Bumiputera equities control measure has unintended consequences

THE government’s move to introduce a control mechanism on the disposal of bumiputera equities to non-bumiputera investors under the 12th Malaysia Plan is seen as disruptive to the market and leading to unintended consequences.

This is because the measure will see the creation of a two-tier price discovery in the market, with bumiputera equities being priced differently than non-bumiputera equities. There is also concern that the measure will dampen investors’ confidence in the Malaysian market.

“This sort of policy is bad on many fronts. It is the type of policy that destroys investors’ confidence in Malaysia, not just FDI (foreign direct investment) but also foreign inflows into the equity and debt markets. It will also dampen domestic investments,” says economist Dr Nungsari Radhi.

Responding to questions from The Edge on the proposed policy, Nungsari says it creates a two-tier pricing on the same asset, which is distortionary and will have deleterious effects. He adds that the policy will make the bumiputera investor a “toxic investor” as his presence in any company will distort its share price.

It will also affect the way bumiputera funds — like those under the management of Permodalan Nasional Bhd (PNB) — are treated, says Nungsari. PNB’s funds are invested in various companies, including industry leaders, listed on Bursa Malaysia.

The companies include Malayan Banking Bhd, Sime Darby Bhd, Sime Darby Plantation Bhd, Sime Darby Property Bhd, S P Setia Bhd, UMW Holdings Bhd, Velesto Energy Bhd, Duopharma Biotech Bhd, MNRB Holdings Bhd and Sapura Energy Bhd.

“Worse of all, this policy will not benefit the large majority of bumiputeras. It will benefit those with wealth to acquire these assets. And worse, it punishes good, viable businesses and investors,” he says.

In presenting the 12th Malaysia Plan last Monday, Prime Minister Datuk Seri Ismail Sabri Yaakob said that to ensure sustainable bumiputera equity ownership, the government will introduce a bumiputera equity framework whereby bumiputera equities are only offered and sold to other bumiputeras.

The selling of bumiputera equities will be monitored by the relevant ministries and agencies, he said. A Bumiputera Prosperity Department will be formed with a clear mandate and function to spearhead and streamline this initiative, says Sabri.

It is not clear what the framework entails or how the mechanism works. The prime minister said the government came up with this initiative because bumiputeras’ equity ownership is still less than the 30% aspired to in the New Economic Policy.

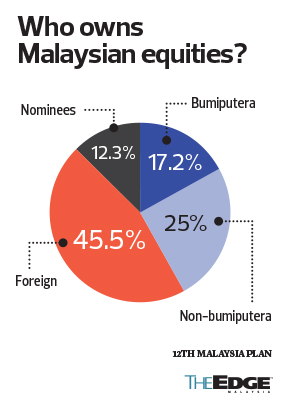

He added that as at end-2019, bumiputera equities constituted only 17.2% of the market value of corporates in Malaysia. Meanwhile, non-bumiputera equities constituted 25%, and foreign ownership was 45.5%.

The rest were held by nominees. It is not clear who the ultimate owners of these shares are, as they are held through investment banks and other financial institutions.

Other questions raised include how these values were derived and how a bumiputera investor is defined.

The measure, if implemented, will also jeopardise the development of bumiputera companies, as they will be restricted in getting access to technology and foreign markets, says Dr Afzanizam Abdul Rashid, chief economist at Bank Islam Malaysia Bhd.

“While the element of control is good to ensure order, we need to appreciate that the business landscape is changing rapidly, and it is extremely competitive.

“At times, businesses, be it bumi or non-bumi, would need to make a commercial decision in order to stay competitive and that may include partnering with other business ventures that may not be bumi.

“Such decisions can be important as it would allow technological transfer to occur in the most effective way while at the same time, it may open up access to foreign markets. So perhaps there should be more clarity on this,” he says when contacted by The Edge.

Meanwhile, Dr Zokhri Idris, director of external relations at the Institute for Democracy and Economic Affairs (IDEAS), says the control mechanism will introduce more bureaucratic intervention in the economy with the creation of the Bumiputera Prosperity Department.

It might create a clash between FDI’s interests with that of the bumiputera agenda, he says. While the mechanism might lead to a short-term gain for bumiputeras, it is not sustainable as in the long run, foreign investment would register this as a risk of doing business in Malaysia, he says.

“It is still too early to project, but we cannot deny the possibility that the foreign firms will shy away due to this mechanism — especially if bumiputera managements have issues on competency and productivity. In the end, bumiputera equities will be unattractive,” Zokhri tells The Edge.

The control mechanism might also impact bumiputeras’ productivity and competitiveness, he adds, as bumiputera entrepreneurs will be competing at a different level than the rest of the market, as they receive more protection.

This could also lead to structural isolationism from the market’s operation, which is counter-productive in the long run in the effort to build up bumiputeras’ industrial and entrepreneurial capacity and capabilities, he says.

There are also concerns that the control mechanism will cause Malaysia to become even less attractive to foreign investors. This is because further protectionism on bumiputera companies and investors might make them more uncompetitive.

Furthermore, there is also concern that the measure might mean that bumiputera agencies such as PNB, Ekuiti Nasional Bhd and, to a certain extent, Majlis Amanah Rakyat, would have to pick up the slack when it comes to buying bumiputera equities.

If the companies or assets are performing and have huge potential, they would be good investments for the bumiputera agencies.

Zokhri also cautions that if the bumiputera-specific government-linked investment companies (GLICs) are roped in to acquire depressed assets to comply with the control measures, it will lead to GLICs being used to rescue certain companies.

“We will see how bumiputera-specific trust funds and private equity firms will race to acquire more bumiputera equities. The immediate problem would be if the share transfer is under the market value, leading to these firms acquiring less-productive companies.

“In the long run, we should be cautioned that such firms are GLICs, where their boards are dominated by the government. We have seen in the past how Lembaga Tabung Angkatan Tentera, Lembaga Tabung Haji and KWAP have been involved in mega scandals involving government’s investments locally and abroad,” he says.

While it is not clear whether the government will rope in bumiputera-centric GLICs to pick up bumiputera equities if there are no other investors from the community, Nungsari says if they do, the GLICs themselves will become toxic investors. “And by extension, Malaysia will become a toxic market. Who wants to come to this market?” he asks.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| BURSA | 7.460 |

| DPHARMA | 1.180 |

| MAYBANK | 9.780 |

| MNRB | 1.710 |

| SAPNRG | 0.045 |

| SIME | 2.800 |

| SIMEPLT | 4.440 |

| SIMEPROP | 0.915 |

| SPSETIA | 1.410 |

| UMW | 4.970 |

| VELESTO | 0.265 |

Comments