WCT’s stock slumps as pandemic hits operations

IN November 2016, Tan Sri Desmond Lim Siew Choon acquired 245.71 million shares or a 19.67% stake in WCT Holdings Bhd, forking out RM2.50 a share or RM614.27 million. The acquisition price was a 42.85% premium (75 sen) to the prevailing share price of RM1.75. Lim was appointed executive chairman while Datuk Lee Tuck Fook and Peter Chow Ying Choon took up the managing director and deputy managing director posts respectively.

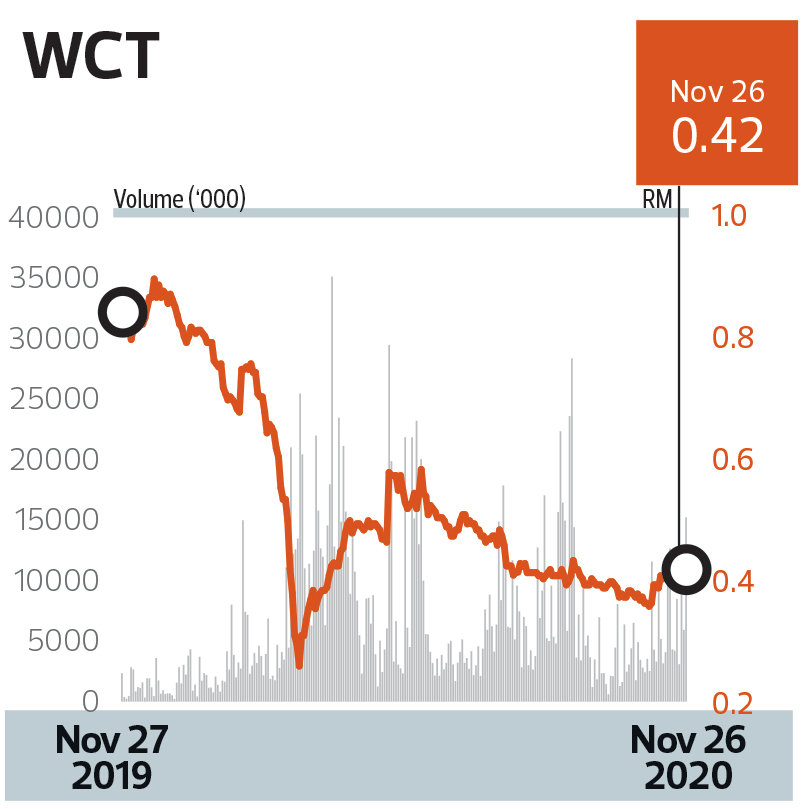

But things have not been plain sailing for Lim and WCT. To put things in perspective, the stock closed at 42 sen last Wednesday, giving the company a market capitalisation of RM588.53 million and Lim’s 25.14% equity interest a market value of RM147.96 million — down 76% from the price he paid for his 19.67% stake.

Meanwhile, WCT’s net asset per share was RM2.23 as at Sept 30. Over the past four years, the stock has averaged RM1.08 apiece — way below the RM2.50 per share that Lim paid. Meanwhile, the company has paid out only 2.9 sen per share in dividends since Lim took over the reins.

While analysts say the company is less aggressive in tendering for projects compared with four years ago and has lost some of its lustre, construction industry players beg to differ. They say WCT is a participant in every significant bid in town and its tender prices are very competitive.

Attempts to speak to Lim’s generals for this article did not bear fruit.

Apart from WCT, Lim has a 39.36% stake in property developer Malton Bhd and 27.8% in Pavilion Real Estate Investment Trust (REIT). Thus, his entry into WCT generated considerable excitement, as other than a construction arm, the company also had a property development division and a number of malls under its umbrella — the Paradigm Malls in Petaling Jaya and Johor Baru and the Bukit Tinggi Shopping Centre in Klang, leased to Aeon — which were deemed a good fit with Malton and Pavilion REIT.

Other assets owned by WCT are the New World Hotel in Petaling Jaya and Premier Hotel in Klang. Unfortunately, all the assets and businesses under WCT — hotels and malls, construction and property development — have been adversely impacted by Covid-19.

One market watcher tries to explain Lim’s predicament. “Desmond is a long-term investor, so he is not very perturbed by the share price. Generally, you are only concerned about the share price if you are looking to sell,” she says, adding that it is not just WCT that has been out of the limelight. Construction players such as Gamuda Bhd and IJM Corp Bhd have also been flying under the radar.

“It’s a construction industry issue. There have been only a few jobs available,” she explains. Then again, Gamuda is trading at RM3.67 per share and IJM at RM1.65, both above the penny-stock level that WCT is in.

In a report on WCT last week, Public Investment Bank notes, “The pandemic appears to have weakened the group [WCT] more notably than others … While WCT’s outstanding order book appears healthy at around RM5 billion, we foresee the group may face some challenges in project execution given the new norms.

“The award of new contracts also remains uncertain given the current operating climate. Its high financial commitments and de-gearing exercise, made more challenging by the weak operating conditions, will limit its growth potential.”

Public Investment Bank has a “neutral” call on WCT, with a 12-month target price of 44 sen.

It is noteworthy that WCT’s current share price has been bolstered by share buybacks. The company has 14.94 million treasury shares and recently undertook a dividend payout of 13.95 million shares, distributed to investors in August. Had it not been for these buybacks, the stock would likely have been more depressed than the current levels.

WCT’s share price hit a 52-week low of 24.3 sen on March 19, but has since gained some traction, trading above the 40 sen band. This is notably way below its net asset per share of RM2.23 as at Sept 30.

Last week, after WCT’s financial results were announced, Hong Leong Investment Bank maintained its “hold” call on the company, with a target price of 42 sen, down from 44 sen previously. “Our target price is derived based on a 40% discount to sum-of-parts value of 70 sen. Our target price implies FY2020/21/22 price-earnings multiples of 59.7 times, 10.9 times and 9.3 times [respectively]. While the stock trades at a low price-to-book value of 0.19 times, we reckon it is reflective of WCT’s weak earnings prospects and fragile balance sheet.”

For the nine months ended Sept 30, WCT saw its net profit drop 87.9% to RM9.24 million from RM76.3 million a year ago, largely due to the Covid-19 pandemic. According to analysts, the company distributed RM24.3 million to holders of its perpetual sukuk, which also adversely impacted its bottom line. Revenue was lower at RM1.16 billion compared with RM1.33 billion a year ago.

As at end-September, WCT had cash and bank balances of RM600.68 million. On the other side of the balance sheet, it had long-term borrowings of RM1.9 billion and short-term debt commitments of RM924.29 million. It also had RM817.9 million in perpetual sukuk on its books.

While WCT’s current order book is in the region of RM5 billion, a chunk of it is from the construction of Pavilion Damansara Heights. According to a report in mid-November, Hong Leong Investment Bank put the outstanding contract value for Pavilion Damansara Heights Phase 1 at RM1.6 billion and Phase 2 at RM1.2 billion, or more than 50% of WCT’s outstanding order book.

In its defence, an executive director at a rival construction company says WCT bagged a RM555 million contract in July 2018 for the development of a mixed-use commercial property project at Tun Razak Exchange from Lendlease Projects (M) Sdn Bhd. “We had also bid for the same job, and we were already very competitive, but they beat us to it.”

He adds that in December 2018, WCT and its partner TSR Capital Bhd won the contract for the construction of an eight-storey mall at the KL118 project valued at RM676.8 million, once again beating a bid by his company. “Collectively, these two jobs are worth more than RM1.2 billion. They beat us to both contracts and have been bidding for every big [project].”

If this is the case, will things pick up for WCT?

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments