Wood manufacturing firms to tap rising housing and furniture demand

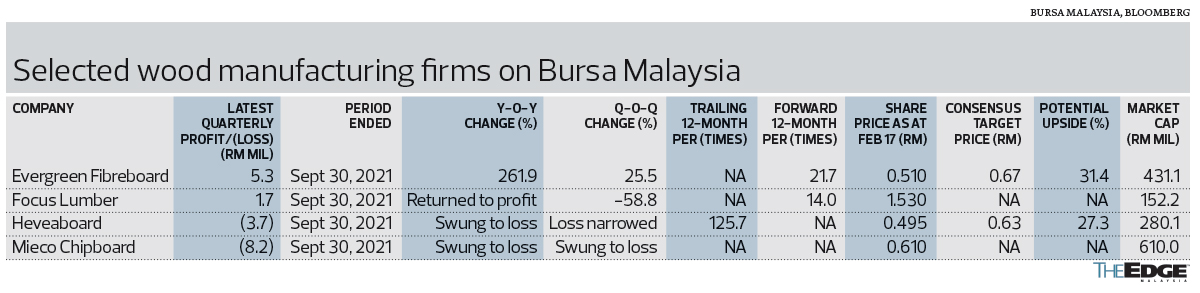

THE wood manufacturing industry has long been off the radar screens of investors, until recently. Shares in panel board manufacturers have gained since early this year, with Focus Lumber Bhd rising 23.4%, followed by Heveaboard Bhd (+15.1%), Mieco Chipboard Bhd (+10.9%) and Evergreen Fibreboard Bhd (+9.7%).

As the global economy stays on the path to recovery, analysts see the revival of housing activity and demand for furniture as key catalysts for the sector.

HLIB Research analyst Tan Kai Shuen says the industry’s valuations were undemanding last year, owing to factors such as prolonged lockdowns, which had a negative impact on production; high raw material prices; foreign labour shortage due to border closures; as well as environmental, social and corporate governance (ESG) concerns on the forced labour issue.

“On raw material costs, prices of rubberwood were higher towards the end of last year because of the seasonally wet weather and floods, while the cost of glue rose because of high urea prices; but the glue price has stabilised and should start easing this year.

“Meanwhile, border closures resulted in the inability to take in foreign workers, but manufacturers have submitted applications to bring in foreign labour. When this materialises, it will be a major earnings catalyst for these firms as they will be able to increase their capacity. Lastly, the concern over the next manufacturing sector targeted for forced labour allegations also caused depressed share prices last year,” Tan tells The Edge.

Nonetheless, he observes that the outlook has turned more positive for the industry in view of the upcoming foreign labour intake, orders and selling prices that remain robust as Malaysia continues to be a beneficiary of the trade diversion from the US-China trade war, as well as the easing of raw material prices.

“I think investors are forward-looking; the foreign labour shortage that is expected to be resolved soon will be a big boost to their capacity,” he says.

Wood manufacturers are likely to see a rebound in earnings for 4Q2021, following the impact from the Full Movement Control Order in 3Q2021 as well as a backlog in orders, according to Tan.

The panel board segment comprises particle board, medium-density fibreboard (MDF) and plywood.

Heveaboard, which produces particle board and ready-to-assemble furniture, is forecast to see a turnaround in the financial year ending Dec 31, 2022 (FY2022), as sales to Japan have been improving since the second half of last year.

“In FY2021, it could still be making losses, but the situation will improve in FY2022 … Heveaboard’s share price has been a laggard so far compared to its peers,” Tan says.

For 9MFY2021, Heveaboard posted a net loss of RM8.51 million against a net profit of RM5.62 million in the same period a year ago.

Evergreen manufactures MDF and particle boards, which contribute 80% to sales; the remaining 20% is from the furniture segment. It has three production sites in Malaysia, Thailand and Indonesia; and the Middle East is a major export market for the group.

“The panel board segment is experiencing a price recovery and this is reflected in the recent strength in its share price. Quarter on quarter, we expect earnings will rebound strongly in 4Q2021,” says Tan.

Evergreen registered a net profit of RM19.14 million in 9MFY2021 versus a net loss of RM21.77 million in 9MFY2020.

Meanwhile, Focus Lumber, which is involved in the manufacture of plywood, veneer and laminated veneer lumber, is expected to ride sustainable high plywood prices throughout 2022.

“The combination of limited existing home inventory in the US and solid buyer demand has driven the need for new housing construction to pick up, which has in turn increased the demand for plywood, a component widely used in internal housing structures,” says HLIB Research analyst Sam Jun Kit in a recent research note.

Sam highlights that Focus Lumber will benefit from the positive spillover effect of the “lumber war” between the US and Canada, as it exports mainly to the US market.

“The US recently imposed a much higher average import duty on softwood lumber from Canada, at 17.9% from 8.99% previously. Canada is the world’s largest softwood lumber exporter and the main exporter of plywood to the US. The steep increase in [the import] duty, coupled with the US’ ongoing trade spat with China, is likely to [cause US importers to source their timber products from other countries] such as Malaysia, Vietnam and Indonesia, amid booming housing demand in the US.”

Focus Lumber returned to the black with a net profit of RM2.94 million in 9MFY2021, compared with a net loss of RM5.63 million in 9MFY2020, underpinned by higher sales volume and average selling prices.

Overall, HLIB’s Tan believes there is still upside for wood manufactures, on the back of strong housing demand in the US, which will benefit mainly Focus Lumber. Evergreen is also poised to take advantage of a pickup in consumer spending on furniture in the Middle East, as well as strong demand from furniture makers in Indonesia and Malaysia.

ESG concerns about forced labour, which was a major issue in 2021, may start to ease, especially with many wood manufacturing companies actively identifying and improving their labour practices.

“Investors who wish to mitigate risk on this end can invest in companies that have a strong governance and management track record. Other key risks are the persistent labour shortage, as a result of the emergence of new [Covid-19] variants, which may prolong the process of foreign labour intake, as well as inflationary pressure on raw material costs that weigh on margins,” Tan says.

Lee Chung Cheng, head of research at JF Apex Securities, expects the industry outlook to remain uncertain, however, with labour and raw material costs being the major concerns.

Lee foresees high raw material prices tapering off in the second half this year, but thinks they may remain elevated and are unlikely to return to pre-pandemic levels.

He also cautions that it is not easy for players to pass on the costs to customers, owing to stiff market competition, especially from Thailand.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments