Brokers Digest: Local Equities - Consumer, Sime Darby Plantation Bhd, Tasco Bhd, Techbond Group Bhd

Consumer

OVERWEIGHT

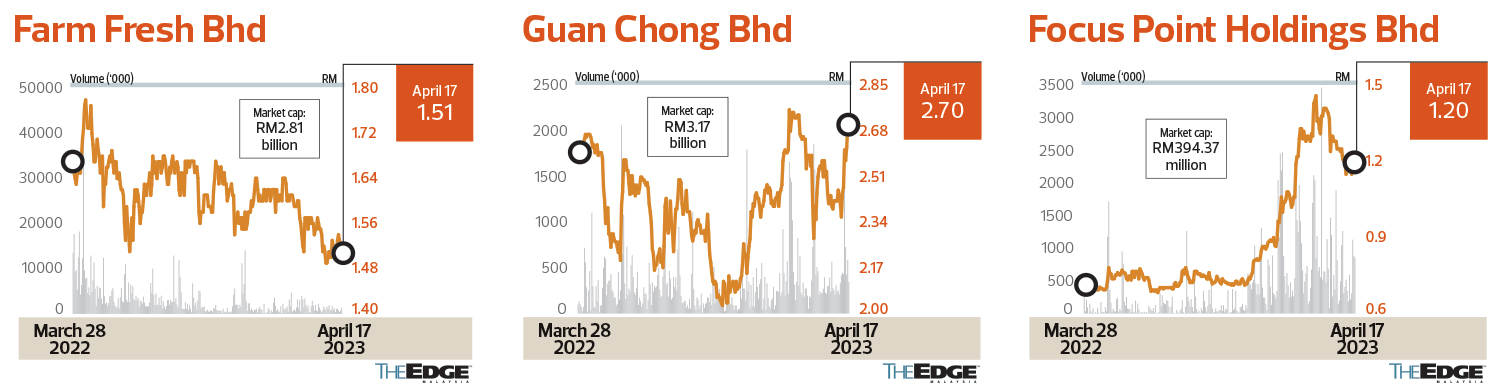

UOB KAY HIAN (APRIL 13): During UOB’s Consumer Day — attended by Farm Fresh Bhd, Guan Chong Bhd and Focus Point Holdings Bhd — the outlook was generally positive with expansion efforts driving growth in each respective industry, more than offsetting creeping costs. In a similar vein, decent earnings visibility from softened commodity prices anchors our “overweight” call on the sector. The sector is also trading below its five-year mean while offering resilient and attractive growth.

Farm Fresh’s midstream processing expansion at Muadzam Shah, Pahang, has come on stream. This should be accompanied by the expansion in Taiping on April 23. This combined expansion lifts overall production throughput by 30% and should relieve its supply-constrained sales. The expansion in the Philippines should commence operations in 3Q2023 while its key new product, growing up milk powder, is due to be launched in 4Q2023.

Guan Chong’s operations in Germany are expected to perform significantly better with the halving of energy costs amid higher sales. Its nascent operations in Ivory Coast and its UK operations should at least break even this year. Overall, Ebitda yield should trend positively heading into 2H23 on the back of recovering volume and ASPs.

Focus Point expects its bakery segment to be the key earnings driver for this year, lifted by the onboarding of its corporate customers in 2H2023. Its optical segment should realise growth as well, albeit more gradually, arising from the roll-out of new stores and positive SSSG. Next year could offer better prospective growth following the full on boarding of its corporate bakery customers by then.

While potential tightened spending from inflationary pressures, recessionary fears and potentially lower subsidies are already present or emerging, they are outweighed by: (i) valuations that are trading below mean, backed by double-digit earnings growth of 12.3%; (ii) diminishing inflationary pressure, including commodities and logistics costs that have a direct and significant impact that clouded earnings visibility previously; and (iii) our preference being skewed towards staples (Fraser & Neave Holdings Bhd, Heineken Malaysia Bhd and British American Tobacco (Malaysia) Bhd, which command resilient demand amid a potential downward shift in the economy, including quasi-staples such as Mr D.I.Y. Group (M) Bhd which managed to grow sales even throughout the pandemic.

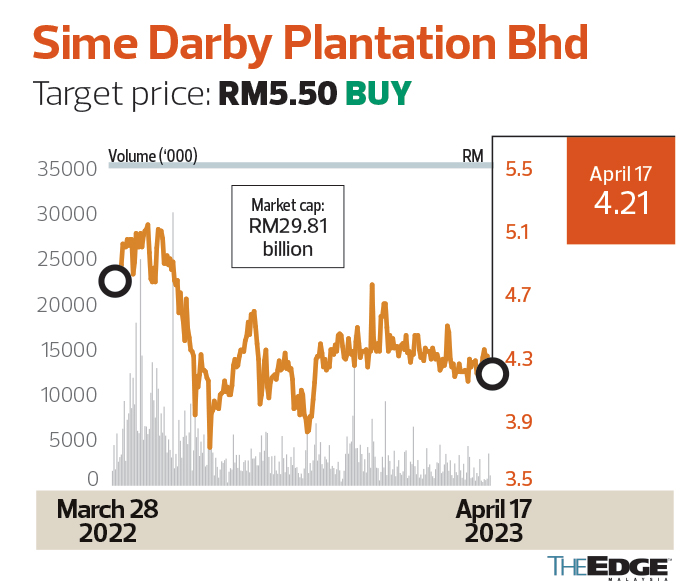

Sime Darby Plantation Bhd

Target price: RM5.50 BUY

MIDF RESEARCH (APRIL 17): On April 14, SDPL entered into two conditional share sale and purchase agreements (CSPAs) with PT Global Berkat Usahatama for the disposal of a 100% stake in PT Ladangrumpun Suburabadi (LSI) and PT Sajang Heulang (SHE) for RM518 million in cash. We are “neutral” on this latest development as this is in line with the company’s internal reorganisation of its non-core operations. There will be a net gain on disposal amounting to RM107 million in FY23 but we are excluding it from our earnings forecast. Proceeds derived from the disposal will be utilised for working capital, based on management guidance.

Overall, we remain bullish on the SDPL outlook due to: (i) a fresh fruit bunch yield and maturity of 16.6 tonnes per hectare, which ranks among the top tiers; (ii) a fairly prime palm tree age profile of 12.1 years, which is still impressive given the company’s large planted area; and (iii) a well-integrated operation where the manufacturing segment, which accounts for roughly 26% of group profit, will help withstand and slow the decline in the ASP for crude palm oil, thus lowering the volatility of earnings.

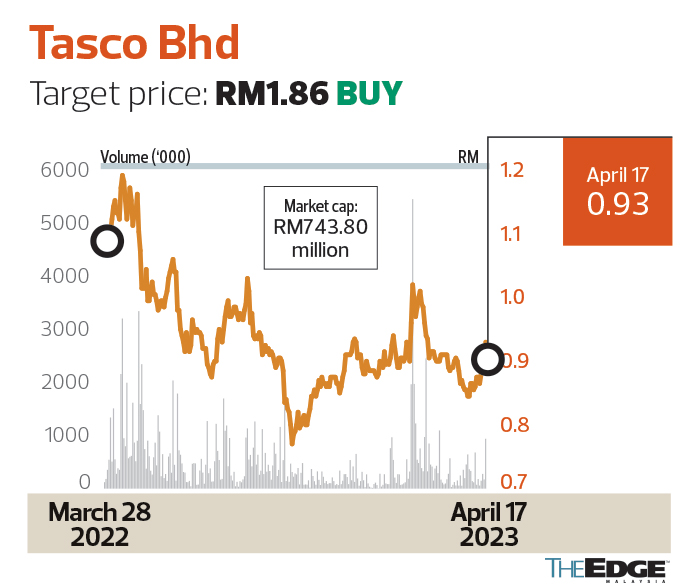

Tasco Bhd

Target price: RM1.86 BUY

RHB RESEARCH (APRIL 17): Following our site visit to Tasco’s Shah Alam Logistics Centre (SALC) in Selangor, we came away reassured of its earnings visibility, amid overdone concerns on freight rates. We believe it will continue to book record earnings again in FY23 by delivering a 4QFY23F bottom line of RM20 million to RM25 million. This would meet our estimate, on top of a potential final dividend payout ratio of 30%. We are also positive on the progress of Tasco’s warehousing and cold chain segment in terms of its expansion plan and new business wins.

The progress of the much-anticipated 600,000 sq ft SALC is on track, and Tasco expects to hand over rental space to its electrical & electronics and retail customers in January 2024. There is another 400,000 sq ft of leasable space under the SALC-Phase 2 expansion in the works. It is in its design stage, given the scarce supply and higher demand for warehouse space in the vicinity. Meanwhile, its new 250,000 sq ft West Port Logistics Centre expansion is expected to be completed by November, in time to cater to a new customer.

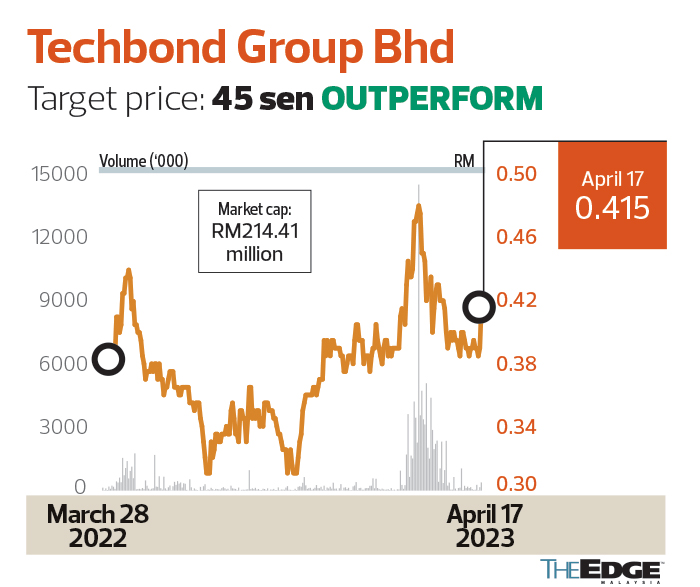

Techbond Group Bhd

Target price: 45 sen OUTPERFORM

KENANGA RESEARCH (APRIL 17): We initiate coverage on Techbond with an “outperform” call and a target price of 45 sen based on a 13.5-time forecast for CY24 EPS of 3.4 sen, in line with international peers in the adhesive sector.

Techbond is a business-to-business adhesives solution provider. The group caters mainly to the timber panel and wooden furniture sectors as well as the fast-moving consumer goods sector. Its markets, in order of size, are Vietnam, Malaysia and Indonesia.

Techbond has multinational, local and regional customers and enjoys strong customer retention. The group’s recent acquisition of Malaysian Adhesives and Chemicals (MAC) from PPB Group Bhd provides the opportunity to penetrate new segments. MAC’s adhesive products are used further upstream, catering to the production of chipboard, particle board and paper carton packaging.

The group is now aiming to leverage its market expertise and existing client network to increase MAC’s market share in the space.

Meanwhile, its new polymerisation plant in Vietnam produces polymers used as inputs for adhesive production.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| BAT | 8.220 |

| F&N | 31.520 |

| FFB | 1.500 |

| FOCUSP | 0.715 |

| GCB | 2.710 |

| HEIM | 23.020 |

| KENANGA | 1.080 |

| MRDIY | 1.520 |

| PPB | 15.940 |

| SIMEPLT | 4.440 |

| TASCO | 0.830 |

| TECHBND | 0.430 |

Comments