my Say: Extraordinary rebound disguises structural weakness

The latest figures from the Department of Statistics Malaysia (DOSM) for gross domestic product (GDP) in the third quarter of 2020 show an extraordinary rebound in economic activity after the steep decline in the second quarter.

All of the components of aggregate demand bounced back so strongly that activity in 3Q almost exactly offset the contraction in 2Q. Measured on an annualised quarterly basis, GDP grew more than 95% and both consumption and investment grew more than 122% and 139% respectively.

If we compare Malaysia’s performance with the countries that showed the strongest rebound in 3Q on an annualised quarter-on-quarter basis, which projects the quarterly growth over the full year, Malaysia’s GDP grew around 95% in 3Q; Mexico grew 54%; Singapore, 34%; and the US, 33%. So, the rebound in Malaysia was two or three times greater than the best performers globally.

Compared with previous downturns, the rebound in 3Q this year is around three times as fast as we experienced during the Asian financial crisis in 1997/98 and around five times as fast as after the global financial crisis in 2008. So, this is an extraordinary recovery in all senses of the word.

This suggests that the short-term raw data reported by DOSM may be overshooting a more realistic long-term adjustment path for the economy after the acute phase of the Covid-19 crisis in 2Q. So, the latest data may not be representative of the likely outcome of the economy over the next few quarters and we may see a revision of these numbers in future statistical releases.

To understand what these more realistic long-term adjustment paths might look like, we need to first consider what is likely to happen with the Covid-19 pandemic locally and internationally and, second, what the quality of the post-Covid-19 growth will be, which we can gauge from some key economic ratios.

In terms of Covid-19, the most positive outcome would be that effective management of the pandemic or the early rollout of successful vaccines reduces the impact and allows the economy to recover, albeit in a “new normal” environment. The negative scenario is that persistent lockdowns continue to hold back the economy and perhaps get even worse.

Under the positive scenario, we expect GDP growth to be around 6.5% in 2021, in line with official projections. We then expect growth to settle at around 4% in 2022. The 6.5% growth path can be split into two parts — the first, around 3.0%, reflecting the long-term growth of the economy and, the second, around 3.5%, owing to the low base in 2020. We expect that GDP will reach its pre-crisis level only in 4Q2021. Prices will stop falling and inflation will stabilise below 2%.

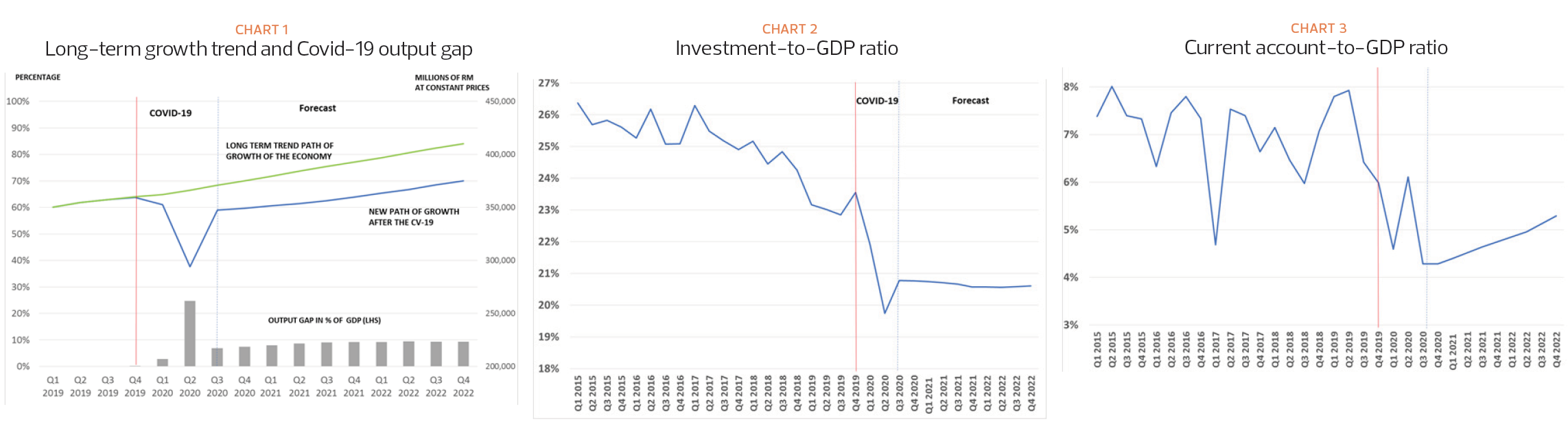

Despite this positive rebound, the impact of the virus crisis is likely to shift the economy from the previous long-term growth path to a lower trajectory. We calculate the structural loss of GDP to be around 10%.

In addition, while the long-run average rate of growth in the last few years was around 5% a year, the new long-run growth rate is likely to be lower at 4% by the end of the forecasting period. The underlying potential growth rate will be about one percentage point lower after Covid-19 compared with before because of a loss of competitiveness, lower productivity and decline in fixed investment. This will be made worse by a hollowing-out of productive capacity as firms close and fail to reopen, and may also be exacerbated by long-term unemployment or underemployment in low-paying, low-value-added forms of work (see Chart 1).

The very positive evolution of the economy in 3Q may mask some warning signs in terms of the quality of the growth. The two main engines of Malaysian economic growth — investment and exports — have been deteriorating for some time. The ratio of fixed investment to GDP and the current account balance, exports minus imports, as a percentage of GDP are shown in Charts 2 and 3. Both show a trend deterioration made worse by the Covid-19 impact.

Investment is the engine of the economy and, measured in terms of the investment to GDP ratio, began to weaken as early as 2018, from around 25% of GDP to a clear downtrend, which accelerated during the Covid-19 period to around 20%. Even if the strong 3Q rebound interrupts the downtrend, we expect investment to stabilise and consolidate around that value for the next two years.

Net external demand, measured in terms of the current account ratio to GDP, has also been hit by the Covid-19 shock — from being previously stable at 5%-8%, it has shifted down during the crisis and is likely to stabilise in a much lower range of 4%n to 6%, which reflects a deterioration of Malaysian competitiveness.

The modest growth forecast for 2022 depends on the weakening of the long-term determinants of consumption. The Covid-19 crisis has caused a significant loss in employment and has cut the purchasing power of salaries. This will hold back disposable income and drag consumption in next few years.

The positive outcomes depend completely on a successful resolution of the Covid-19 crisis. If we have a continuation of lockdown, restrictive measures and uncertainty around the impact of the virus, there will be a negative impact on the economy, locally and internationally. This will make the positive outcomes unlikely and risk a long phase of recession complicated by the risk of deflation through 2021 and beyond.

Dr Paolo Casadio, Dr Hui Hon Chung and Dr Geoffrey Williams are economists at HELP University based in Kuala Lumpur. The views expressed here are their own.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Comments