Furniture exporter finds synergy in e-commerce

This article first appeared in The Edge Malaysia Weekly on March 25, 2024 - March 31, 2024

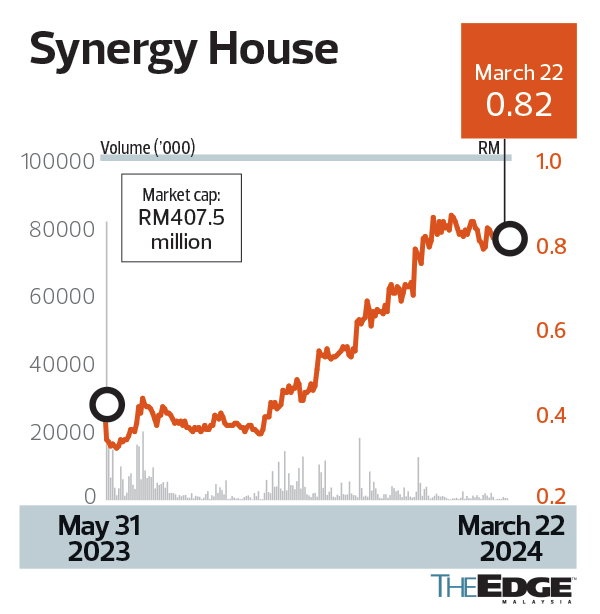

SYNERGY House Bhd was one of the few ACE Market initial public offerings (IPOs) in 2023 that surprisingly underperformed on its debut, opening nearly 12% lower than its 43 sen offer price.

However, those who had subscribed for its shares then and held on would be well pleased with the stock’s subsequent performance, which after the initial hiccup in June began to pick up momentum in November and further pace this year. By last Friday’s close, it had put on a hefty 134% to close at 82 sen a share, valuing the company at RM407.5 million.

The furniture exporter’s timely pivot to e-commerce — particularly the overseas business-to-consumer (B2C) segment — continues to pay off handsomely, propelling its share price, but some question if this growth is sustainable given the economic slump in key markets.

While demand for furniture exports is seen to be ebbing after players enjoyed a high growth run during the Covid-19 pandemic, the little known e-commerce furniture exporter expects to maintain an annual revenue growth rate of at least 30% as it taps ongoing demand from its target markets in the US and UK.

Synergy House’s senior management says it expects growth to be driven by its overseas B2C segment, which has delivered thanks to a timely pivot to e-commerce just before the Covid-19 pandemic struck in 2020.

The company, which is a cross-border e-commerce seller and furniture exporter with a niche in in-house designed and affordable ready-to-assemble (RTA) home furniture, has businesses that are segmented into business-to-business (B2B) and B2C.

The group’s offerings include furniture for the bedroom, living room and dining room and it is highly dependent on the US and UK markets for its revenue growth.

Speaking to The Edge at the Synergy House headquarters in Setia Alam, Selangor, the group’s non-independent executive director Tan Eu Tah, non-independent executive director Teh Yee Luen and chief financial officer Kenneth Ng explain how e-commerce has been a game changer for the group and will drive its growth to the next level.

Synergy House Furniture Holdings Sdn Bhd, the private vehicle of Tan and Teh, controls Synergy House with a 74% shareholding.

The successful take-up of Synergy House’s goods on overseas online platforms is reflected not just in its revenue growth over the past four years, but notably, in the hike in revenue contribution from the B2C segment, which spiked exponentially to RM121.7 million (45%) in FY2023 from RM5.3 million (4%) in FY2020.

Ng says while the B2B segment has been “steady” — thanks to long-term customers — B2C sales contribution grew significantly as Synergy House commenced selling on Wayfair US in 2020, followed by Wayfair UK, Amazon US and Amazon UK in 2022, as well as Mano Mano, eBay UK, Cenports US, Wayfair Canada and Wayfair Germany thereafter.

In the last five years, group revenue grew 142% to RM270.2 million in FY2023 from RM111.48 million in FY2019. Net profit grew to RM27.15 million from RM10.9 million, giving the group profit after tax margins of up to 10%.

The group’s net profit for the fourth quarter ended Dec 31, 2023 (4QFY2023) came in at RM10.27 million, 27.3% higher than RM8.07 million in the preceding quarter. Revenue was 31% higher at RM90.77 million while the net profit margin decreased slightly to 11.3% in 4Q from 11.7% in the preceding quarter, as depreciation of the greenback towards the year end resulted in net foreign exchange losses of RM1.3 million in 4QFY2023.

“In order to mitigate forex risks, our overseas businesses are conducted in various currencies, also to reduce dependency on the US dollar,” says Tan.

For a rough idea of the operating margins of Bursa Malaysia-listed furniture players in FY2023, Synergy House’s and Lii Hen Industries Bhd’s stood at 16.8% and 11.41% respectively, while Poh Huat Resources Holdings Bhd’s was 9%.

It should be noted, however, that the latter two are not pure play e-commerce furniture outfits that fully outsource their production but, on the contrary, are furniture manufacturers.

While some quarters are convinced of Synergy House’s revenue growth potential, there are concerns about the group’s ability to sustain the momentum of the last few years.

Sceptics point to the downward trend in Malaysia’s furniture exports owing to a high furniture inventory situation in the US and economic downturn in the US and UK — both major markets for Synergy House. In fact, data from the Office for National Statistics show that the UK economy entered a technical recession in 4Q2023 as households there cut back on spending amid soaring prices, including for petrol and diesel.

Naysayers are also cognisant of Plantation Industries and Commodities Minister Datuk Seri Johari Abdul Ghani’s recent report stating that the timber and furniture industry has not been insulated from the effects of global headwinds, with the exports of timber and timber products falling by 13.2% to RM21.9 billion in 2022 and furniture exports declining by 18.1% to RM9.1 billion in 2023. A weakening of housing demand in the US has been highlighted since it is the biggest buyer of Malaysian furniture and accounts for more than half of furniture exports, according to Johari.

To quell concerns as well as explain the premise behind Synergy House’s targeting of the US, Canada and selected countries in Europe as its primary markets, Ng walks The Edge through its working processes, which rely heavily on transaction data, artificial intelligence and IT, to track sales conversions as well as to project buyer patterns and market needs.

Tan and Teh concede that the global furniture e-commerce space is highly competitive, hence Synergy House’s investment of more than RM2.2 million in IT and market intelligence software in the past three years, and a further allocation of RM1 million for IT software and hardware this year.

Tan points to a map of the US displaying historical indications of the company’s product transactions and pages of data. “Towards the east are the major cities to which young adults or families move to start or advance their careers. As they move into a new or rented place, they need basic and affordable furniture such as beds and wardrobes. The downtrend in furniture exports could be telling of high-value furniture items or material for the long term such as fittings.

“However, our products are very affordable and as our records show, easily bought for the short term for this transient demographic. In fact, the most expensive item we sell is priced at no more than US$300 (RM1,422).”

This, he says, explains why concerns of high inflation and soaring living costs in Europe “are worrying but do not mean that people will stop buying necessary furniture, as reflected in Synergy House’s records”.

“This year, we are targeting four new platforms as we widen our range of B2C stock keeping units to more than 2,000 by the year end from 1,608 in 2023, and to commence B2C sales in France. We will expand on Amazon Germany, Amazon Canada, Amazon France and Mano-Mano France,” says Tan, adding that high-income nations with vast populations of young adults and budding families are targeted.

“We will launch new product categories, including home improvement items such as vanity furniture, children’s bunk beds, sofas, wooden flooring and wooden doors,” adds Teh.

RHB Research, in a Jan 15 report, says Synergy House’s evolution from being a (traditional) manufacturer in 1990 into a pure-play furniture distributor that fully outsources manufacturing works sets it apart from other listed furniture players.

“Thanks to its asset-light business model (operating in lower-cost Asian nations like Malaysia), the group can now channel all resources into design and development, going from 360 designs in 2019 to a whopping 2,500 as of December 2023. As Malaysia’s only cross-border e-commerce furniture distributor, Synergy has a foothold in the US, the UK, and United Arab Emirates via its RTA furniture exports. These are considered affordable fast-moving consumer goods,” says RHB Research, noting the company’s price-earnings ratio of 12 times, 9.5 times and 6.9 times for FY2024 to FY2026, with PE growth of 0.33 times and return on equity of 30%.

The research house recommends a “buy” on the stock with a target price of RM1.08.

“In the worst-case scenario, the company’s revenue is flat. Its growth is still remarkable,” remarks former investment banker Ian Yoong, who says he acquired shares in Synergy House, post-IPO.

While Synergy House does not have a dividend policy, it announced first and second interim dividends per share of one sen (paid) and 0.6 sen (payable) respectively for FY2023, translating into a 2% yield.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments