Brokers Digest: Local Equities

CIMB Group Holdings Bhd

Target price: RM5.20 BUY

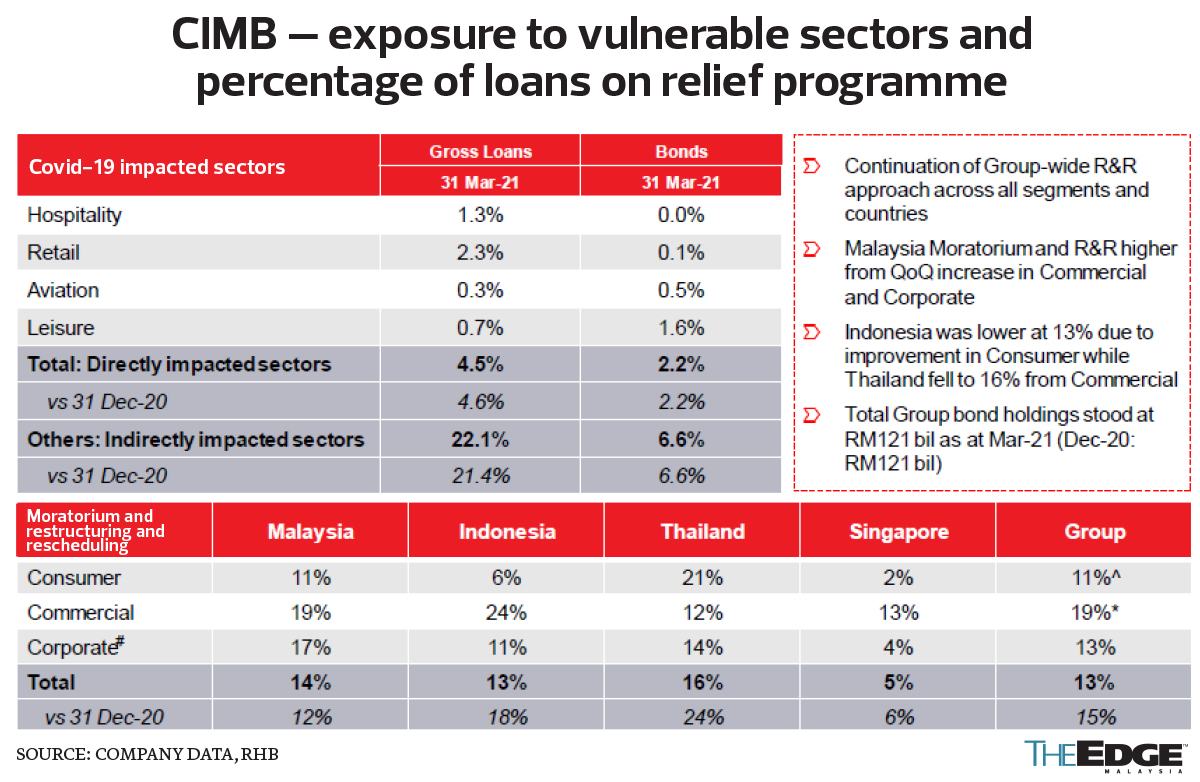

RHB INVESTMENT BANK (JUNE 1): CIMB’s 1Q21 core Patami beat expectations on better net interest margin (NIM) expansion and lower-than-expected credit cost. Most guidance is maintained except for NIM, which is revised up on a better current account, savings account (CASA) mix. We are encouraged by CIMB’s progress in reviving its return on equity (ROE) and most indicators point to the group being well on track in its transformation plan. Our target price values CIMB at an FY21 P/BV of 0.9 times.

Downside risk from the latest round of lockdown was highlighted, but credit cost guidance was kept at 80 to 90 basis points (bps) for now. Management also referred to some kind of assistance programme (via banks) that the government will potentially introduce shortly, which could have an impact on CIMB as well. Such conservatism prompted management to keep its ROE target at 6% to 7% even though ROE came in at more than 9% in 1Q21. Loan growth will likely be muted as a result of the continuous portfolio optimisation exercise.

Excluding the RM1.156 billion one-off revaluation gain from the deconsolidation of TnG Digital, CIMB delivered RM1.301 billion in core Patami during 1Q21, which beat our and consensus’ forecasts. Core ROE rebounded to 9.3% from 2.1% in FY20.

As at end-March, 13% of its loan book was on a relief programme, down from 15% as at end-December. Its Malaysian loan book saw a higher relief portion of 14% (December: 12%), mainly due to an oil and gas corporate borrower whose bond was restructured into a loan. Loans were up 0.2% quarter on quarter (q-o-q), mostly driven by 1.4% growth in mortgages. Asset quality was fairly stable q-o-q, with the gross impaired loan ratio at 3.4%. Deposits were up 0.1%, mostly on CASA growth. The CASA ratio stood at 42.3% (4Q20: 41.3%). Following the deconsolidation of TnG Digital, it will now be accounted as an associate in CIMB’s books — a net positive impact, given TnG Digital’s annual loss of about RM150 million.

We maintain our “buy” call, with an unchanged target price of RM5.20, offering an upside of 22% and a dividend yield of about 4%.

British American Tobacco (M) Bhd

Target price: RM15.70 SELL

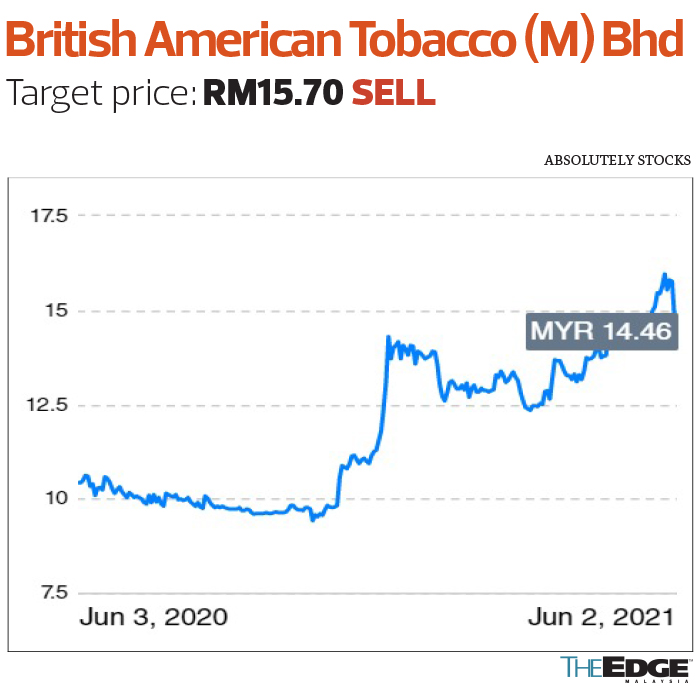

TA SECURITIES (JUNE 1): Implementation of Budget 2021 measures in tackling the illicit cigarette trade alongside the embarking of legalisation and regulation of vape products has started to yield early success, leading to a legal industry volume recovery of 19% year on year (y-o-y). Nevertheless, management says the government needs to remain agile as syndicates are quick to change their modus operandi to circumvent any clampdown.

The third Movement Control Order (MCO 3.0) is expected to negatively affect the operations of BAT. Furthermore, duty-free sales will remain subdued for the rest of FY21, given that international travel restrictions are still being enforced in Malaysia.

BAT’s cost base is now leaner post-completion of restructuring efforts throughout FY20. We expect parts of the savings could be allocated to strategic brand investments, which would enhance BAT’s brand awareness.

Following the jump in share price, we recommend that investors take profit, as we reckon BAT’s recovery may take a breather amid the implementation of MCO 3.0. As such, we downgrade BAT to “sell” from “buy” previously, with an unchanged target price of RM15.70.

Bonia Corp Bhd

Target price: RM1 ADD

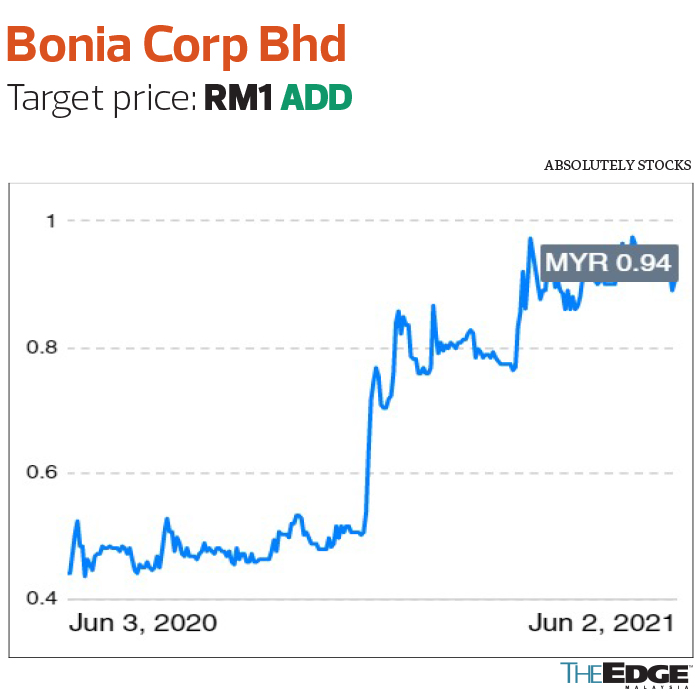

CGS-CIMB RESEARCH (JUNE 1): We expect the demerger of SBG Group (mostly retails the Sembonia brand) and its subsequent listing on the LEAP Market to be completed sometime in 3QFY22. We retain our neutral to slightly negative view of this exercise as the benefits of having different platforms to optimise strategies and capital management for specific brands would be offset by the lower liquidity in the LEAP Market compared with Bursa Malaysia’s Main and ACE Markets.

We slightly raise our FY21 EPS forecast, as we lower our revenue assumptions, but lift our margin forecast in the light of 9MFY21 earnings beating consensus. We retain our “add” call on the stock, with an unchanged target price of RM1, still based on FY22 P/BV of 0.5 times. Notwithstanding the challenges to retailers, we remain positive on Bonia’s improving profitability and disciplined cost management. Key rerating catalysts include faster-than-expected sales recovery. Key downside risks are a prolonged nationwide lockdown, higher-than-expected operating costs and intensifying competition.

Johore Tin Bhd

Target price: RM2.25 OUTPERFORM

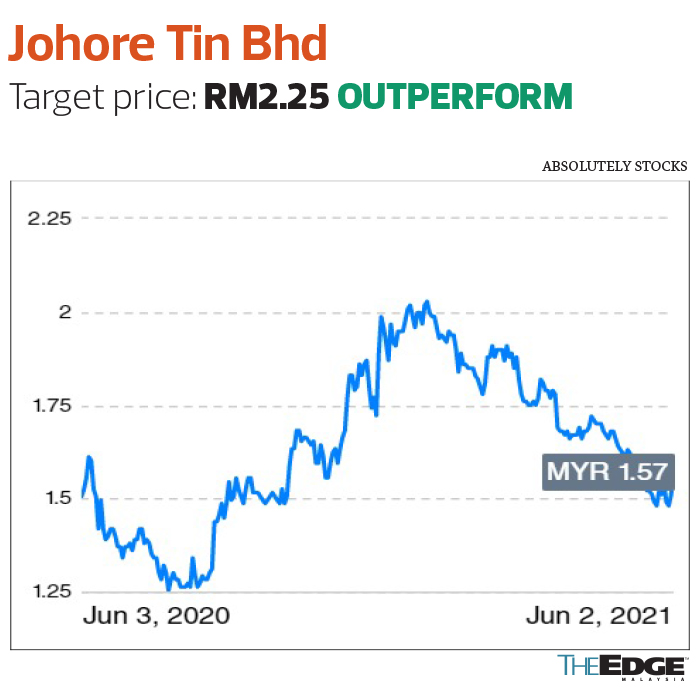

PUBLICINVEST RESEARCH (JUNE 1): Johore Tin’s net profit jumped 109% y-o-y to RM9.5 million in 1QFY21, likely attributable to the normalised margin in the tin manufacturing segment following the adjustment of selling price. After adjusting for one-off items, its 1QFY21 core net profit came in at RM10 million. The results were within expectations, accounting for 20% and 22% of our and consensus’ full-year estimates respectively. Nevertheless, we are adjusting our forecast for FY21-23 downwards by 3% to 7% to account for MCO 3.0 impact, as the company is only allowed to operate at 60% capacity, coupled with the increase in raw material costs. We are still positive on its long-term outlook as its Mexico operations should enable the company to tap the North American market.

We maintain our “outperform” call, with a higher target price of RM2.25 — up from RM2.08 previously — as we roll forward our valuation base year to FY22 EPS. For the quarter, Johore Tin declared a single-tier interim dividend of one sen.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments