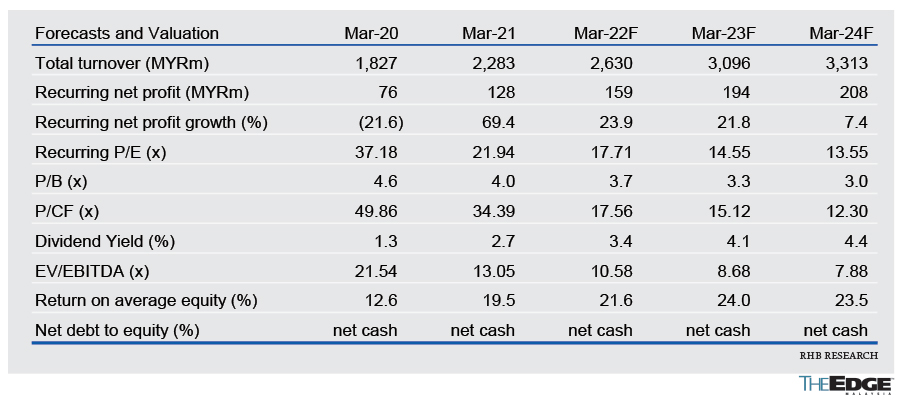

Brokers Digest: Local Equities - SKP Resources Bhd, PPB Group Bhd, Tenaga Nasional Bhd, Focus Point Holdings Bhd

SKP Resources Bhd

Target price: RM2.28 BUY

RHB RESEARCH (SEPT 7): Near-term earnings growth will be boosted by favourable seasonal demand, easing of production capacity limitation, and contribution of new production lines starting 4QFY22F. Beyond that, we expect the order flow to remain robust, thanks to its key customer’s product innovation and ambitious growth target.

We believe it will be timely for SKP to capture the increased order flow arising from the year-end festive demand, and this could propel 3QFY22F to a record high in terms of financial performance. Beyond that, SKP is scheduled to commence two new production lines by 4QFY22F and 1QFY23F. It is also embarking on another major expansion that could start construction by end-2021, and potentially lift total capacity by roughly 40%, once completed. Meanwhile, management reiterated that the hike in raw material, freight and foreign exchange costs will not compress margins, given the cost pass-through mechanism in place.

Following the surge in demand for consumer electronics on the back of stay-at-home practices globally, we are not overly concerned about a potential sharp slowdown due to normalisation. Essentially, we believe sales orders will remain robust underpinned by the key customer’s product innovation as well as the affluent and discerning end consumer profile. In addition, the focus and strategy to roll out customised products to cater for the Asian markets should also drive sustainable growth, considering the relatively lower penetration rate, for example in China as compared with the Western countries. Currently, SKP ships most of its manufactured output to China and has observed a strong growth rate.

We raise FY23F-24F earnings by about 14% to account for the robust job orders and sustainable margin trends per management guidance. Correspondingly, our target price is lifted to RM2.28 based on unchanged 19 times 2022F PER, which is in line with close peer VS Industry Bhd. New product tendering or bidding should be called by its key customer by year end, as usual, and we gather that SKP is also in talks with a potential new customer. However, the outcome of whether the party can be onboarded will only be known, at the earliest, by mid-2022. That said, we have yet to impute any new win into our model and, hence, the aforementioned would pose earnings upside risk.

PPB Group Bhd

Target price: RM20.70 BUY

UOB KAY HIAN RESEARCH (SEPT 7): Management expects food commodity prices to remain volatile in view of the current poor weather and tight supply situation; however, PPB is confident with its own better supply chain management and experienced procurement team to secure raw materials at the right timing with better pricing. Hence, the profit margin compression may come in lower than market expectation despite the huge spike in the commodity prices.

Consumer-related segments are expected to perform satisfactorily as there was some logistics and operational disruption in 1H21 especially in the Klang Valley due to the severe Covid-19 situation. With a higher percentage of the population vaccinated and better economic recovery in 2H21, we expect the sales volume for the consumer-related segments (grains and agribusiness, and consumer products) to be higher as compared with 1HFY21. On top of that, this would also boost its new 500-tonne-per-day wheat flour mill by Vietnam Flour Mills Ltd (VFM-Wilmar Flour mill), which is expected to complete by 3Q21.

The property and environmental engineering and utilities segments are expected to improve once the MCO is lifted with: (a) better footfall in their malls, (b) increased sales of its development properties, and (c) better progress on construction works and projects.

Tenaga Nasional Bhd

Target price: RM12.42 OUTPERFORM

PUBLIC INVESTMENT BANK (SEPT 8 ): Tenaga Nasional (TNB) via its wholly-owned subsidiary TNB Power Generation Sdn Bhd announced that it has received a letter of notification from the Ministry of Energy and Natural Resources to develop a hydroelectric power plant with a capacity of 300MW in Gua Musang, Kelantan.

The hydropower plant will be built in Mukim Ulu Nenggiri, Jajahan Gua Musang, Kelantan, and is one of the two large-scale hydro projects commissioned by Suruhanjaya Tenaga in Peninsular Malaysia. The project cost is estimated at RM5 billion, which we understand will be financed through a combination of debt and equity.

To recap, this project is part of the strategic national hydroelectric project that complements TNB’s aim in supporting the government’s ambition to increase the share of renewable energy in its installed capacity to 31% in 2025 and 40% in 2035 under its power generation plan. While the project is expected to be earnings accretive, the construction is estimated to take five years. As such, the expected scheduled commercial operation date is June 1, 2027, which is beyond our forecast horizon. All told, we make no changes to our earnings estimates at this juncture but affirm our “outperform” call, with the DCF-derived target price unchanged at RM12.42.

Focus Point Holdings Bhd

Target price: RM1.03 BUY

HONG LEONG IB RESEARCH (SEPT 7): We understand that in April, Focus Point sustained strong sales momentum and chalked in record-high sales for both the optical and food and beverage (F&B) segments. However, the subsequent Phase 1 restrictions hampered June sales with lower foot traffic in retail areas, which dragged the group’s optical division. F&B, on the contrary, registered better revenue from the higher corporate sales and stable sales from the new Komugi outlet in SS2.

With the various restrictions and closure of retail outlets, we gather that Focus Point is able to receive rental rebates from landlords. Furthermore, the group also managed to save some staff costs with the RM1 million wage subsidy from Perkeso and 60% workers’ capacity restrictions, which shortened the workdays for its employees to four days a week. Management is optimistic with the pathway returning to normalcy, thanks to the ramp up of vaccination rates that would provide a further boost for its contact lens business as offices reopen.

We remain confident on Focus Point’s scalable business model as we reckon that both its optical and F&B segments are able to ramp up fully once operating conditions normalise. Furthermore, we expect a high probability of securing new F&B corporate clients given the popularity of its current product offerings.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments