Consolidation in stockbroking industry to persist

THE recent proposal by Alliance Bank Malaysia Bhd to dispose of its stockbroking unit to Phillip Futures Sdn Bhd may suggest further consolidation is in store for the stockbroking industry, in view of dwindling trading volumes this year.

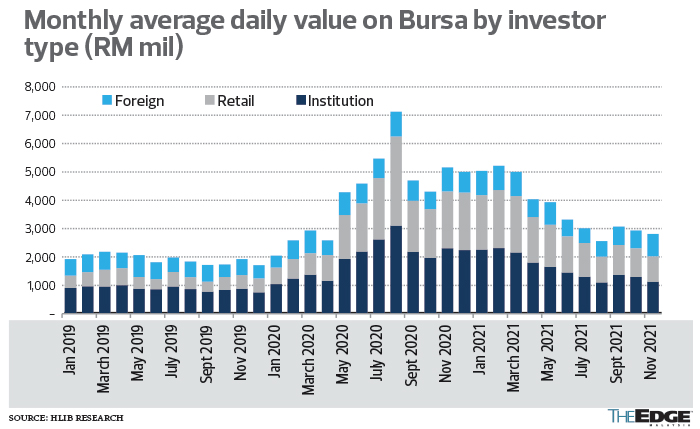

Last year was an exceptional one for stockbroking firms. Trading interest, particularly among younger investors, picked up swiftly after the global equity rout in March.

Plans for mergers and acquisitions (M&A) seem to have reemerged in the stockbroking industry, likely caused by a foreseeable dampening effect from the stamp duty hike next year.

The stockbroking industry is fragmented with many small and big players, leading to heightened competition. According to Bursa Malaysia, there are currently 30 stockbroking firms in the country.

Not helping is the low-fee environment. For instance, online retail broker Rakuten Trade Sdn Bhd, a joint venture (JV) between Kenanga Investment Bank Bhd and Rakuten Securities Inc, offers the lowest brokerage fees — as low as RM7 — in Malaysia.

Smaller brokers, in particular, have been dragged down by margin compression in the industry. This, in turn, has weakened their ability to compete. So, either JVs or M&A could be the way forward for the industry.

In fact, there have been several corporate exercises involving stockbroking firms in the past few years. CGS-CIMB Securities Sdn Bhd, a JV between CIMB Group Holdings Bhd and China Galaxy International Financial Holdings Ltd, commenced operations in July 2019.

But not all have come to fruition. The proposed merger between JF Apex Securities Bhd and Mercury Securities Sdn Bhd fell through after dragging on for more than two years.

Two months ago, Insas Bhd unveiled plans to unlock the value of M&A Securities Sdn Bhd via a reverse takeover exercise. M&A Securities is set to assume the listing status of furniture maker SYF Resources Bhd.

Datuk Bill Tan, managing director of corporate finance at M&A Securities, foresees that more stockbroking firms will be pressured to undertake M&A exercises in view of the lower trading volumes that would result from the proposed stamp duty hike.

“There will be more competition in the market with lower profits by all the stockbroking houses. Our business will definitely be affected, so there could be more M&A in the industry,” he says.

Tan thinks the most important thing is to increase trading volumes in the stock market, and this cannot be achieved if there is no cap on the stamp duty. “The cost is just too high. Other markets are trying to reduce costs, yet Malaysia is increasing the cost,” he points out.

Compared with the peak of 27.8 billion shares in August 2020, last Friday’s trading volume slumped to less than three billion shares.

An industry observer says Alliance Bank’s proposed disposal suggests that the banking group does not see value in the stockbroking business anymore. “There is always a case to go for M&A because the volume has come off already.

“We have just too many players in the market for everyone to make a decent return. I think it makes good economic sense for M&A to be looked at, but it is not ruled or prescribed by the authorities. It is driven by market forces.”

With investors’ enthusiasm dwindling as cost challenges increase, he believes there is renewed M&A interest among stockbroking firms. “There will be discussions in the industry. A couple of firms have been up for sale for so long.”

Despite the competition from pure online brokers, traditional stockbroking firms have their own strengths too, he points out. Nonetheless, he observes that the lower trading volumes have been reflected in the financial results of some stockbroking houses.

“If you look at Kenanga Investment Bank, you can see that its profit has dropped, reflecting the decline in enthusiasm. For Rakuten, it just made money for the first time last year after losing money for four to five years. With reduced turnover, I am eager to see Rakuten’s upcoming results,” he adds.

For 3Q2021 ended Sept 30, Kenanga’s net profit sank 56.48% year on year to RM21.44 million from RM49.27 million, owing to lower net brokerage and trading and investment income, as a result of the weaker trading volumes on the local bourse. Quarter on quarter, it was down 29.87% from RM30.57 million.

The industry observer points out that automation will become an important factor in the effort to control costs. “It may cost you more but, eventually, you will have a smoother and more efficient operation.

“Some players may want to merge their back offices with joint settlement and clearing. It may not be a full-fledged merger, but it could be a sharing of common functions, so you don’t lose your proprietary information.”

Nonetheless, he cautions that Malaysia may lose some foreign funds if the quantum of the proposed stamp duty hike is not reduced. “We are one of the highest right now in terms of transaction costs compared with Singapore, Indonesia and Thailand. If I were a foreigner, I wouldn’t necessarily look at Malaysia only,” he points out.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments