Creditors in difficult position as cash-strapped Sapura Energy bites bullet again

SAPURA Energy Bhd has to bite the bullet again. This time around, it is not obtaining fresh funds; it is undertaking a massive debt restructuring involving banks, vendors and contractors as the oil and gas (O&G) giant is still cash-strapped.

Sapura Energy announced last Thursday that the court had granted an order under Section 366 of the Companies Act that will enable it and its subsidiaries to summon meetings with its creditors to consider and approve a proposed scheme of arrangement and compromise as part of its debt restructuring plan.

The company has also obtained a restraining order under Section 368 — effective for three months from March 10 — to restrain and suspend legal proceedings against it, while enabling the group and its subsidiaries to engage with its creditors without being disrupted by the threat of litigation.

In other words, the group is buying time to settle its debt obligations. Some see the debt restructuring plan as a final attempt to get it out of the woods.

Some analysts comment that the restructuring should have been done much earlier as the writing had been on the wall for some time now, with winding-up petitions by vendors and suppliers and the liquidity stress since December 2021 being the last straw for the company.

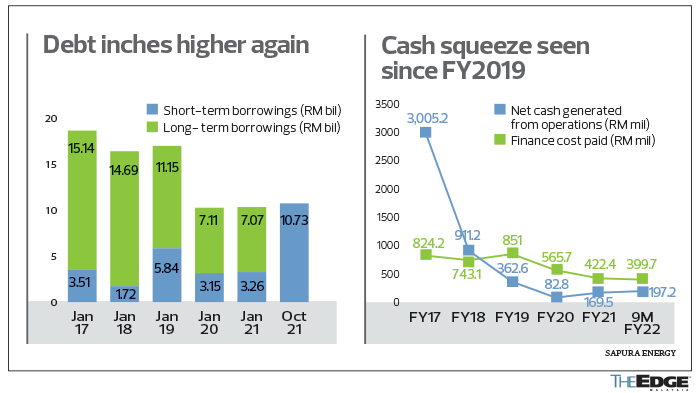

Despite a RM4 billion cash call in 2019 and a subsequent RM10.3 billion debt refinancing in 2021, Sapura Energy continued to bleed red ink in four of the last five years. Worse, its sales are not generating sufficient cash to sustain it as a going concern.

Its loss-making contracts were an additional burden, compounding its RM10.7 billion debt and trade payables of RM3.35 billion. Moreover, its pandemic-related expenses proved challenging to claim.

Sapura Energy’s 44-page filing with Bursa Malaysia last Thursday detailed a restructuring of debt owed to creditors that involved the listed entity and 22 subsidiaries, including its fabrication, engineering, vessel, and drilling divisions.

The proposal entails a haircut where out of every RM1 in liabilities owed, roughly 25 sen will be refinanced. Another 20 sen will be converted to perpetual non-tradable in-kind notes of 5% coupon per annum. The perpetual paper is convertible into ordinary shares of Sapura Energy in its fourth year.

The remaining 55 sen will be converted to perpetual non-tradable zero-coupon notes issued by Sapura Energy, which will be converted into shares in its subsidiaries, namely Sapura Drilling Sdn Bhd, Sapura Technology Solutions Sdn Bhd and Sapura Geosciences Sdn Bhd, in the fourth year.

An industry watcher says it is likely that Sapura Energy would have already gauged the appetite of its biggest lenders before coming up with the numbers. Recall that the restructuring is the outcome of its Board Restructuring Task Force, which was first established in December 2021.

But vendors and suppliers, some of whom have not been paid since 2020, appear to have been caught off-guard.

Vendors ‘disappointed’ with turn of event

A senior official of one vendor company pursuing legal action against Sapura Energy says the news “is not a healthy sign for the industry and not welcome news for many of the affected subcontractors and vendors”.

“As unsecured creditors, we probably will have to accept hefty haircuts, which will destroy many subcontractors and vendors that have over the years built up their capabilities.

“Our wish is for Sapura Energy’s main shareholder to really understand that the group is really a giant project contracting company and to put in place senior management that can not only ride out the crisis but have the appropriate experience to run a project contracting company,” the vendor company’s official said.

Industry association the Malaysian Oil and Gas Services Council (MOGSC), when contacted, said: “As a representative of the many subcontractors and vendors who have supported Sapura Energy through the years, MOGSC is truly disappointed with this turn of event.

“Many of these companies, which are mostly SMEs (small and medium enterprises), will now face serious financial difficulties, some amounting to litigation [involving] their respective principals and suppliers. This is despite most jobs being completed and delivered to the end clients such as Petronas, Mubadala and Shell.

“Unfair treatment of the supply chain that was diligently built over many years will surely have serious and damaging consequences for the country. These disastrous consequences should be at the forefront of the mind of the stakeholders, including Petronas, the national oil company, and the government.

“Under these circumstances, MOGSC would be expecting intervention by the relevant stakeholders, which MOGSC would be happy to facilitate.”

In the past, local-listed oil and gas service equipment (OGSE) companies — such as Barakah Offshore Petroleum Bhd and TH Heavy Engineering Bhd, which overgeared at the height of the oil boom — had also taken similar actions.

Despite the tedious restructuring process, both had struggled to rebound with a clean slate, with the latter close to being delisted after failing to submit any regularisation plan.

If negotiations fall through, the next option is for Sapura Energy to be liquidated, which will cost even more for its creditors and could adversely affect the industry ecosystem. The company has some 700 vendors that are hopeful that it would be able to meet its payment obligations.

Clawing for funding in the interim

As the restructuring progresses, Sapura Energy also intends to secure interim funding in order to continue operating as a going concern.

Its 40%-shareholder Permodalan Nasional Bhd injected RM2.67 billion into Sapura Energy in 2018 by taking up the unsubscribed portion, on top of its entitlement.

There will be another round of debate on whether PNB should step in once again to help meet the ailing company’s liquidity needs.

After PNB, Sapura Energy’s second largest shareholder is its former president Tan Sri Shahril Shamsuddin, who controls 13.91% of the company.

Part of the debt restructuring exercise may include the monetisation of its prized assets, which is timely now considering the oil price is at a seven-year high.

Sapura Energy’s assets include its remaining 50% stake in exploration and production arm SapuraOMV. The company had sold off 50% of SapuraOMV to Austria’s OMV Aktiengesellschaft for US$890 million (around RM3.73 billion) in 2018, when oil averaged US$71 per barrel.

With oil price now above US$100 per barrel, and with Sapura Energy’s 500 million cu ft per day Jerun gas field offshore Sarawak slated to come onstream in 2024, the sale of the 50% stake in SapuraOMV could fetch a similar price tag or higher.

The company also has other sizeable assets, such as its fabrication yard in Lumut, six semi-tender drilling rigs and six tender assist rigs, as well as crane vessel Sapura 1200 and pipelaying vessel Sapura 3500.

Overall, the restructuring will definitely see Sapura Energy downsizing and becoming a contractor again instead of a full-fledged asset operator as it had envisioned.

After slashing its debt, selling its assets and securing the interim funding, the company will still need a profit-generating business to turn it around.

It remains to be seen how long the oil price can sustain above the comfortable operating level of US$80 per barrel.

But the biggest loser will perhaps be the shareholders, who are last in the queue.

When Sapura Energy undertook the RM10.3 billion refinancing last year, one of the conditions set was that PNB would need to maintain a minimum shareholding of 33% in the company across a seven-year period. Malayan Banking Bhd, a 49%-unit of PNB, was one of the lenders involved in the refinancing.

One analyst covering the sector opines that “PNB will have to make sure the entire exercise is successful or else Maybank is at stake”.

While PNB has said its investment in Sapura Energy represents less than 1% of its assets under management, it is worth noting that PNB pays dividends to its unitholders based on dividends and capital gains that it realises in its investments.

At four sen per share, the counter is trading at a discount of 90.7% to the group’s net assets of 43 sen per share as at end-October 2021. Its net assets include nearly RM4.9 billion of goodwill or 30 sen per share. Its market capitalisation now stands at RM559.27 million.

This brings the value of PNB’s 40% stake to RM223.71 million, less than 10% of the RM2.67 billion it injected in 2018, not including prior investments.

For the nine months ended Oct 31, 2021 (9MFY2022), Sapura Energy booked a net loss of RM2.28 billion on revenue of RM3.66 billion. This means that all three of its billion-ringgit annual losses happened in the last five years, including RM2.5 billion in FY2018 and RM4.6 billion in FY2020.

When Sapura Energy did its RM4 billion cash call in 2019, many had expected the capital injection to salvage the O&G giant.

Time will tell if the debt restructuring is the remedy for Sapura Energy. Hopefully, it is not wishful thinking that its vendors and contractors will also benefit from it, and that the company will not go belly up before the completion of the exercise.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments