Cover Story: Is PRS outperforming EPF?

Eight years since its introduction, Private Retirement Schemes (PRS), a voluntary long-term saving and investment scheme, is beginning to gain traction. Assets under management exceeded the RM5 billion mark last year, with about 500,000 Malaysians putting money in these schemes for their retirement.

“From 2014 [the first full year when eight providers started offering PRS units for sale] to 2020, an average of RM630 million flowed into PRS funds annually,” says Husaini Hussin, CEO of Private Pension Administrator Malaysia (PPA).

Last year was especially good for PRS funds despite Malaysia going through several Movement Control Order periods beginning March 18. The personal tax relief of up to RM3,000 until 2025 provided by the government was a key factor contributing to the increase in inflows.

While there were substantial withdrawals from PRS funds during that period, amounting to 52% of total withdrawals compared with 18% in 2019, more money flowed in rather than out, says Husaini. “The withdrawals were mostly made by PRS members who were 55 years old and above, as they are no longer restricted from accessing their PRS savings.”

Most PRS investors — about 53% of them — are between 30 and 50 years old. They have mainly stayed invested in the scheme with a long-term goal. They are typically those who have achieved a good level of financial strength.

About 80% of PRS members are employed, which means they have savings in the mandatory Employees Provident Fund (EPF) as well. Most of them invested in PRS funds with an aggressive investment approach.

“Almost three-quarters of our assets under management are invested in growth and non-core funds, which are mostly aggressive,” says Husaini.

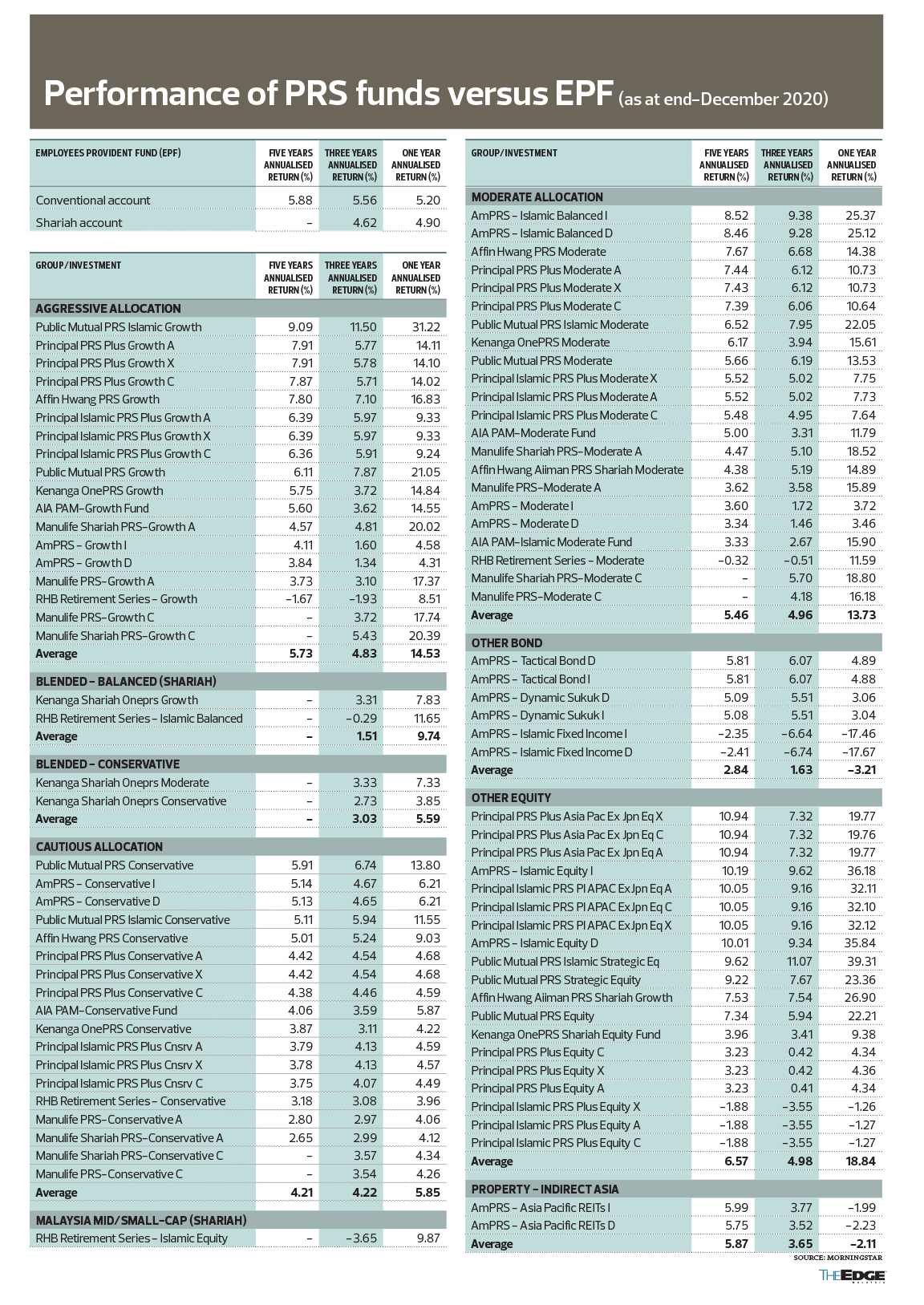

Yet, despite the encouraging growth of the PRS industry, a key question is how well the PRS funds have performed compared with EPF? As a benchmark, the provident fund has produced an annualised return of 5.88% over the past five years.

The answer depends on which fund, given that PRS funds are managed by various fund managers.

According to Morningstar, a Chicago-based investment research firm, 31 of the 79 PRS funds outperformed EPF’s (conventional account) annualised return of 5.88% over the past five years, as at the end of last year.

(Wealth compares the 2020 performance of PRS funds to that of EPF for a more like-to-like comparison. The most recent PRS performance table is available on Page 9.)

However, the results do not include the sales charge imposed on investors by unit trust consultants. The sales charge could be waived or be as high as 3%.

According to Morningstar, the “Other Equity” category, which are funds invested regionally and globally, is the best-performing category. On average, it generated a five-year annualised return of 6.57%. These outperforming funds include the Principal PRS Plus Asia Pacific ex-Japan Equity (10.94%), AmPRS-Islamic Equity I (10.19%) and Principal Islamic PRS PI Asia Pacific ex-Japan Equity series (10.05%).

The “Aggressive Allocation” category, which are funds mainly invested in local equities, is the second best-performing category, providing investors with an average annualised return of 5.73%, slightly below the performance of EPF’s conventional account. The top performers in this category are Public Mutual Islamic Growth (9.09%), Principal PRS Plus Growth series (7.87% and 7.91%) and Affin Hwang PRS Growth (7.8%).

More outperformers are seen under the “Moderate Allocation” category, with funds managed by brands such as AmInvest, Affin Hwang, Principal, Public Mutual and Kenanga.

However, all funds under the “Cautious Allocation” category, except for one, underperformed EPF’s conventional account. All funds under the “Other Bonds” category also generated lower returns than EPF’s conventional account.

Industry players say local funds, especially those under the “Conservative Allocation” category, underperformed EPF due to various reasons.

Chan Ai Mei, chief marketing officer at Affin Hwang Asset Management Bhd, says conservative funds can only invest 20% of investors’ money in equities while the rest is invested in fixed income. For comparison, EPF allocated 36% of its members’ money to equities and 51% to fixed income, according to its 2019 annual report. It also allocated 10% to real estate and infrastructure and 3% to money market funds.

“The mandate of these funds has limited their performance,” she points out.

Another reason is the underperformance of the local stock market, based on the benchmark FBM KLCI, which comprises the largest 30 companies in terms of market value, says Lum Ming Jang, chief investment officer at Public Mutual Bhd.

Until end-April, the FBM KLCI had retracted 14.4% over a three-year period. On the other hand, the US and regional markets, represented by the Dow Jones Industrial Average and MSCI All Country Far East ex-Japan Index, had rallied 46.4% and 28.5% (in ringgit terms) respectively over the same period.

“The performance of the Malaysian equity market has been lacklustre in recent years, largely due to a lack of fresh catalysts, slower corporate earnings growth and outflow of foreign funds,” says Lum.

Munirah Khairuddin, CEO of Principal Asset Management Bhd, says investors have been pulling out their money from Malaysian equities in recent months, which is the main reason local equities did not perform well in the first half of this year. The stronger US dollar, slow rollout of vaccines in the region and political risks in some commodity-exporting markets are among the reasons.

She adds that the global technology sector is another key driver for the outperformance of some global and regional funds. “The US big tech firms, such as Alphabet (Google), Amazon, Apple, Facebook and Microsoft, represented nearly 25% of the S&P 500. Their investors have made outsized gains, and this has benefitted some PRS funds.”

Having said that, the underperformance of the local equity market also makes it the cheapest in the region in terms of valuation, while the average dividend yield of 3% of the FBM KLCI is the second highest among major Asia-Pacific indices after Singapore, says Munirah.

Mixed views from financial planners

Industry players, including various licensed financial planners, opine that PRS is a good initiative. But they have mixed views on whether it is the best investment instrument for retirement saving other than EPF.

Apart from the personal tax relief, the lock-in feature of PRS is good as it forces investors to stay invested over the long term. Pre-retirement withdrawals from PRS funds would incur a tax penalty of 8% on the withdrawal sum, says AHAM’s Chan. “It helps people who lack the discipline to save and invest consistently for retirement over the long term.”

However, it is worth noting that since last year, the government has allowed PRS members to make withdrawals of up to 30% of their PRS savings for healthcare and housing purposes without a tax penalty. This is akin to EPF’s withdrawal mechanism as investors tend to compare their PRS investments with EPF, says Chan.

The lock-in feature also helps investors reap the benefit of compound returns, says Joyce Chuah, CEO of Success Concepts Sdn Bhd. “It particularly benefits the younger generation, who have many more years ahead of them to save and invest for their retirement.”

PRS is also a voluntary scheme that provides investors with the flexibility to decide how much they can invest for retirement, unlike EPF, which is mandatory, says Keah Eewen, licensed financial planner at VKA Wealth Planners.

“You can contribute as little as RM50 or a fixed percentage of your monthly income to the scheme, depending on your retirement goal. It also gives investors the flexibility to invest in aggressive, moderate or conservative funds based on their risk profile,” she adds.

However, the downsides of PRS are apparent. For one, a minimum dividend of 2.5% per annum is guaranteed to EPF members under the EPF Act 1991. PRS does not have the same statutory guarantee, says Keah.

“My advice is for retirees to stay put with EPF. Even in the worst scenario, they will be guaranteed a minimum dividend of 2.5% per annum.”

The lock-in period, seen as a boon for investors, can be a bane too. For instance, what if a PRS fund has not performed well in a given period? According to an industry player, no screening process has been applied to PRS to root out funds that have consistently underperformed so far.

By comparison, EPF’s Members Investment Scheme (EPF-MIS), which allows its members to invest part of their retirement savings in privately managed unit trust funds, applies a screening process known as the Simple Average Rating for Consistent Returns (SACR).

The SACR is computed based on a fund’s aggregate performance over three years by comparing its performance against that of its peers. Unit trust funds that underperform a specific benchmark are delisted from the EPF-MIS scheme.

“I have not heard of any screening process applied to PRS funds as yet,” says an industry player.

What if investors want to switch from an underperforming fund to one that is managed by another fund house? This could involve a manual process such as filling up physical forms and submitting them offline, says Bryan Zeng, general manager at FA Advisory Sdn Bhd.

An online search finds that the switching fee, which is charged when investors pull out their money from a fund to invest it in another fund managed by a different fund house, ranges from 0% to 3%.

“I would prefer that PRS members are provided with more flexibility to withdraw, save and invest their money for retirement, instead of being locked up,” says Zeng.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments