Strong vehicle sales to benefit HIL Industries’ automotive segment

FAMILY-run HIL Industries Bhd has not been getting much investor attention over the years. As a one-stop plastic solution provider, its plastic component products are widely used in the automotive, electrical and electronics (E&E) and telecommunications and information technology (IT) industries.

Major local and foreign marques have been its key customers. Buoyed by strong car sales, the company expects better performance ahead, barring any persistent lockdown.

“Based on our customers’ forecasts and our yield model, we expect to do very well in 2022. We are even expecting to do better this year compared with last year … Our internal target is always to at least grow revenue by 20% per annum,” HIL Industries managing director Datuk Milton Norman Ng Kwee Leong tells The Edge.

He says orders from its major customers, especially Perodua, have been very high, underpinned by the extension of the sales tax exemption for vehicles. However, the recent Full Movement Control Order has affected the automotive industry, which is not considered an essential industry.

“In previous years, we did 10 to 16 parts for every Perodua car, but starting from two years ago, it has gone up to 38 to 40 parts per model for Aruz and Ativa, as we are giving out more value-added products,” he adds.

Besides Perodua, its other customers include Toyota, Honda, Proton and Volkswagen, according to him.

“We are one of the pioneers in the plastic manufacturing industry. We are even the first vendor for Proton Saga. But eventually, we moved more towards Perodua because we like the way its system is managed.

“Perodua provides a lot of vendor development programmes. When our skills are well developed, then we can give better quality products to them,” he explains.

HIL Industries’ automotive clients are served by its two plants in Shah Alam. It is looking to expand by setting up a new plant that is closer to its clients.

To secure higher content contact, the company has also been expanding its product range. “For example, a few years ago, we formed a JV (joint venture) with Indonesian partner PT Dasa Windu Agung to undertake headlining operations. We successfully developed the product and started supplying to Perodua in 2019,” Ng says.

Being lean and efficient, he adds, is crucial to remaining competitive in the region. “The supply chain sourcing has become very global. Our products are competitive because we export to India and Brazil for Volkswagen. Even for Honda Japan and Thailand, we ship back the plastic parts to them.”

Last year, the automotive division contributed about 80% to HIL Industries’ manufacturing business, with the remaining from E&E and IT.

Following a consolidation last year due to the loss of a customer, Ng says the Penang plant, which manufactures plastics components for the E&E sector, has kick-started its operations, with the aim of ramping up production by mid-July or early August.

“We export to Western Digital in Thailand and have also secured a new customer — BYD, which is in the iRobot vacuum cleaner business.”

HIL Industries has a plant in Suzhou, China, which was set up in 2016, serving IT players such as Dell and Wistron. Due to market competition and the difficulty in getting suitable talent, the company does not plan to expand its production in China.

Overall, exports (China plant not included) accounted for 5% of its manufacturing sales last year. It is aiming for 10% overseas contribution next year.

Although the price of resin — the main raw material for its manufacturing business — has been rising in recent months, Ng says the company will not be badly hit as it can pass on the cost to customers.

HIL Industries was listed on Bursa Malaysia in 1992 following a management buyout in 1989, which saw Ng’s father Tan Sri Ng Boon Thong emerge as the largest shareholder.

Filings with the stock exchange show that the senior Tan owns direct and indirect stakes of 4.54% and 70.37% respectively.

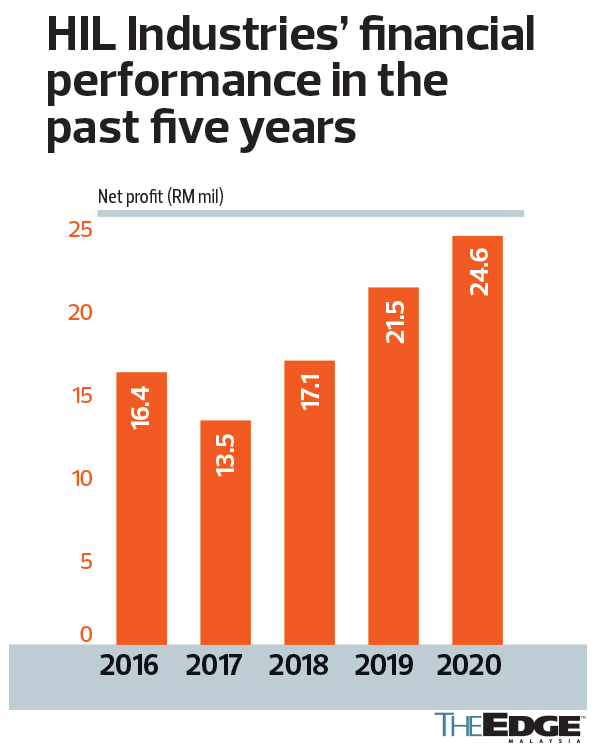

The company’s net profit grew 14.4% to RM24.6 million for the financial year ended Dec 31, 2020 (FY2020) from RM21.5 million in FY2019, driven by higher contribution from its manufacturing and property businesses. Its net profit margin also expanded to 15.1% from 13.9%.

For the first quarter ended March 31, 2021, its net earnings even expanded 50.2% to RM6.2 million against RM4.1 million in the same quarter a year ago.

The property business is equally important for the company, as Ng foresees revenue contribution from property overtaking manufacturing, going forward. In 2020, revenue contribution from the manufacturing and property segments stood at RM82.91 million and RM80.1 million respectively.

This explains why the company proposed a name change to Amverton HIL Bhd in April this year. Ng explains that its property plan is to deploy the JV model with Amverton Bhd — which is also owned by the Ng Family — to avoid heavy upfront costs.

Notably, last month, HIL Industries signed four JV agreements with Amverton to develop four landed projects in Sungai Buloh, Klang and Pulau Carey, Selangor, with a combined gross development value (GDV) of RM471.1 million.

“At the moment, we don’t have much land bank. We have over 30 acres in Melaka and a few more acres here and there. We are very asset light. We try to do JVs and acquire assets that we can turn around and launch faster,” says Ng.

On the contrary, Amverton — which was a listed company on Bursa Malaysia before being delisted in April 2020 — has a few thousand acres of land.

“We (HIL Industries) are fortunate to have them (Amverton) carry and hold the assets. When the assets are ready for development, we can either have a JV with them or acquire the land from them. Of course, if there is good land from third parties at a reasonable price, we will also look at that,” he notes.

The decision to privatise Amverton was made after taking into consideration the fact that both HIL Industries and Amverton were involved in property development. “Since Amverton was not doing so much [development], we chose to maintain the listing status of HIL Industries, which is very asset light with no liabilities.”

HIL Industries has been in a net cash position over the years, with RM101.6 million as at end-December 2020. It is planning to launch 100 townhouses (RM39 million GDV) and 125 super-link terrace houses (RM100 million GDV) under the Amverton Links 2 development in Klang. This comes after a total of 84 double-storey link units — with a GDV of RM60 million — were fully taken up.

It had unbilled sales of RM6.59 million as at end-March from Amverton Green Condo and Amverton Links, but this is expected to jump to RM60 million from 2Q onwards.

HIL Industries will continue to focus on affordable landed development in the Klang Valley, which is deemed the best property market in Malaysia.

It is worth noting that HIL Industries diversified into the personal protective equipment (PPE) segment last year, with the manufacturing of face masks and face shields. The aim, Ng says, is to tap plastic manufacturing in the medical industry.

“Although we came in late, the PPE margins are quite good. We focus on high-end surgical masks, not just the normal three-ply masks.

“We want to understand how the PPE and medical industry operate. When there is an opportunity, whether by M&A (mergers and acquisitions) or plastic parts for the medical industry, then we get ready for it. We are still actively looking for M&A,” he shares.

Its shares have slipped 12.9% since early this year and closed at 91.5 sen last Thursday, giving the company a market capitalisation of RM322.34 million.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments