Furniture makers sit tight, await uptick in orders amid headwinds

This article first appeared in Capital, The Edge Malaysia Weekly on November 27, 2023 - December 3, 2023

LOCAL furniture players have experienced a significant slowdown in orders since early this year, owing to tepid demand from US customers stuck with surplus inventories. That said, some of them have delivered a better quarterly financial performance on the back of a slight recovery in the furniture sector as well as strong US dollar, cushioning some of the negative impact of weak sales volume in North America, which is a major earnings contributor for many firms.

Analysts are generally optimistic of a gradual improvement in the furniture industry, but concede that the long-term outlook remains uncertain given a potential downturn in the global economy next year.

Thye May Ting, an analyst at PublicInvest Research, observes that a recent uptick in furniture orders was attributed to low inventory levels in the US. This positive trend is expected to be further boosted by the upcoming Christmas and Chinese New Year festivals, which will result in earnings spilling over to the first half of 2024.

However, she says the improvement may not be significant compared with the surge in earnings on a high-base effect during the pandemic period, when staying or working from home boosted furniture demand.

“We foresee the earnings going forward being supported by year-end festivals and prevailing demand, while the property sector remains sluggish in the near term due to the high interest rate environment, so we do not anticipate a huge spike in orders coming in,” Thye continues.

While the weak ringgit does help boost furniture earnings, she says the positive catalyst has already been priced in. Year to date, the local currency has depreciated about 7% against the greenback.

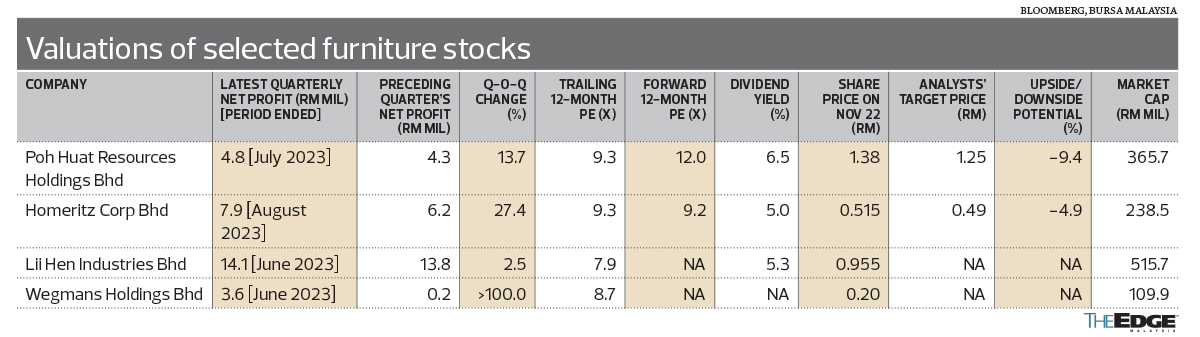

Underpinned by the strong US dollar, shares of furniture stocks have enjoyed some positive momentum in the past two to three months. Poh Huat Resources Holdings Bhd’s share price has gained 8.7% since early September, closing at RM1.38 last Wednesday for a market value of RM365.7 million.

Similarly, Lii Hen Industries Bhd is up 13.7% since end-August, closing at 95.5 sen last Wednesday and valuing the company at RM515.7 million.

TA Securities analyst Tony Chan is adopting a more cautious stance. Pointing to the continued decline in US existing home sales, he projects a more meaningful pickup in demand in the second half of next year.

“The slower furniture demand in the US was mainly hit by lower home sales on the back of the current high 30-year mortgage rate of around 7%. US existing home sales also dropped to the lowest level in 13 years. As such, I don’t expect any significant pickup in demand in the near term.

“However, the good news is it seems like the US Federal Reserve is likely to pause the interest rate hike following the cooling off of inflation. With that, the worst could be over and I expect the demand will pick up again in the second half of 2024.”

Sales of previously owned US homes fell by the most in nearly a year in October, highlighting the toll that elevated mortgage rates and still-high prices continues to take on the resale market, according to Bloomberg. Contract closings decreased 4.1% from a month earlier to a 3.79 million annualised pace.

Chan points out that the recent improvement in sales of local furniture players was partly due to the replenishment of US warehouse stocks and ahead of the upcoming Christmas sales. “Hence, I think we need to wait for another two more quarterly results to have a more concrete conclusion on the sustainability of the [furniture makers’] financial performance.”

Citing the recent collapse of furniture stores such as Klaussner Furniture, Noble House Home Furnishings and Mitchell Gold + Bob Williams, he highlights the challenges faced by the global furniture industry.

Nonetheless, local furniture makers are expected to benefit from the weak ringgit environment, says Chan. “We expect some of them are likely to register stronger results due to better profit margins as a result of favourable forex movements.”

Chan’s top pick for the sector is Poh Huat as it is seen to be a proxy for the US furniture recovery next year because more than 90% of its revenue is derived from North America. Furthermore, the Johor-based furniture firm is supported by an undemanding valuation and a decent dividend yield.

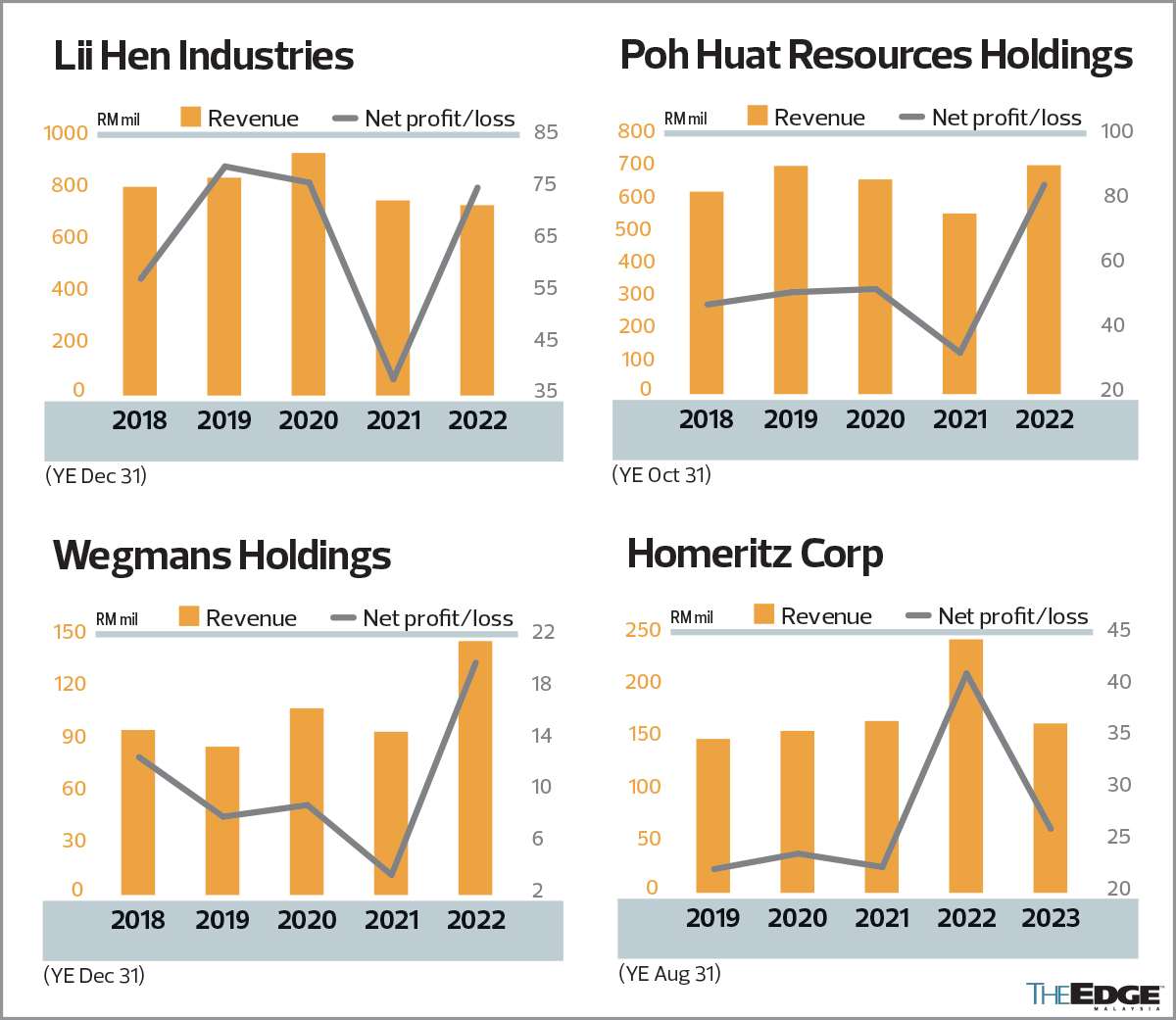

A strong net cash position of RM288.5 million and zero borrowings also put Poh Huat in a strong position to sail through near-term headwinds. For the nine months ended July 31, 2023, the company posted a 73.7% decline in net profit to RM15.9 million from RM60.5 million in the same period a year ago, as furniture importers in North America held back orders while focusing on clearing inventory.

Net profit for the May-July quarter was higher at RM4.8 million compared to RM4.3 million in the February-April quarter, mainly attributable to the higher level of production activities.

Bloomberg estimates show that Poh Huat could register a much stronger August-October quarter to wrap up the current financial year (FY2023) with a net profit of RM32.35 million, before rebounding to RM44.45 million and RM48.7 million in FY2024 and FY2025 respectively.

Poh Huat is also of the view that the US housing slowdown and weaker furniture spending will continue for some time. “We have scaled back our operating hours and workforce in line with the reduced orders. We are now working with our customers to develop a newer range of products, particularly for the office segment which has weathered the slowdown better while anticipating a pickup in our home furnishing orders towards the year-end Christmas festival peak,” it said last August when announcing its 2Q financial results.

Homeritz Corp Bhd and Lii Hen Industries were also in a net cash position, the former with RM170 million as at end-August and the latter with RM187.4 million as at end-June.

Financially, Wegmans Holdings Bhd posted the biggest jump in net profit of 21 times to RM3.6 million for the April-June period, from RM167,000 in the preceding quarter, driven by higher sales volume from North America which contributed nearly 60% of its sales. For FY2022, its net earnings also soared significantly to RM19.8 million from RM3.4 million in the previous year, also owing to higher sales from North America, the stronger US dollar and the absence of the Movement Control Order in Malaysia.

Despite the external headwinds faced by the furniture sector, a relatively higher dividend yield for some furniture stocks could be an attractive investment option for investors.

Poh Huat has the highest dividend yield of 6.5%, as it paid out an eight sen dividend for FY2022. For 9MFY2023, the dividend payout was five sen per share.

Lii Hen Industries and Homeritz offer dividend yields of 5.3% and 5% respectively.

According to the Department of Statistics, the total value of Malaysia’s wooden furniture exports was estimated at RM11.1 billion in 2022, of which the US accounted for more than half at RM6.27 billion (56.3%). Other key export markets were Singapore (RM609.6 million, or 5.5%), Japan (RM602.4 million, or 5.4%), Australia (RM517.8 million, or 4.6%) and the UK (RM405.3 million, or 3.6%).

In 2020 and 2021, total exports of wooden furniture amounted to RM10.6 billion and RM10.4 billion respectively.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| HOMERIZ-WC | 0.000 |

| POHUAT | 1.470 |

| WEGMANS-WC | 0.020 |

Comments