Part 4: Still paying the price for capital controls 23 years later

In a little over two decades, Malaysia has gone from being one of the fastest-growing economies in the early 1990s, to the slowest in the region — in terms of per capita GDP. Not surprisingly, we failed to achieve our long-term ambition to become a high-income nation by 2020.

The stock market, Bursa Malaysia (formerly Kuala Lumpur Stock Exchange), too, has seen a sharp reversal in fortunes — from the heydays of the early 1990s super bull cycle to being a chronic underperformer. The FBM KLCI and FBM Top 100 Index consistently rank among the worst-performing indices in the last 5-, 10-, 15-, 20- and 25-year periods — compared with market benchmarks in Vietnam, South Korea, Thailand, Indonesia, the Philippines and Singapore. Back then, the KLSE’s market cap far exceeded those in all of these countries. Today, Bursa’s market cap is smaller than all but that of the Philippines. Malaysia’s weightage in the MSCI Emerging Market Index fell from a peak of 20% in 1994 to a little over 1.3% by end-2021, underscoring this comparative underperformance. For the past decade, Corporate Malaysia has been suffering from what appears to be a secular decline in revenue, profits and return on capital.

The average Malaysian is struggling to keep pace with the rising cost of living despite receiving comparatively high wage growth annually — because the majority of new jobs created over the years are low-paying ones. As a result, the national savings rate is in a long-term downtrend. Household debt has risen to the highest among our peers — second only to South Korea — even as we try to maintain our lifestyle. Much has been written about the looming retirement crisis, if nothing is done now, where large sections of the population will fall into poverty in old age over the coming 20 to 30 years.

We have written in depth about all of the above in a series of articles over the past few weeks. The question is: Why did the country perform so poorly? An analysis of the data since 1990 tells us that the Asian financial crisis (AFC) was a critical turning point.

Prior to the AFC, Malaysia had largely followed the conventional playbook — the structural transformation from a mining and primary commodities economy to a diversified agriculture-based one, to one driven by manufacturing and exports. Malaysians enjoyed strong income growth and a rising standard of living on the back of rapid development, urbanisation and industrialisation, especially through the late 1980s and early 1990s. The industrialisation strategy was fairly well executed, as were capital markets development plans, in lockstep with market-friendly, liberalisation and deregulation policies. The economy was further boosted by large-scale infrastructure projects and, at times, controversial privatisation (sometimes, piratisation) programmes.

Malaysia was hugely successful in attracting foreign investments and became a key regional electrical and electronic (E&E) hub. As we showed last week (“Part 3: Why Bursa is a chronic underperformer … low productivity growth and too many low-paying jobs”, The Edge, Issue 1410,

Feb 28), GDP per capita was the fastest growing in the region from 1990 to 1997, second only to South Korea. Over the next 22 years, from 1997 to 2019 (pre-pandemic), our GDP per capita growth ranked last (see Table 1). What changed?

The AFC severely affected and disrupted growth in the entire region, not just Malaysia. The crisis was, by and large, not of our making and beyond our control. Critically, though, our response diverged far from the conventional approach, which comes with tough reform requirements. Then prime minister Mahathir Mohamad imposed sweeping capital control measures, banning all offshore trading of Malaysian stocks and the ringgit, which was pegged at 3.80 to the US dollar. Proceeds from the sale of portfolio securities that had been held for less than a year had to be kept in ringgit in the country for at least a year.

The unorthodox capital control measures shielded the country from the worst of the crisis fallout in terms of the human impact — unemployment, wages and poverty levels, at least in the short term. It certainly protected many tycoons — who were saddled with huge debts, many of which were also denominated in foreign currencies — from bankruptcies. The measures, however, have deep and cascading negative effects over the longer term. The biggest casualty was investments, a critical growth driver and, we think, the root cause of Malaysia’s current malaise.

Capital control measures and the treatment of foreign portfolio investors during the AFC was harsh. Portfolio funds were initially prohibited from repatriating proceeds from share sales, which was then replaced by a graduated exit tax levy. This was later abolished — but the harm, we think, was done. The restrictions raised questions over the integrity of contracts and laws for all future potential investors, hurting confidence and raising the risk premium for investing in the country (see “CLOB got clobbered” on Page 16, on the suspension of shares trading on CLOB).

As a result of the capital controls, Malaysia was temporarily dropped from the MSCI EM Index in December 1998, which further compounded the negative sentiment and capital outflows, given that index benchmarking is widely used by both active and passive fund managers to measure their performances. At the same time that Malaysia was dropped from the benchmark index, South Korea was given full weightage, from 50% previously. Taiwan’s weightage in the index too was gradually lifted to fully reflect its market capitalisation by 2005.

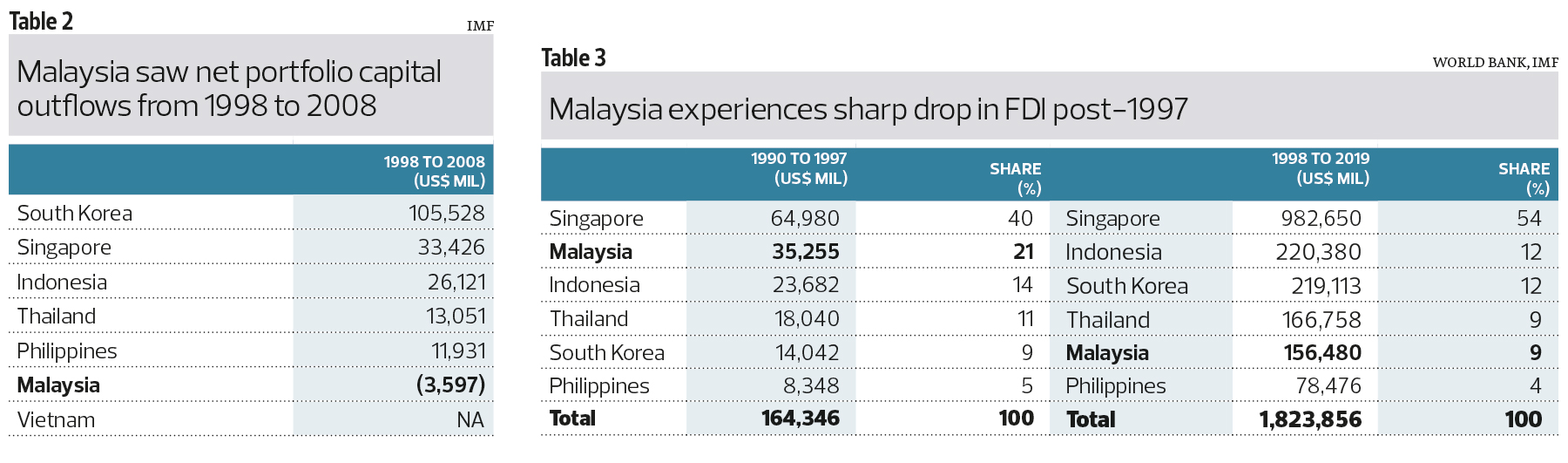

For the 10 years thereafter, from 1998 to 2008, Malaysia was the only country — among the five founding Asean members plus South Korea — to report cumulative net outflows of foreign portfolio investments (both debt and equity combined) (see Table 2). That must have hurt the development of our capital markets and is likely to have deprived many businesses of a valuable source of funding for investments and growth.

Although foreign direct investments (FDIs) were largely exempted from capital control measures, they too took a huge hit. We think this can be attributed in no small part to perceptions — as we said, restrictions on portfolio fund flows raised questions over the integrity of contracts and laws, which dampened investor confidence and raised the risk premium for investing in the country.

Malaysia attracted 21% of the total FDI flows into Asean-5 plus South Korea from 1990 to 1997, second only to Singapore. This share fell to just 9% from 1998 to 2019, the second lowest after the Philippines (see Table 3). Remember, FDI was the key driver for economic growth in the years prior to the AFC — not just in terms of capital but, importantly, also the transfer of technology and know-how, and the creation of supply chains and support ecosystems, and jobs.

There is no question that Malaysia lost out on foreign capital funding — from both FDI and capital markets — in the aftermath of capital controls. Perhaps even more critical is the time we lost — the years when Malaysia dropped off investors’ radar, and foreign money sought out investment opportunities in other newly emerging countries. China’s rise to become the world’s factory is most probably inevitable, but the rapid growth in countries such as Vietnam was likely to have been hastened by what transpired during the AFC.

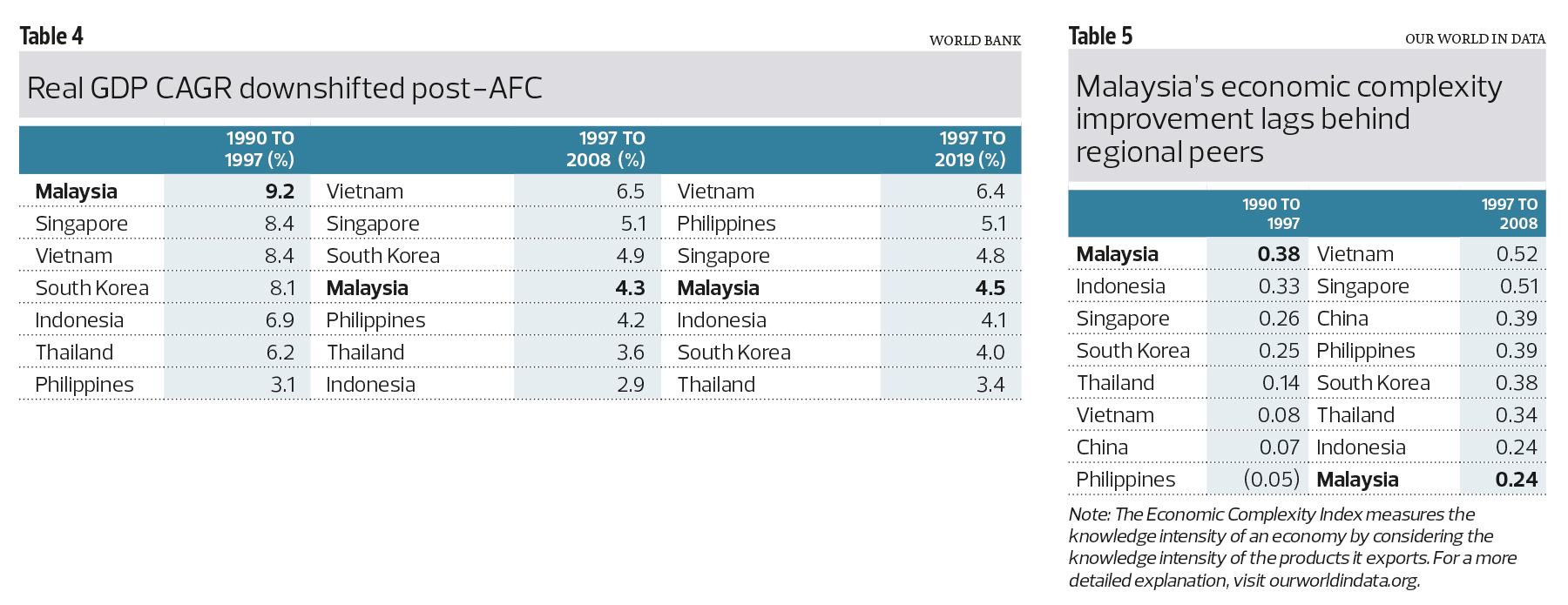

Reduced investments have deep and lingering repercussions on the economy. Gross capital formation as a percentage of GDP fell sharply, from a high of 43% in 1997 to an average of less than 24% in the following decade (1998 to 2008) — forcing a premature de-industrialisation of the country. Slower investments in new productive capacity translated to slower growth in potential output and actual GDP (see Table 4 on Page 18).

Reduced investments may have also played a critical role in slowing the move up the value chain and capping productivity gains. Malaysia’s economic complexity index — as reflected by the diversity and complexity of production and exports — showed the strongest improvements from 1990 to 1997 but fell behind not only that of the advanced economies of Singapore and South Korea but also that of its Asean peers and Vietnam (according to data compiled by Our World in Data) in the ensuing decade (see Table 5). Higher levels of complexity typically entail the creation of high-skilled, high-paying jobs and more sophisticated ecosystems — meaning, higher per capita GDP.

Stripped of investments as the primary driver of economic growth, the government then actively encouraged domestic consumption to drive the economy. This turned out to be yet another premature and unsustainable strategy — the income level of the average Malaysian was simply too low. It resulted in a sharp rise in household debt and precipitous decline in the gross savings rate. In 1997, Malaysia’s savings rate as a percentage of GDP was the second highest in the region, after Singapore. By 2020, our savings rate was near bottom, barely above that of Vietnam. Domestic savings is another important — and depleting — source of funding for investments.

As we explained last week, slow productivity gains, coupled with rising wages, led to falling corporate profits and return on capital. Low return on capital, in turn, means little incentive for new investments, including in mechanisation, automation, innovation and R&D that would improve productivity. This negative feedback loop is further compounded by the sense of complacency that cheap migrant labour will always be readily available.

Since the AFC, there have been few significant government policies as catalysts to promote productive investments and move up the value chain. Worse, the country has seen a slow deterioration in the quality of education and training. High-skilled, high-paying jobs as a percentage of total new jobs created declined, capping wage levels and accelerating the brain drain. Meanwhile, Singapore has successfully transformed itself into a global financial hub and regional tech centre. Vietnam is turning into a manufacturing powerhouse with the advantage of a huge reservoir of labour in its nearly 100 million population. When you keep running in place, others will pass you by.

The one sector that did grow rapidly after the AFC was property, no thanks to government policies promoting domestic consumption. Property, however, is largely non-productive investments, and did little to boost Malaysia’s competitiveness in global markets. Indeed, for the iconic projects, inevitably, the architects, engineers, contractors are — more often than not — foreign-based.

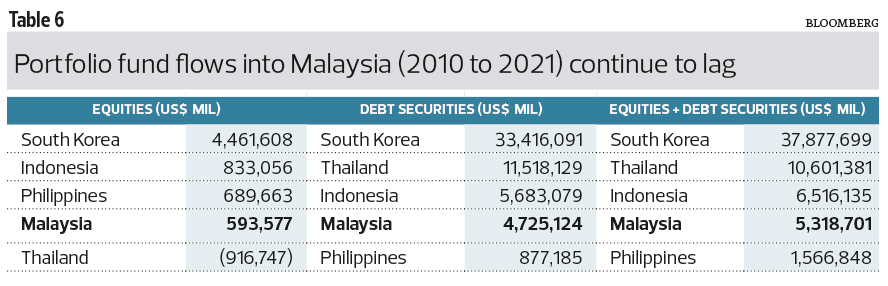

More than two decades after the AFC, Malaysia remains comparatively unattractive to foreign investors. Bursa reported net cumulative foreign equity fund outflows since 2010 while foreign shareholding in the local bourse has fallen to just 20.4%. Over the same period, cumulative fund flows into the bonds market too have been lower than for Thailand and Indonesia (see Table 6).

Clearly, Malaysia urgently needs fresh catalysts to put it back on the path to stronger productivity gains and per capita GDP growth. That requires renewed investment impetus in productive capacities. A successful digital transformation could drive efficiency and productivity gains.

Yes, there are many causes contributing to the decline in productivity-wage gains that is weighing on per capita GDP growth. They include the lack of meritocratic practices, rampant rent-seeking, deteriorating education standards and decisions that are driven — overly — by short-termism, among others. But there is no doubt that the AFC was a key turning point and the capital controls imposed then were a major trigger. Most of the capital control measures have long since been lifted. Yet, the unintended, long-term — and very costly — consequences are still felt to this day. It is a lesson we must not forget. Consistent, transparent and conducive government policies are critical. We conclude this four-part series by repeating a quote by Warren Buffett that we highlighted in Part 1:

“It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you’ll do things differently.”

The US stock market is seeing heightened volatility as the war in Ukraine continues to unfold. Worries over supply disruptions drove crude oil and gas prices sharply higher, flaming inflationary pressures. We disposed of our entire stake in BP plc, given prevailing uncertainties over its exit from Russia amid mounting political pressure. BP owns 19.75% of Russian government-controlled oil producer Rosneft Oil Co and has several other, smaller joint ventures in the country. Rosneft accounts for roughly one-third of BP’s oil and gas production.

The Global Portfolio gained 2.6% for the week ended March 2, recouping some losses from the previous week’s selloff. The biggest gainer for the week was CrowdStrike Holdings Inc (+24.7%). The cyber security sector is seen as benefiting from rising geopolitical tensions. Other notable gainers included Builders FirstSource Inc (+16%) and ServiceNow Inc (+11.9%). On the other hand, top losers included Alibaba

Group Holding Ltd (-7.7%), Taiwan Semiconductor Manufacturing Co Ltd (-5.4%) and Mastercard Inc (-4.7%). Last week’s gains boosted total returns since inception to 52.5%. This portfolio is outperforming the benchmark MSCI World Net Return Index, which is up 51.3% over the same period.

The Malaysian Portfolio, on the other hand, fell 2.4% last week. The big losers were Ta Win Holdings Bhd (-9.4%), Telekom Malaysia Bhd (-6.6%) and RCE Capital Bhd (-5.2%). Shares in Kuala Lumpur Kepong Bhd (+7.9%) did well on the back of record high prices for crude palm oil. Plantation companies will see bumper profits with the rising prices, much of which will go straight to the bottom line. Total portfolio returns now stand at 129.4% since inception. We are outperforming the FBM KLCI, which is down 12.7% over the same period, by a very long distance.

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments