Relief measures help GETS Global, Annum, Bahvest stave off PN17 status

IN 2020 and 2021, the Securities Commission Malaysia (SC) and Bursa Malaysia introduced temporary relief measures to help Bursa-listed companies with cash flow difficulties during the Covid-19 pandemic. These measures included giving listed issuers more time to rectify their unsatisfactory financial conditions.

With the relief period having ended on Dec 31, 2021, more companies in financial distress will come to the fore.

The first month of 2022 has already seen four listed issuers entering the list of companies under Practice Note 17 (PN17) category. They are AirAsia Group Bhd (since renamed Capital A Bhd), Serba Dinamik Holdings Bhd, Top Builders Capital Bhd (formerly known as Ikhmas Jaya Bhd) and Jerasia Capital Bhd.

At the end of January, companies under PN17 and Guidance Note 3 (GN3) totalled 27, which accounted for 2.98% of the 907 companies listed on the Main and ACE Markets, according to Bursa.

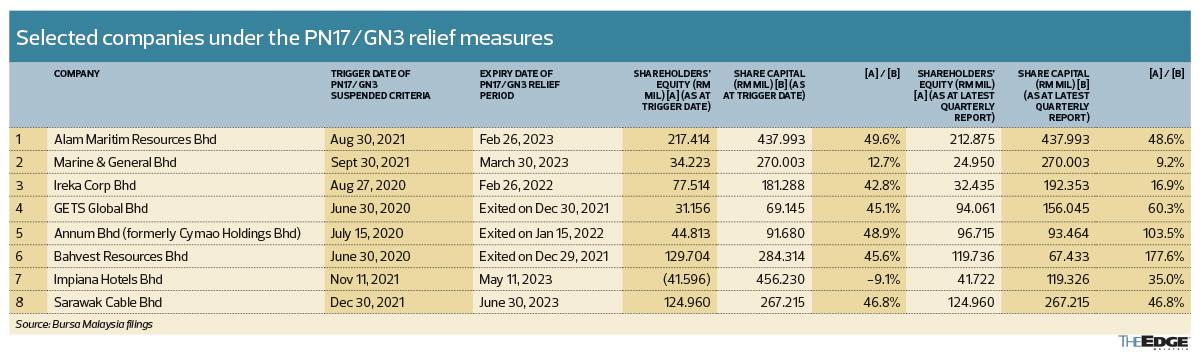

The good news is, a check on Bursa by The Edge shows that three companies — GETS Global Bhd, Annum Bhd and Bahvest Resources Bhd — have benefited from the deferment of being classified as a PN17/GN3 listed issuer during this period.

Take, for instance, GETS Global. The bus operator and glove manufacturer had triggered the PN17 criteria in June 2020 after its shareholders’ equity of RM31.16 million fell below 50% of its share capital of RM69.15 million as at March 31, 2020. Its external auditors, Messrs PKF, had also flagged a material uncertainty related to its ability to continue as a going concern when going through its accounts for the financial period ended June 30, 2019.

Thanks to the 18-month relief period, the group’s shareholders’ equity has risen to RM94.06 million — representing 60% of its share capital of RM156.05 million as at end-September 2021. On Dec 31, 2021, GETS Global announced that it no longer triggered any of the PN17 criteria.

Likewise, Annum (formerly known as Cymao Holdings Bhd) had fallen into the the PN17 category in July 2020 after its shareholders’ equity fell to only 49% of its share capital as at March 31, 2020. Its external auditor PKF had also cast doubt on Annum’s ability to remain as a going concern when auditing its accounts for the financial year ended Dec 31, 2019.

However, as at end-September 2021, the group had increased its shareholders’ equity to RM96.72 million — representing 104% of its share capital of RM93.46 million. Upon the expiry of the 18-month PN17 relief period on Jan 15, Annum also said it no longer triggered any of the suspended criteria.

As for ACE Market-listed Bahvest, it had triggered the GN3 criteria in June 2020 after its shareholders’ equity fell below 50% of its share capital at the end of March 2020. However, as at end-September 2021, the group had managed to increase its shareholders’ equity to RM119.74 million — representing 178% of its share capital of RM67.43 million.

In April 2020, the SC and Bursa had introduced the waiver as part of a package of measures aimed at alleviating the impact of Covid-19 on businesses. With the waiver, companies that triggered any of the suspended criteria between April 17, 2020, and June 30, 2021, would not be classified as a PN17 and GN3 company for 12 months.

The waiver was extended, with the latest extension granting companies that trigger the PN17 or GN3 suspended criteria between July 1, 2021, and Dec 31, 2021, an 18-month relief period.

Capital A hit hard by relegation to PN17 category

Of the industries affected by the pandemic, none has been hit as hard as the airline industry. Capital A has been loss-making since 2019 and is expected to remain in the red for the financial year ended Dec 31, 2021 (FY2021).

The low-cost carrier had triggered the PN17 suspended criteria in July 2020 when its external auditor Messrs Ernst & Young PLT said in its FY2019 audit report that there was material uncertainty over its ability to continue as a going concern. Also, its shareholders’ equity was only 37% of its share capital as at March 31, 2020. However, Capital A was given the 18-month reprieve until Jan 7 this year from being classified as a PN17 company as part of the Covid-19 relief measures.

Capital A’s stock declined pretty steeply after it announced on Jan 13 that its appeal for relief extension was rejected by Bursa and it is now a PN17 listed issuer effective Jan 7. Since the announcement, the share price of Capital A has fallen 27% to hit an all-time low of 54.5 sen on Jan 31. It closed at 66.5 sen last Thursday, bringing its market capitalisation to RM2.77 billion, amid news that the government may reopen Malaysia’s international borders from as early as March 1.

Minority Shareholders Watch Group (MSWG) CEO Devanesan Evanson says even though Capital A was technically a PN17 company more than a year ago, the clock did not start ticking for the airline until it was classified as a PN17 listed issuer — it has 12 months to submit a regularisation plan to Bursa for approval, or face delisting.

“The 18-month relief period was like a holiday where there was no urgency to regularise your financial condition. That’s why Capital A’s share price had been able to maintain [a constant upward trend],” he tells The Edge.

“But now that Bursa has said no to an extension, it is now a PN17 listed issuer, and it has one year to regularise its financial condition because if it doesn’t, it will face trading suspension and a delisting. That’s why the share price dropped — the one-year clock has started ticking.”

Devanesan notes that panicked investors had triggered the sell-off of Capital A shares on Jan 14, wiping RM520 million off its market capitalisation overnight. “The market panicked. Investors may wonder what happens if it doesn’t regularise [its financial condition] within one year.”

Why do investors continue to hold on to stocks of companies that have triggered the PN17 criteria? Devanesan says one main reason is that some investors may have thought that Bursa would extend the PN17/GN3 waiver.

“Recall that Bursa had recently announced another 12-month extension of the temporary relief measures to provide flexibility for fundraising by way of private placement and rights issue, which would have expired on Dec 31, 2021. Shareholders probably thought Bursa would extend the PN17/GN3 waiver too.”

On its part, Capital A has been rushing to raise capital to shore up its balance sheet as the pandemic continues. Its group CEO Tan Sri Tony Fernandes has said that the airline has raised over RM2.5 billion to date.

“We have plans to raise up to RM400 million in additional capital this year. This will ensure sufficient liquidity to ride out the effects of the pandemic in 2022,” he said.

However, this reassurance failed to prevent the recent selldown in Capital A shares. “On a balance of probabilities, the investors did not want to take the risk because the one-year time frame [to regularise its financial condition] is fast approaching, and prefer to move their investments elsewhere,” MSWG’s Devanesan says.

In a Jan 17 report, CGS-CIMB Research aviation analyst Raymond Yap estimated that Capital A will need a RM7.385 billion boost to its shareholders’ funds on a pro forma basis as at Sept 31, 2021, in order to be removed from the PN17 classification, which he thinks will be extremely challenging to achieve.

Still, Devanesan does not expect shares of other companies facing PN17/GN3 status to witness heavy selling pressure like that of Capital A “given that the market has already factored this into their share price”.

Etiqa Insurance and Takaful chief strategy officer Chris Eng Poh Yoon concurs. “For stocks that don’t have a large institutional following, I don’t think their share price will react so much.”

He says in the case of Capital A, the PN17 classification has negative implications for its share price because some institutional investors have mandates that prevent them from investing in such companies.

“For example, some funds are not permitted to invest in ACE Market-listed companies even though the fund managers may think highly of the stock. And this investment mandate differs from one fund to another.

“It is like a company dropping out from the shariah-compliant list. If that happens to a stock in a takaful fund, they would have to sell off the shares even though they think six months later the stock will be back on the shariah-compliant securities list. They still have to sell off the shares first because the investment mandate says so,” Eng says.

“Also, some retail investors probably thought Capital A would be able to get the appeal accepted while some might be unaware that there was a risk of it being classified under PN17,” he adds.

An investment banker, who asked not to be named, believes the recent selldown in Capital A shares is just retail investors’ knee-jerk reaction. He says aviation stocks like AirAsia will remain volatile, influenced by news flow on travel.

While some quarters believe 2022 will be a recovery year for the travel and tourism sector, the International Air Transport Association has said that a full recovery to 2019 levels will only happen in 2024.

Sieving through companies in financial distress

“There are basically two types of PN17 companies: Those on the way to becoming insolvent, and those, like Capital A, that primarily triggered the PN17 criteria because of certain parameters that Bursa has set, but still have a viable future. Capital A just needs time to regularise its financial condition. It is a function of how fast it can rebuild its business,” the investment banker says.

A check on the local bourse reveals that Malaysia Pacific Corp Bhd has been the longest-standing PN17 listed issuer since November 2014, when its external auditors had expressed a disclaimer opinion in its audited financial statements for the financial year ended June 30, 2014. After several extensions, the property firm has yet to submit its proposed regularisation plan to Bursa. Last Friday, it was granted more time — until June 30 — to do so.

“For Capital A, it still has a solid underlying business. Financially, it is still not out of the woods. It wants to be the No 1 ride-hailing and food delivery company in Asia. To me, I give it a fair shot at being able to rebuild its business,” the investment banker adds.

According to CGS-CIMB Research’s Yap, Capital A has until the end of 2022 to submit a regularisation plan to Bursa for approval, after which it will have six months to execute the plan. It will then need to apply to Bursa to lift the airline from its PN17 status. This comes with the condition that the airline registers net profit for two consecutive quarters immediately after the completion of the implementation of the regularisation plan.

Is there hope for distressed companies without relief measures?

Meanwhile, PN17 companies whose 12-month deadline to submit their regularisation plan is coming up soon include in-flight catering service firm Brahim’s Holdings Bhd and public bus operator Konsortium Transnasional Bhd (KTB).

Brahim’s has until Feb 27 to submit its regularisation plan, or face delisting. In its latest filing with the exchange on Feb 3, it warned that it is unlikely to be able to finalise and submit its regularisation plan to Bursa for approval within this time frame and hence, it intends to seek an extension of time from the regulator.

Likewise, all eyes are on KTB to see if it can submit its plan to address its financial condition by April.

It also remains to be seen whether Alam Maritim Resources Bhd, Marine & General Bhd, Ireka Corp Bhd, Impiana Hotels Bhd and Sarawak Cable Bhd can avoid becoming PN17 companies. All except for Ireka have until 2023 to rectify their financial condition.

Ireka’s PN17 relief period ends on Feb 26, but it announced on Feb 8 that it had sought an extension to the waiver from Bursa. The group triggered the financially distressed company status in August 2020 after its auditor flagged a material uncertainty related to its ability to continue as a going concern regarding its accounts for the financial period ended March 31, 2020. Its shareholders’ equity of RM77.51 million fell to less than 50% of its share capital of RM181.29 million as at March 31, 2020, owing to the loss recorded by its associate Aseana Properties Ltd, whose business had been significantly affected by the pandemic.

Nevertheless, Ireka’s latest results for the quarter ended Sept 30, 2021, show that its shareholders’ equity has fallen to RM32.44 million — representing 17% of its share capital of RM192.35 million.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| 6548 | 0.000 |

| ALAM | 0.025 |

| ANNUM | 0.095 |

| BAHVEST | 0.540 |

| BURSA | 7.450 |

| CAPITALA | 0.685 |

| CIMB | 6.650 |

| EPICON | 0.420 |

| IREKA | 0.270 |

| JERASIA | 0.005 |

| M&G | 0.285 |

| MAGMA | 0.190 |

| ONEGLOVE | 0.245 |

| SCABLE | 0.160 |

| SERBADK | 0.020 |

| TOPBLDS | 0.005 |

Comments