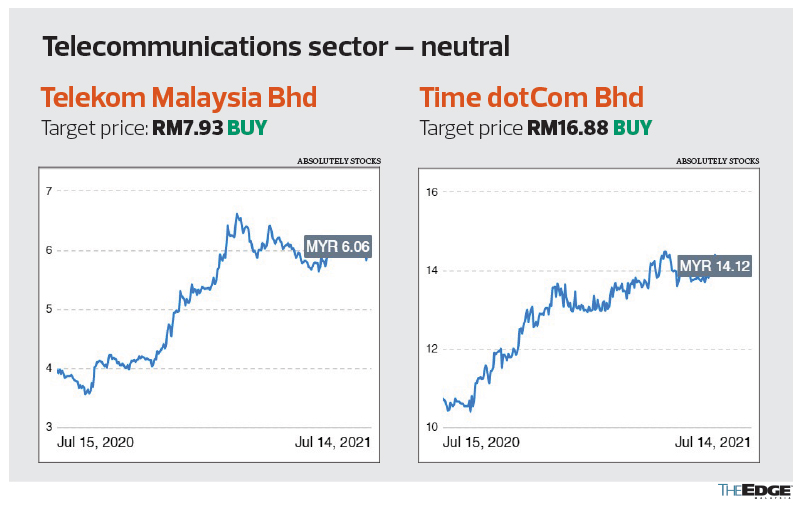

Brokers Digest: Local Equities

HONG LEONG INVESTMENT BANK RESEARCH (JULY 15): We laud the government’s move to establish Digital Nasional Bhd (DNB) to roll out a single neutral 5G infra for efficiency gain and eliminate asset duplication. After Huawei pulled out its standalone bid, Ericsson was awarded the 10-year contract worth RM11 billion to deploy around 10,000 sites along with a target to achieve 80% population coverage by 2025. The 5G network is expected to be both SA (standalone) and NSA (non-standalone) architectures on the same hardware on day one, granting full compatibility to all 5G devices in the market. NSA will be running on the most sought-after 700MHz as anchor band, taking advantage of its superior propagation feature. Meanwhile, SA will be utilising C-band (3.5MHz) as a NR (new radio) band.

Fibre is king. Its role as backhaul to transfer data at the speed of light has become ever more critical and a mandatory prerequisite in broadband/5G builds. Demand will spike not only in terms of capacity, but also coverage in order to compensate for 5G spectra (especially mmWave) shortcoming in propagation. Surge in wholesale bandwidth demand will boost margins even under MSAP (Mandatory Standard on Access Pricing) regime. Also, new fibre rollouts are commercially negotiated (price not regulated) and fixed telcos will command more lucrative returns. Using MCMC’s site rental pricing as guidance, a back-of-the-envelope calculation implies that fibre leasing will account for the bulk of the RM7 billion allocation in DNB’s tender and secured cash flow to fibre owners, especially Telekom Malaysia.

Despite this low-rate environment, telcos’ dividend yields, which average around 2.2%, are not attractive enough to spur domestic and foreign buying interests. Telcos’ foreign shareholdings have improved from their 2017/18 low levels with more apparent swings observed in Telekom Malaysia and Time dotCom.

It is business as usual as the Big-3 telcos remain disciplined and cost-focused. If the Celcom and Digi amalgamation materialises, we expect healthier market rivalry with lesser price undercutting for market share gain. Pre-to-postpaid migration continues to be motivated by voice-to-data substitution.

Maintain “neutral” and reiterate our emphasis on fixed over mobile as they are the prime beneficiaries in broadband/5G infrastructure deployment. Our top picks are Telekom Malaysia (“buy”, target price: RM7.93) and Time dotCom (“buy”, target price: RM16.88).

Astro Malaysia Holdings Bhd

Target price: RM1.36 BUY

MAYBANK INVESTMENT BANK (JULY 14): A May 24, 2021, ruling that the sale of TV boxes with pirated content is illegal is a potentially positive turning point for Astro. With this ruling, Astro is approaching e-commerce and social media platforms to cease the sale of such TV boxes. It is hoped that Malaysians who terminated their Astro accounts in favour of TV boxes will eventually re-subscribe to Astro.

Every RM100 million of TV subscription revenue recouped will accrete RM51 million to our earnings estimate and 10 sen to our target price. In the event that Astro recoups all, albeit unlikely, of the RM1.1 billion TV subscription revenue it lost over the last five years, we estimate that the accretion to our core net profit estimates would be RM550 million and the accretion to our DCF-based target price would be around RM1.10.

Our FY22E/FY23E/FY24E core net profit estimates are raised by 10%/4%/4% respectively on lower-than-expected depreciation and amortisation. Our DCF-based target price is raised by only 2% to RM1.36. Maintain “buy”.

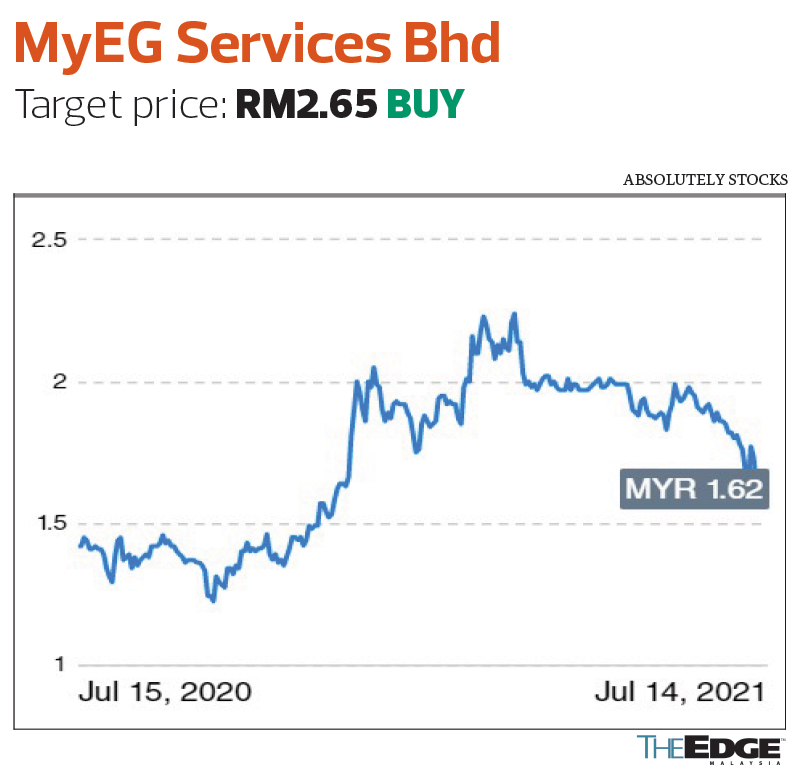

MyEG Services Bhd

Target price: RM2.65 BUY

UOB KAY HIAN RESEARCH (JULY 14): The Ministry of International Trade and Industry (Miti) has made it compulsory for workers employed by manufacturers within Selangor enclaves placed under the Enhanced Movement Control Order (EMCO) to be tested twice a week using Antigen Rapid Test Kits (RTK-Ag).

The push for mass testing will further escalate daily testing volume (88,458 tests/day in July versus 75,848 tests/day in 2Q21), enhancing MYEG’s earnings. MYEG is currently handling around 5,000 Covid-19 tests/day from its foreign worker programmes and MySafeTravel portal. This has contributed to an estimated 15% of MYEG’s 1Q21 net profit.

There is no change to our net profit forecasts although Miti’s required testing could provide a pleasant upside surprise. Maintain “buy” with a target price of RM2.65, pegged at 25 times 2021F PER, and incorporating MYEG’s investment in S5. Our valuations have not factored in any option values of its previous investments in various China and Malaysia start-ups, the chances of clinching the e-visa concession, and the potential of its blockchain and cryptocurrency initiatives.

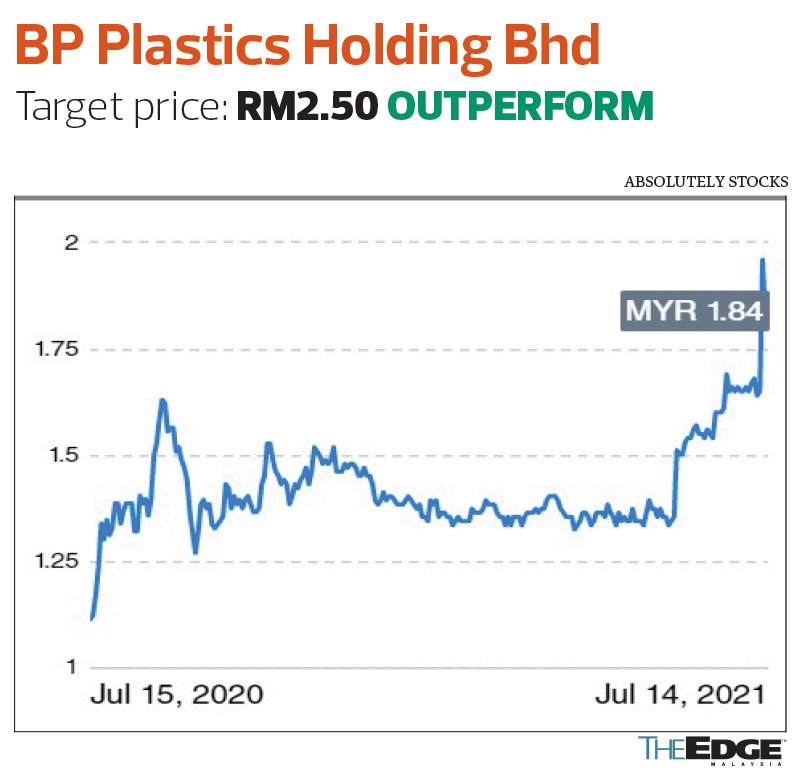

BP Plastics Holding Bhd

Target price: RM2.50 OUTPERFORM

KENANGA INVESTMENT BANK (JULY 12): BP Plastics (BPPLAS) is a key polyethylene film manufacturer in Asia that produces premium stretch film and customised packaging film. We are bullish on BPPLAS for robust demand from export and local markets and like its attractive 5.4% dividend yield.

BPPLAS is in a strong net cash position, when coupled with its ability to consistently generate healthy cash flows, allowing sustained dividend payouts. BPPLAS has consistently paid dividends of 4 sen to 8 sen from 2016 to 2020, with a payout ratio above 50% of net income. We are positive that BPPLAS will continue to pay dividends of at least 8 sen for FY21. We expect DPS of 9 sen for both FY21 and FY22, representing yields of 5.5%, above the industry average of 2.5%.

We estimate FY21E and FY22E net profit of RM36.1 million (+22.4% y-o-y) and RM39.4 million (+9% y-o-y) respectively. Our target price is based on 13 times PER on FY21E EPS of 19.2 sen. We initiate coverage with an “outperform” rating with RM2.50 target price, based on 13 times FY21E PER.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments