Worse likely to come for semicon sector, say analysts

KUALA LUMPUR (May 3): Dismal quarterly results from both Unisem (M) Bhd and ViTrox Corp Bhd — bellwethers of the local semiconductor sector — have set a rather gloomy tone for their peers.

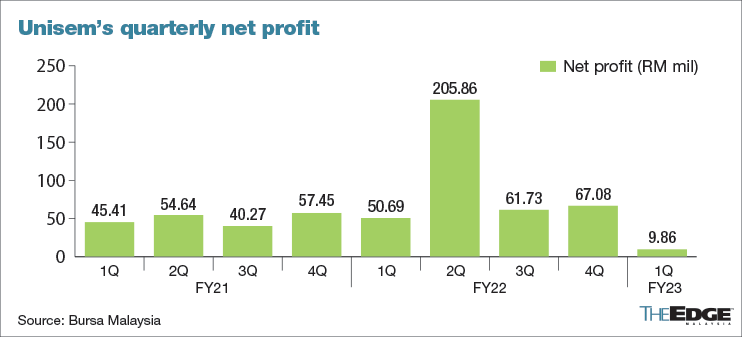

Unisem, one of the largest outsourced semiconductor assembly and test (OSAT) players in Malaysia, reported last Thursday (April 27), a net profit of just RM9.86 million for the first quarter ended March 31, 2023 (1QFY2023) — down 80.5% year-on-year (y-o-y) and 85% quarter-on-quarter (q-o-q) — making it the group’s weakest quarterly performance since 1QFY2020, when it posted a net loss of RM2.83 million. The weaker earnings were attributed to lower sales volume, which the group said was in line with “softer market conditions”.

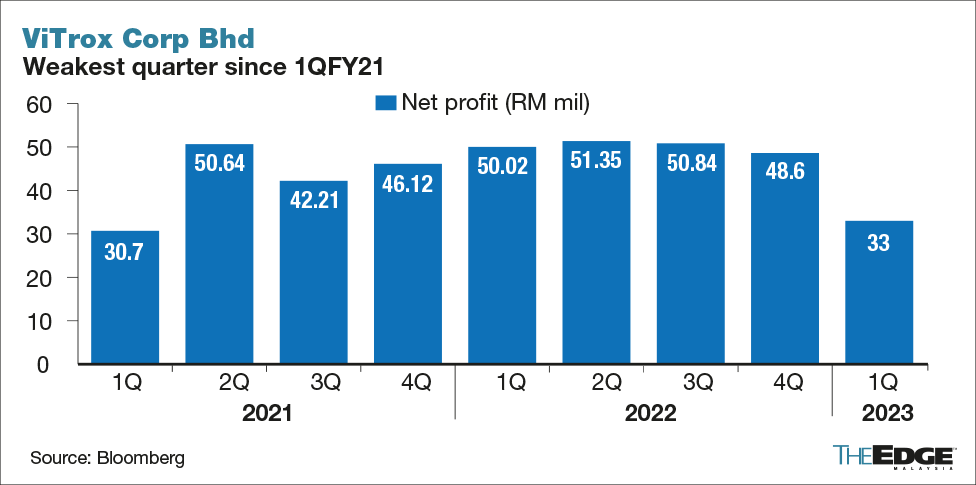

Similarly, ViTrox, the largest automated test equipment (ATE) firm in the country, also posted a lower net profit of RM33 million for 1QFY2023 — its weakest quarterly performance in two years, following the RM30.7 million it made in 1QFY2021.

The group’s 1QFY2023’s earnings were down 34% y-o-y and 32% q-o-q, mainly because the previous year saw a taxation provision reversed following the extension of pioneer status for its wholly owned ViE Technologies Sdn Bhd. This was coupled with lower demand for its machine vision systems amid a global semiconductor downturn.

This was followed by Globetronics Technology Bhd reporting on Tuesday (May 2), a 65% drop in its first quarter net profit to RM3.3 million, as revenue fell amid lower volume loadings from its customers, higher tax expense and forex losses. The group even issued a profit warning for the year, as it forecasts softer revenue ahead and rising costs.

Unisem and Vitrox, on the other hand, indicated that the downturn may be short-lived, as they expect to soon see improvements in their respective results.

Unisem directors expect the group’s performance to improve by the next financial quarter, despite the soft demand seen for its products and services in 1QFY2023. ViTrox is “cautiously optimistic” about its prospects for the second half of 2023, despite operating in a challenging environment, and is focusing on preparing for a “strong rebound in the near future”.

Globally, the sector’s downturn is marked by the quarterly losses reported by semiconductor giants like Intel Corp, Samsung Electronics Co and memory chip maker SK Hynix Inc.

Samsung expects the global tech industry to begin emerging from its downturn later this year, while SK Hynix said production cuts by memory chip makers will improve market conditions from the second half of 2023.

Against this backdrop, will things get worse before they get better for the semiconductor sector? Market experts whom The Edge contacted, by and large, think so.

Kenanga Research analyst Samuel Tan said the semiconductor sector’s prospects remain challenging until year end, given the macroeconomics headwinds, including weak consumer sentiment, that have a negative impact on demand for consumer electronics products.

“While the market expects the operating environment for the semiconductor sector to improve by the second half of this year, I am not expecting it to be a sharp recovery. The situation may only start to pick up by the end of this year, followed by a gradual recovery next year,” Tan said.

Fortress Capital Asset Management CEO Thomas Yong said the semiconductor sector’s prospects are hard to tell at this juncture because he is seeing mixed guidance from sector players.

“Some sector players are predicting that 1H2023 [first half of this year] will be the current cycle’s bottom, while some are alluding that it might drag further into 3Q2023 [third quarter this year]. So far, we have seen more negative guidance than positive ones from the sector’s bellwethers,” said Yong.

Hence, Yong expects potentially poorer results to come in 2Q2023, compared to 1Q2023. “The semiconductor sector is still facing some headwinds, especially from the automotive sector, which has been doing relatively well all this while versus the broader semiconductor sector,” he noted.

Having said that, Yong said things may play out differently for each player, depending on their supply chain and geographical exposure. “For instance, ViTrox derives about 30% of its revenue from China and has significant exposure to the telecommunication sector, which could potentially cushion softness from other sector exposures,” Yong said.

Meanwhile, any weaker-than-expected performance — from lower utilisation rates and further delivery push-out by customers, to higher raw material and labour costs — could be a negative catalyst for local semiconductor players.

On the flipside, upsides could come from a stronger-than-expected China recovery and mounting US-China technology conflict, the latter of which could provide positive spillover effects to the local semiconductor sector.

“China is also stimulating its semiconductor sector with huge stimulus packages. This can be another catalyst for our Malaysian tech players, especially for those with significant and established exposure to the country,” Yong added.

Notwithstanding the challenging and downbeat near-term outlook, certain quarters believe there are still pockets of opportunities for investors to look for among semiconductor counters.

According to Areca Capital Sdn Bhd CEO Danny Wong Teck Meng, the negative news has already been priced in. Hence, selected counters in the semiconductor sector “look decent to accumulate for recovery” in 2H2023 or next year.

“The other influencing factor for the tech sector is the end of the rate hike cycle; perception is that it will normalise over the next few quarters — a positive factor for tech valuation,” he added.

“I am confident [that] 2H2023 will be better than 1H2023 because aggressive destocking (started in 2H2022) of inventory by industry players or their customers will be done by 1H2024. When inventory levels normalise, orders from players and customers will recover. However, it is uncertain whether the 2H2023 recovery will be U or V shaped. That depends on the macro,” said Wong.

Unisem’s ‘bombshell’ 1QFY2023 results

Investment analysts who track Unisem have either downgraded or reaffirmed their “sell” recommendation on the OSAT firm, saying the group’s 1QFY2023 results were below their expectations.

RHB Investment Bank Research downgraded Unisem to “neutral”, with a lower target price of RM2.86 (from RM3.80). Post-1QFY2023 results, the research outfit cut its forecast for Unisem’s FY2023 earnings by 27% to RM196 million, for FY2024 by 9% to RM291 million, and for FY2025 by 8% to RM331 million, after factoring in lower loadings and lower margin assumptions.

“While we believe the numbers are set to improve with better utilisation moving forward, we are unsure of the pace of recovery into 2H2023 — it may not reach optimal utilisation rates due to its expansion plan,” the research outfit’s analyst Lee Meng Horng said in a note last Friday (April 28).

Kenanga Research’s Tan has likewise slashed his earnings forecast for Unisem by a whopping 42% in FY2023 to RM143.2 million. He also cut the earnings forecast for FY2024 by 19% to RM223 million.

Describing Unisem’s 1QFY2023 results as a “bombshell”, with its core net profit of RM9.9 million, Tan said this is way below expectation and accounted for only 4% of both his and consensus’ full-year estimate.

Tan also lowered his target price for Unisem to RM2.75 from RM3.10, but kept his “market perform” recommendation.

He also noted that he remained cautious about Unisem’s path to recovery, as there will be new capacity coming-in in 2HFY2023, which may further increase operating costs.

“In Chengdu [China], its phase three plant (which doubles the capacity of phases one and two combined) has been completed and is in the midst of qualifying customers in phases. Meanwhile, its new plant in Gopeng [Perak] is expected to be completed by November 2023, with the onboarding of customers to only take place in 1QFY2024,” Tan wrote in a research note.

TA Securities made the least change to its earnings estimate for Unisem, as its earnings forecasts were lower than the others. It trimmed its forecast for FY2023 by just 1.4% to RM155.2 million, and for FY2024 by only 0.8% to RM191.4 million.

Notwithstanding the seasonally weaker 1QFY2023, TA Securities expects Unisem to see sequential improvements, underpinned by a recovery in demand and operating leverage. The group, it noted, also sees upside from customers adopting a “China Plus One” strategy, given its presence in both Malaysia and China.

Still, TA Securities, who kept its “sell” call on Unisem with an unchanged target price of RM2.40, said it remains cautious about Unisem’s near-term outlook amid the slowdown from the consumer, communications, and personal computer market segments. These segments accounted for 65% to 71% of Unisem’s revenue from FY2018 to FY2022.

Of the nine analysts tracking Unisem, based on Bloomberg data, three rated it a “sell”, four had it on “hold” and two gave it a “buy”, with an average 12-month target price of RM2.75 — which represents a 6% downside from Unisem’s closing price of RM2.93 on Tuesday (May 2).

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments