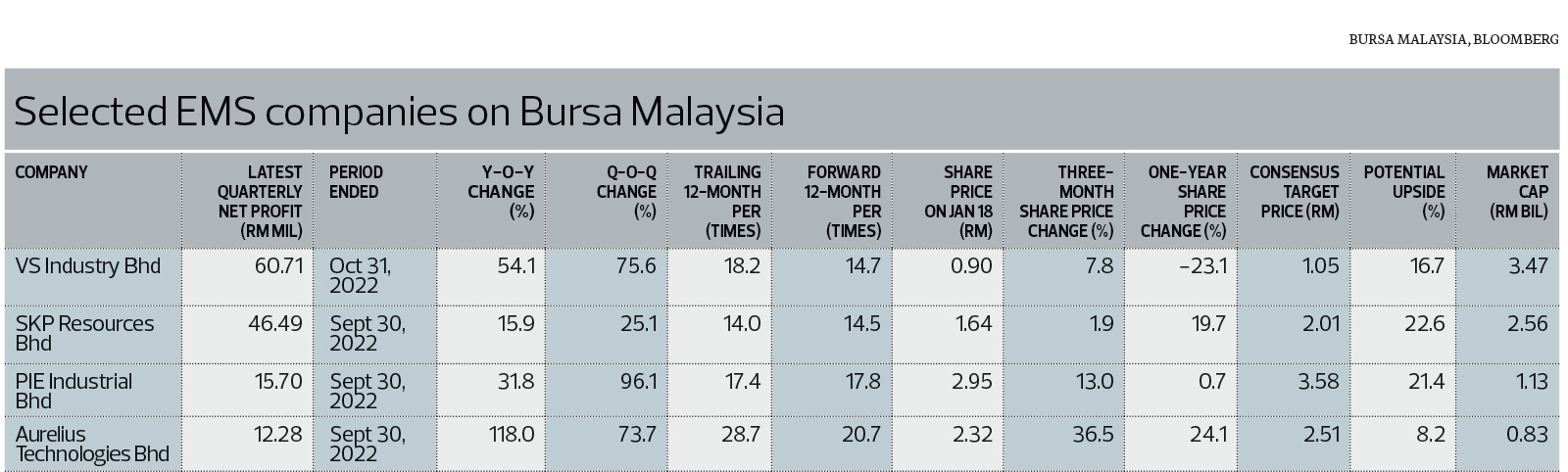

At a glance, almost all EMS stocks have risen in the past three months, with Aurelius Technologies Bhd registering the highest gain of 36.5%, followed by PIE Industrial Bhd (+13%), VS Industry Bhd (+7.8%) and SKP Resources Bhd (+1.9%).

Betamek Bhd, however, has seen its share price slip 3% since it debuted on the ACE Market of Bursa Malaysia with a listing price of 50 sen last October.

An analyst with a non-bank-backed research house, who declined to be named, stresses that investors have to be more selective in picking EMS counters. He favours those that have more exposure to non-consumer electronic products.

“Since last year, demand for consumer electronic products has been soft and we believe demand for this segment will remain soft this year,” he tells The Edge.

Taking NationGate as an example, he notes that the company derives less than 1% of its revenue from the consumer electronics segment as it is significantly exposed to the industrial segments, including the sub-segments of data centres and telecommunication.

NationGate is one of the best-performing initial public offerings (IPOs) in recent years, rising to a high of RM1.17 last Tuesday against its IPO price of 38 sen a share. The company is focused on the assembly and testing of electronic components and products to produce completed printed circuit boards, semi-finished sub-assemblies and fully assembled electronic products as well as semiconductor devices.

At last Wednesday’s closing price of RM1.14, it had already exceeded research houses’ target prices that ranged from 54 sen to 98 sen.

Explaining the reason behind the strong interest in NationGate, the analyst says the company provides more value-added services such as chip-on-board processes that are typically seen only among outsourced semiconductor assembly and testing (OSAT) players.

Cape EMS Bhd is the upcoming EMS listing in the first quarter of the year, having signed an underwriting agreement with Hong Leong Investment Bank Bhd and AmInvestment Bank Bhd for its IPO last week.

The analyst prefers PIE, which has exposure to both the consumer and industrial segments. In comparison, SKP Resources Bhd is very much dependent on consumer electronics.

“I’m not saying SKP Resources won’t do well, but there will be less excitement on its investment in the consumer segment,” he says.

One of PIE’s strengths is its vertical integration capabilities in a wide range of components, including printed circuit board assembly, injection moulding, lens, cable and wire, metal stamping and box assembly. It has more than 50 customers, with 10 key ones accounting for more than 90% of sales revenue.

SKP Resources is involved in the manufacturing of plastic components, precision mould making, advanced secondary processes, sub-assembly of electronics equipment and full turn-key contract manufacturing.

Meanwhile, Mercury Securities analyst Ronnie Tan says Aurelius Technologies is one of his top picks, given its high capabilities and technical know-how, being able to serve a diversified set of customers. He estimates that the company’s performance in the second half of the financial year ending Jan 31, 2023, will be stronger on the back of higher contribution from a customer as a result of increased order uptake due to the commissioning of additional new surface mount technology lines for this customer.

Tan says, “Margins for this customer will be relatively higher with the consignment of raw materials.”

To address the constraint in the manufacturing floor space and continued business growth through the acquisition of four new customers in FY2023, Aurelius Technologies intends to build a new manufacturing plant, which will house another 165,000 sq ft of manufacturing floor space, more than double the capacity of its existing space.

Overall, Tan expects the EMS sector to experience robust growth driven by capacity expansion and strong order flows. It also benefits from the US-China trade war, which has prompted many companies to relocate to Southeast Asia.

Despite ongoing labour shortages, he highlights that more companies have been investing in technology to upgrade their manufacturing facilities towards industry 4.0, which involves the automation of production lines for business operations. This will increase productivity and allow for better control over labour costs.

In a December 2022 research note, Maybank Investment Bank Bhd upgraded the EMS sector to “positive” from “neutral”, as it believes that value in the sector has emerged, alongside signs of a stabilising macroeconomy, a slowdown in interest rate hikes and an expectation of a mild recession — as opposed to a hard landing — for developed countries. This is given that countries in the West are the main source of consumption of EMS firms’ locally assembled products.

Nonetheless, an analyst from a bank-backed research house cautions that demand may still be challenging for the EMS sector.

“SKP Resources is our only ‘buy’ in the sector. We believe its earnings are relatively more resilient, judging from its customer profile, while the new production lines commencing this year will translate into earnings growth for the company,” he says.

Taking into consideration the concern over a slowdown in the global economy, which could lead to a material cut in orders, he thinks valuations for EMS counters are not too demanding at this point.

Bloomberg data shows that Aurelius Technologies is trading at the highest valuations, with trailing 12-month and forward 12-month price-earnings ratios of 28.7 times and 20.7 times respectively. This compares with 14 times and 14.5 times respectively for SKP Resources — the lowest among the key EMS providers.

In terms of share price, SKP Resources and PIE offer the highest potential upside, at 22.6% and 21.4% based on the consensus target prices of RM2.01 and RM3.58 respectively.

PIE — No sign of slowdown in demand

Meanwhile, PIE continues to receive new enquiries despite talk of a global recession and waning demand.

“We’ve seen no signs of a slowdown in our business. A lot of people have been talking about the recessionary outlook, but we still can expect growth. We hope that both earnings and sales can grow another 15% this year,” managing director Alvin Mui Chung Meng tells The Edge.

In the first nine months of 2022, PIE’s net profit expanded 18.1% year on year to RM42.8 million, from RM36.2 million. The fourth quarter is typically the strongest for PIE.

Mui says the company’s target this year is to expand its profit margins.

“Although we have received a lot of new enquiries, we have to be careful to ensure that we pick the best customer as we have limited resources. We want to maximise our available resources for the best,” he says, noting that its net margins are hovering at 5% to 6%.

While the labour shortage was the key issue that PIE faced last year, Mui says the situation has improved this year with the faster approval process for foreign workers.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments