The lure of small-scale solar

THOSE who are interested in Malaysia’s solar photovoltaic (PV) sector often point to the big industry catalysts such as the Large Scale Solar (LSS) scheme, which involves a capacity of 823mw under the latest round of contracts that were awarded in 2021.

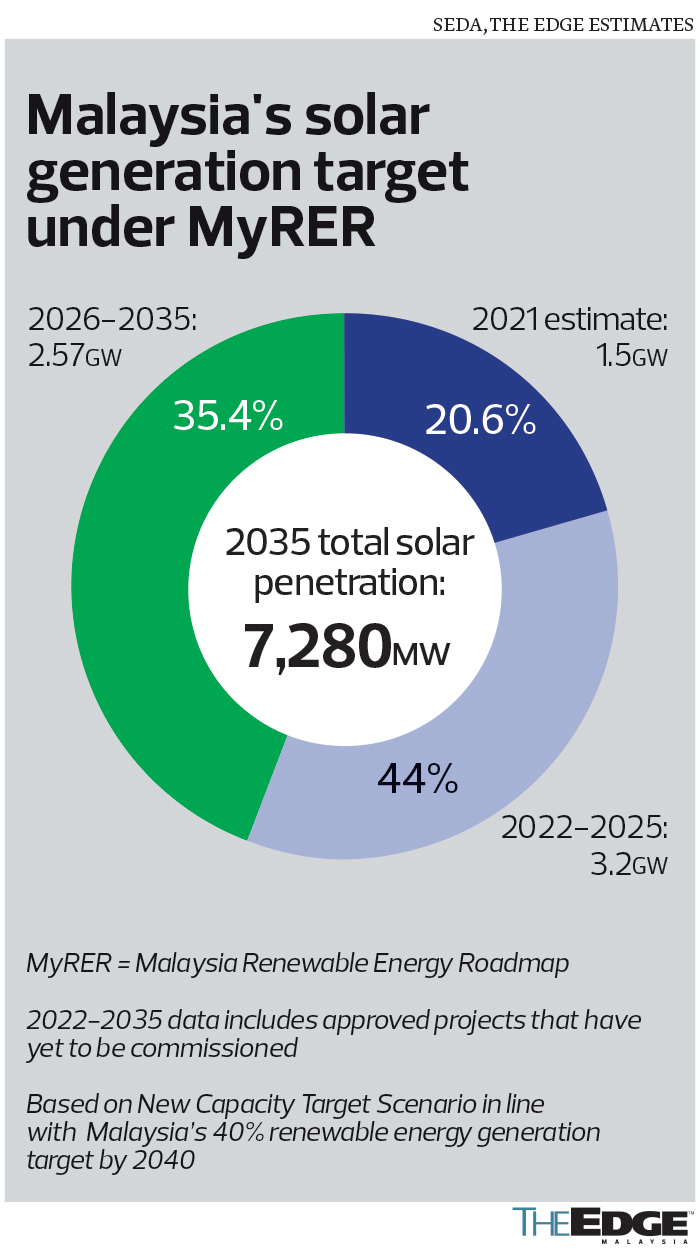

The LSS scheme, involving a total capacity of 2,327mw to date, is but one of the country’s many efforts to triple its installed solar capacity to 4,706mw by 2025 and 7,280mw by 2035 from an estimated 1,500mw in 2020, according to the Sustainable Energy Development Authority Malaysia (SEDA). The bulk of this capacity will come from rooftop solar installations on residential units as well as commercial and industrial (C&I) buildings.

Compared with the 10mw to 50mw of AC power (mwac) awarded to each successful bidder in the latest round of LSS contracts, rooftop solar projects are smaller at just 4kW AC to 5mwac. Past analyst estimates put a typical solar PV project construction value at about RM3 million to RM4 million per mw capacity.

Briefly, a solar project’s installed capacity is typically measured by megawatt-peak (MWp), which refers to the system’s power output under ideal conditions (as sunshine varies throughout the day), whereas MWac refers to the capacity of the inverters, which more closely resemble the actual generation after converting the solar-generated DC power to AC, as appliances in homes and businesses run on AC.

While the rooftop solar projects are smaller, a 2018 study by SEDA found that rooftop solar generation had a market potential of 18,000mw — way beyond Malaysia’s baseline target — suggesting that there is ample room to grow should the buy-in exceed expectations.

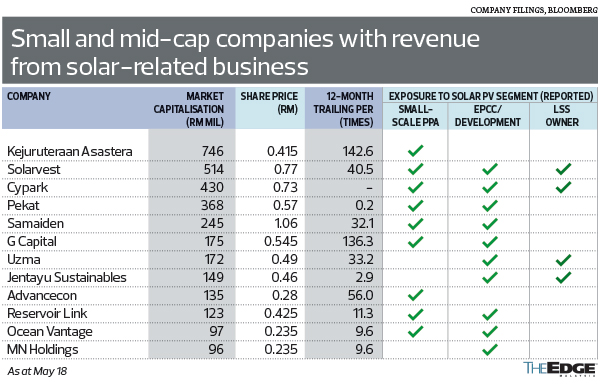

Even companies in unrelated sectors have acquired or set up a solar-dedicated unit to gain some exposure to this segment. At least 25 Bursa Malaysia-listed companies are tapping into the solar PV segment, many of which are looking at small-scale projects as well.

The new IPPs

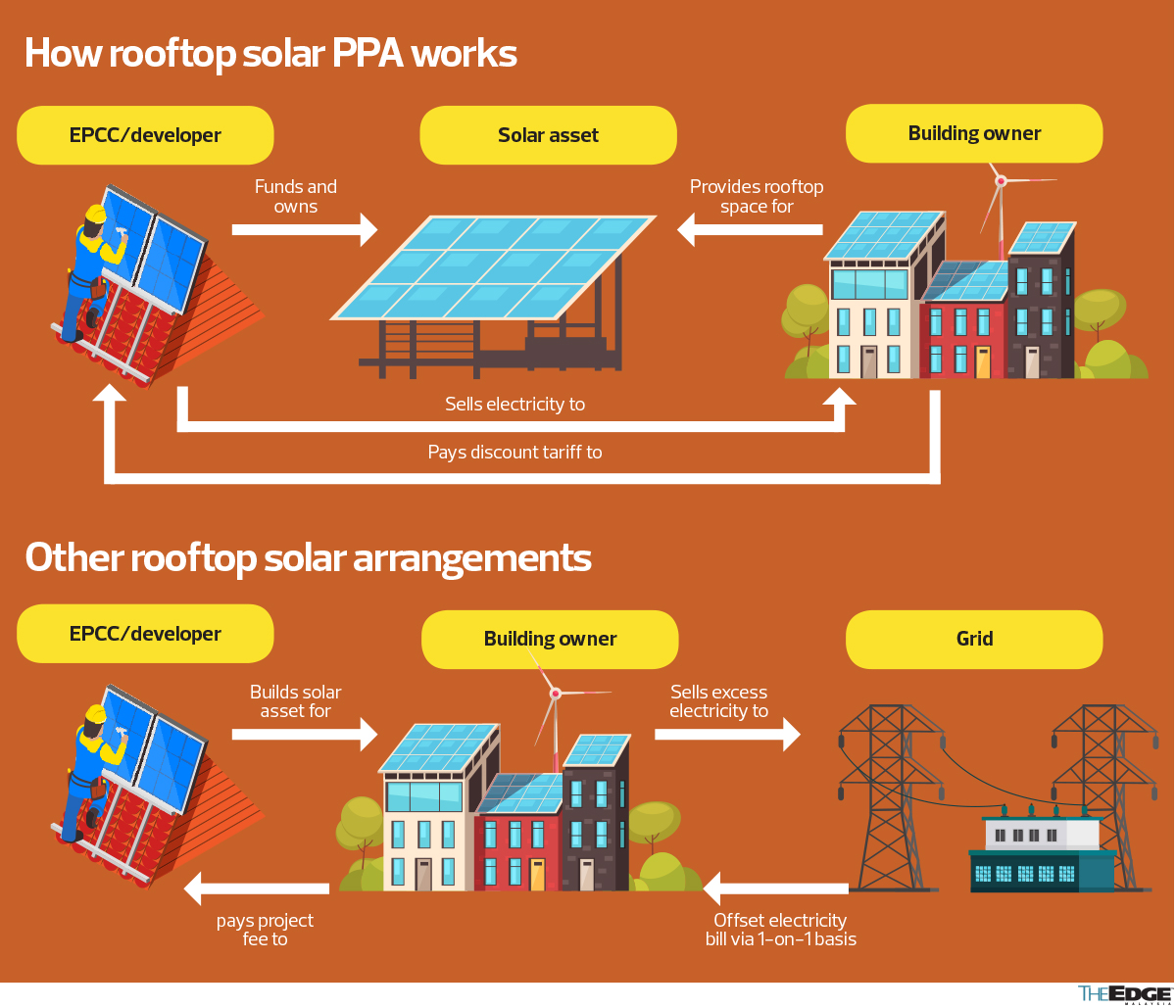

The latest hype is about companies inking power purchase agreements (PPAs) to sell solar-generated electricity — not to Tenaga Nasional Bhd, but directly to consumers.

These companies are paving the way for a new breed of independent power producers (IPPs) that do not rely on LSS projects. Instead, they are developing small solar assets, with each serving a single client in the C&I segment.

The PPA allows them to set their own electricity selling prices — typically around 15% cheaper than existing tariffs — and generate a mid to high single-digit internal rate of return based on how effective they are in procuring, developing and maintaining the solar asset.

The companies include ACE Market-listed Pekat Group Bhd. Its joint venture (JV) with Mega First Corp Bhd (MFCB) owns several solar assets on rooftops of buildings whose owners choose not to provide any upfront costs for installation, such as the 12mwp asset at Proton Holdings Bhd’s facility.

Under a 15-year PPA, Proton can buy electricity at a cheaper rate from the JV and reduce its carbon footprint, while the JV partners secure long-term recurring income. It is a win-win arrangement for both parties.

“Renewable energy is still the way to go. If you think electricity prices won’t go up, that is not correct,” Pekat Group Bhd chief operating officer Tai Yee Chee tells The Edge in a recent interview.

“Further, the corporate environment now has ESG (environmental, social and governance) compliance to deal with. The lowest-hanging fruit is to adopt a solar power generation system.”

Including Pekat, at least 11 listed companies plan to or have announced such PPAs, including pure-play solar companies Samaiden Group Bhd and GSPARX Sdn Bhd. Other players include G Capital Bhd (which is mainly in transport), Advancecon Holdings Bhd (earthworks), Reservoir Link Energy Bhd and Uzma Bhd (oil and gas), as well as Kejuruteraan Asastera Bhd (engineering). Pekat is also involved in the earthing and lightning protection business.

Small-scale EPCC

A number of these “mini IPPs” also build solar assets for C&I clients for a fee. These comprise building owners who wish to own the rooftop assets rather than sign a PPA, and residential unit owners, who must own the assets outright. The residential unit owners will have to fund the project themselves (financing is available), but will own all of the power generated, including excess power that can be sold to the national grid.

GSPARX, a unit of Tenaga, has secured 1,200 C&I and residential customers since 2018, involving a total capacity of 127mw. For residential assets installed through GSPARX, the cost ranges from RM3,900/kWp to RM4,500/kWp, which takes about one month to complete and about five years to see a return on investment, says Tenaga in an email reply.

Meanwhile, Pekat, whose mainstay is the C&I segment, points out that contracts in this space are smaller at RM1 million to RM10 million, compared with LSS projects that could fetch RM40 million for 10mwp. Still, this segment has helped the group grow its revenue at 66.35% per annum on average in the last four years.

Pekat chief commercial officer and solar division managing director Wee Chek Aik says the group will take on bigger projects at the right time, having had its first exposure as an engineering, procurement, construction and commissioning (EPCC) contractor for the LSS scheme with a 12mwp plant in Perak. “We have to factor in stronger fundamentals in terms of cash flow, as well as [look at] raw material prices and the labour situation.

“Of course, we are not satisfied with the amount of revenue we are achieving [RM176 million for the group] announced in 2021. That is not our ceiling.”

LSS beneficiaries

Due to its size, the EPCC segment of the LSS scheme remains attractive to bigger players, including pure-play renewable energy groups Solarvest Holdings Bhd and Samaiden, as well as O&G services group Uzma.

With its LSS project wins, Samaiden’s order book has jumped to RM377 million from less than RM50 million in 2020, while Uzma’s relatively new venture has secured more than RM100 million worth of EPCC jobs for the LSS scheme.

Other companies with exposure to the LSS space serve some niche segments. Newly listed MN Holdings Bhd, for instance, provides project management for LSS substations while O&G player Reservoir Link undertakes LSS construction and supplies solar mounting systems and AC/DC inverters.

Solarvest and Uzma are in the LSS4 scheme as project owners with 50mwac each, alongside Advancecon, with 26mwac. They are on a list of at least 14 Bursa-listed companies that aim to have large-scale solar assets locally or overseas. As the development of most LSS4 projects has yet to start, there is quite a bit of work to be dished out.

Big market, big competition

Rooftop solar installations can sell excess power to the national grid as it falls under the Net Energy Metering (NEM3.0) scheme. The scheme runs until end-2023 and still has 374.72mwac available.

Installations that do not sell excess electricity to the grid come under the Self Consumption (Selco) scheme. There is no limit to how many parties can apply for this scheme, be it on-grid or off-grid, hence, SEDA’s estimate of 18,000mw rooftop solar market potential.

The size of the Malaysian solar PV market has attracted even the national oil company Petroliam Nasional Bhd (Petronas) to participate. Its solar unit, Amplus Energy Solutions Pte Ltd, has grown its solar capacity under operation and development to more than 1,000mw in India, Malaysia and Dubai, servicing over 200 customers across more than 400 projects.

Despite the growing competition, Tenaga says GSPARX is confident of the market outlook for solar PV, especially in the C&I segment, as Malaysia transitions to the endemic phase of Covid-19 and businesses pick up in terms of production.

“Incentives such as the Malaysian Investment Development Authority’s Green Investment Tax Allowance are available to corporations that opt for solar PV, which would help to significantly reduce their payback period,” says Tenaga.

In its reply to The Edge, Solarvest acknowledges the growing competition, but points out that the situation varies depending on the project size. “To come on board as EPCC in a smaller-scale solar project may not be a huge challenge in this case, but to be able to compete for a high-profile project or bigger-scale EPCC, the entry barrier is still there.

“The scale that we are at, managing multiple projects simultaneously, requires years of accumulated experience to pull off. So, a track record matters.”

Pekat also acknowledges that the increased competition has slightly impacted margins, but emphasises that shorter project tenures help with cost management. “Last year saw an adjustment in margins, but we foresee it to be at current levels. The priority is to have a strong project profile, secure good clients — a mix of private sector and government — and secure projects with decent margins to sustain the business for the long term,” says Wee.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| ADVCON | 0.280 |

| BURSA | 7.470 |

| GCAP | 0.365 |

| KAB | 0.345 |

| MFCB | 4.680 |

| MNHLDG | 0.620 |

| PEKAT | 0.495 |

| RL | 0.330 |

| SAMAIDEN | 1.300 |

| SLVEST | 1.490 |

| TENAGA | 11.600 |

| UZMA | 1.280 |

Comments