Analysts upbeat on Wasco’s outlook after 3Q earnings meet expectations

KUALA LUMPUR (Nov 29): Analysts are upbeat on Wasco Bhd’s outlook after the pipe-coating solutions provider’s results for the third quarter ended Sept 30, 2023 (3QFY2023) came in within expectations.

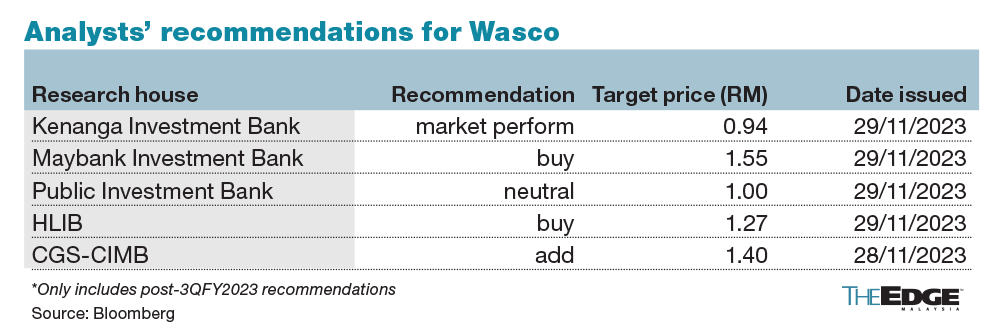

In a note on Wednesday, HLIB Research said Wasco’s 3QFY2023 core net profit of RM20.8 million lifted core earnings for the nine-month period ended Sept 30, 2023 (9MFY2023) to RM49.9 million — 68% and 71% of the research house’s and consensus’ full-year expectations respectively.

“We (HLIB) deem the results to be in line with our estimates, as we expect sequential stronger earnings in the coming quarter,” said the firm, maintaining a “buy” call on Wasco, with an unchanged target price (TP) of RM1.27 — 12 times forecasted FY2024 earnings-per-share (EPS).

The research firm said Wasco’s current outstanding order book stood at an elevated RM3.6 billion as at September 2023, providing a strong earnings outlook in the coming quarters, as the group enters into a “steep recognition cycle” for projects in hand.

“We note that Wasco has recently secured a US$34 million contract from Schneider Electric France for the supply of pre-fabricated buildings for a project in Africa, as well as a US$13.4 million contract from Nederlanse Gasunie in relation to pipe coating services for a carbon capture and storage project,” said HLIB.

“Contract flows will remain resilient, as upstream activities are picking up in the oil and gas sector, due to favourable oil prices. With a tenderbook amounting to RM7 billion (historical success rate of circa 30%), management guided that most will likely be awarded next year. We also expect a sequential stronger performance in 4QFY2023, as management hinted more work progress is being executed in the last quarter,” it added.

Maybank Investment Bank (Maybank IB), which deemed that Wasco’s 9MFY2023 core earnings came in at 68% of its full-year estimates, has forecasted the group to record a 36% net profit growth in FY2024, as it understands that the bulk of the accelerated progress billings for the RM1.1 billion East African crude oil pipeline project and the RM558 million Yinson projects will be recognised next year.

“Current completion rate for both projects stands at 37% and 31% respectively,” it said in a note.

Maybank IB maintained its “buy” call on Wasco, with a higher TP of RM1.55 — pegged to 12 times FY2024 price-to-earnings.

Wasco’s 9MFY2023 core earnings also fell within Kenanga Research’s expectations at 73.4% of his full-year estimate.

“We (Kenanga Research) maintain our ‘neutral’ call and TP of RM1.00, pegged on 11 times multiple of FY2024 EPS,” Kenanga Research said in a note on Wednesday.

At the time of writing, Wasco’s shares were up 3.5 sen or 3.7% at 98 sen, valuing the company at RM755.44 million.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| WASCO | 1.510 |

Comments