Brokers Digest: Local Equities - Sports Toto Bhd, Sunway Construction Bhd, Gamuda Bhd

UOB KAY HIAN RESEARCH (JAN 3): 2023 should be a warmer and less turbulent year for Malaysian equities, although sentiment would likely be frigid for most of 1H23 before turning positive around midyear, ahead of the prospect of a global economic recovery towards end-2023.

Our end-2023 FBM KLCI target of 1,640 points incorporates a valuation buffer of -0.75 standard deviation (SD) to the historical PER mean versus the pre-pandemic years’ year-end valuation of +0.5SD. While we envision that the unity government will remain the country’s ruling coalition, the key political events to monitor are Umno’s upcoming election (in April or May) and PAS’ momentum in this year’s state elections (in Kedah, Kelantan, Terengganu, Penang, Selangor and Negeri Sembilan).

Stay highly defensive but maintain exposure to key investment themes such as China’s border reopening. High-dividend yielders, particularly ones with back-end dividends, greatly appeal as value preservers. We would turn risk on towards end-2Q23 in anticipation of the market pricing in a global economic recovery towards year end. We would position for semiconductor-related stocks to stage an upward trend earlier than the index.

The key structural themes relate to trade diversion arising from the US’ sanctions against China and the green agenda. The compelling winners within our coverage of the first theme are Penang-based automation and semiconductor production equipment (SPE) companies.

The green agenda theme is uplifting for industrial commodities and particularly hydro-powered Malaysian smelters, suppliers to the electric vehicle (EV) supply chain and selected oil and gas (O&G) offshore-oriented (FPSO and jack-up rig) companies.

The cyclical themes relate to the turning point of the downtrodden semiconductor stocks, economic reopening themes (Asia’s border reopening and ramp-up of foreign worker hiring in Malaysia), as well as China’s emergence from lockdowns and border reopening. Other meaningful investment themes include blockchain trading platforms, the O&G sector’s rising return on investment for offshore assets (FPSOs and jack-up rigs), and the eventual MRT3 contract award.

We are overweight on defensive sectors such as consumer staples, gaming, healthcare, REITs and, selectively, the building material, O&G and technology sectors.

Our top stock picks have been recalibrated to be more defensive, but remain a blend of back-end-dividend yielders (Genting Malaysia Bhd, TIME dotCom Bhd), and alpha-driven thematic beneficiaries such as China’s reopening (Malaysia Airport Holdings Bhd) and the green agenda (Greatech Technology Bhd, Press Metal Aluminium Holdings Bhd, Yinson Holdings Bhd) beneficiaries. We dropped CIMB Group Holdings Bhd and VS Industry Bhd, and added Sunway REIT.

We categorise high yielders into three groups — stocks having back-end dividends, anticipated special dividends and high absolute yields. Stocks that fit this defensive theme are British American Tobacco Malaysia Bhd and Sunway REIT (high absolute yields), Hap Seng Plantations Holdings Bhd and RHB Bank (back-loaded dividends), and Genting Malaysia and TIME (special dividends).

Other notable “buy” calls include trade diversion beneficiary Pentamaster Corp Bhd, green agenda beneficiary OM Holdings Ltd, reopening and cyclical recovery beneficiaries Genting Bhd and SKP Resources Bhd, O&G beneficiary Bumi Armada Bhd and Gamuda, the frontrunner to clinch a sizeable MRT3 contract in 1H23.

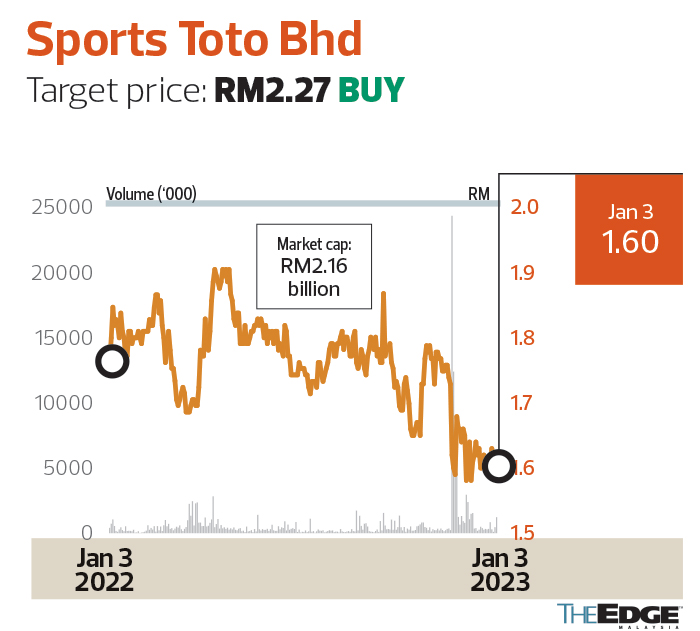

Sports Toto Bhd

Target price: RM2.27 BUY

HONG LEONG INVESTMENT BANK RESEARCH (JAN 3): The Kedah menteri besar announced a ban on all number forecast operators in the state effective Jan 1, 2023, by not renewing business licences. While this is a negative development, we believe the earnings impact from the closure of outlets will be moderate as it represents only 2.9%, or 20, of Sports Toto’s total outlets.

Kedah has a predominantly Muslim population and the impact is cushioned by Sports Toto’s growing luxury car dealership segment in the UK, which contributed 32.1% of the group’s Ebit in FY22. There is a risk of Perlis following suit, but the impact would still be manageable as the state has only four, or 0.59% of the total 680 outlets.

Following the closure of the 20 outlets, the Ministry of Finance — which awarded the gaming licences — could either allow a relocation to other states or revoke the licences.

We maintain “buy” with an unchanged target price of RM2.27. Following a slew of negative announcements, including the recent reduction in special draws from 22 to eight and the closure of Kedah NFO outlets, sentiment for the stock may be weak in the near term. Nonetheless, we expect the aforementioned events to have minimal impact on earnings. The stock currently offers a generous dividend yield of 8.6%.

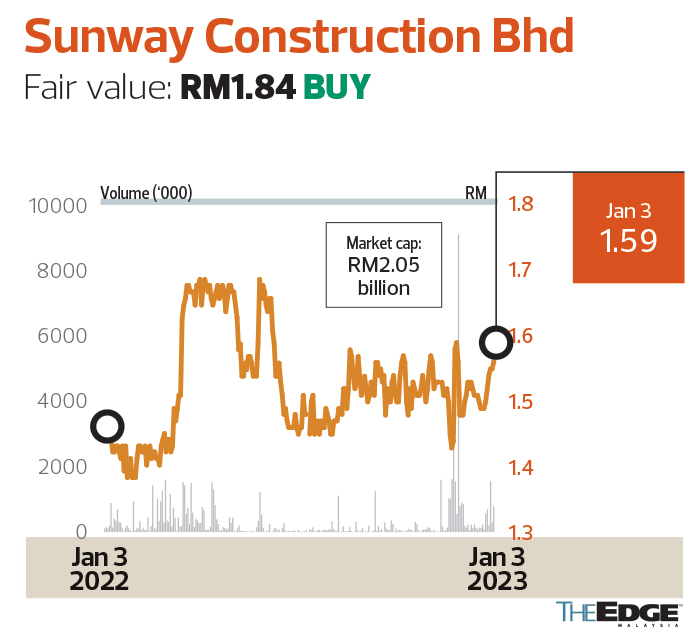

Sunway Construction Bhd

Fair value: RM1.84 BUY

AMINVESTMENT BANK RESEARCH (JAN 3): We upgrade Sunway Construction (SunCon) to “buy” with a higher fair value of RM1.84 (versus RM1.51 previously). We believe the stock is attractive given its 18% upside to our revised fair value and is currently trading at an undemanding FY23 PER of 12 times, being 13% below our benchmark of 14 times for large-cap construction companies.

SunCon secured a substantive contract worth RM1.7 billion to design, develop and construct a data centre in Sedenak Tech Park in Johor for Yellowwood Properties, which is expected to be completed in 3QFY24. Excluding this award, total projects secured in FY22 amounted to RM900 million, lower than our replenishment assumption of RM1.2 billion for the year. We now assume an order book replenishment of RM2.9 billion for FY23 versus RM2 billion previously.

Based on SunCon’s estimated share of pre-tax profit from the contract at RM64 million in FY23, or 39% of FY23 net profit, we raise its net profit by 22% for FY23 and 15% for FY24 to account for the higher order book replenishment assumptions. Potential replenishment may come from the construction of semiconductor plants and internal building jobs. We also believe the company is well positioned to secure MRT2 jobs due to its strong balance sheet and proven track record in MRT1 and MRT2.

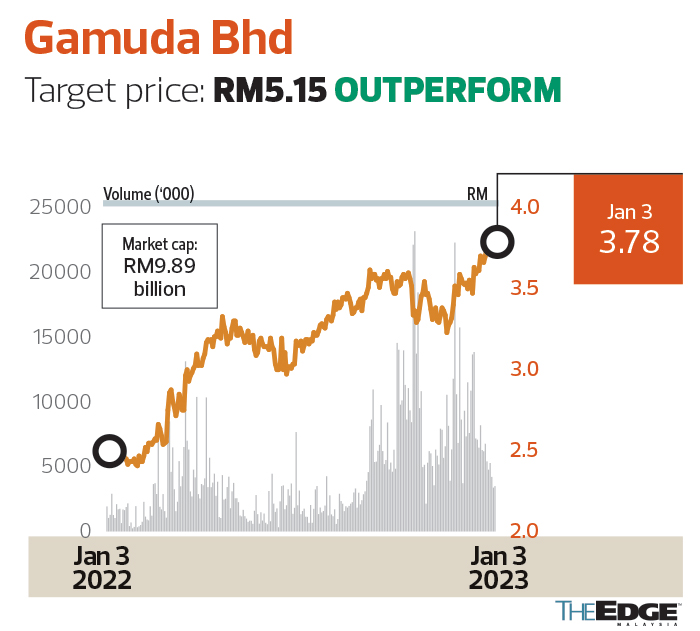

Gamuda Bhd

Target price: RM5.15 OUTPERFORM

KENANGA INVESTMENT BANK RESEARCH (JAN 3): Gamuda Bhd is acquiring eight adjoining parcels of freehold land in Kundang Jaya, Rawang, with a total area of 532 acres for RM360 million, translating to about RM15.50 psf. With a tentative gross development value (GDV) of RM3.3 billion spanning a 10-year horizon, the land parcels are earmarked for a mixed-use development (mainly landed residential) and are located close to the ongoing 810-acre Gamuda Gardens development.

We are mildly positive as the land will enable Gamuda to broaden its product offering in Rawang to include affordable landed houses, despite little accretion to earnings in the immediate term.

There is no change to FY23-FY24 earnings as the land will not contribute to the forecast periods. Maintain “outperform” with an unchanged target price of RM5.15, based on 15 times earnings for its construction segment. We continue to like Gamuda for the good chance of it securing the MRT3 job; its recent job wins in Australia, Singapore and Taiwan that speak for its competitiveness in the international market; its net cash position as at 1QFY23, which gives it an edge when participating in public infrastructure projects on a PFI or deferred payment model; its strong earnings visibility underpinned by a record-high order book of RM16 billion; and efforts to expedite growth in renewable energy in line with global sustainability goals.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| ARMADA | 0.590 |

| BAT | 8.190 |

| CIMB | 6.660 |

| FBMKLCI | 1569.250 |

| GAMUDA | 5.250 |

| GENM | 2.620 |

| GENTING | 4.520 |

| GREATEC | 4.470 |

| HSPLANT | 1.870 |

| OMH | 1.470 |

| PENTA | 4.200 |

| PMETAL | 5.380 |

| REIT | 831.230 |

| RHBBANK | 5.510 |

| SKPRES-WB | 0.055 |

| SPTOTO | 1.390 |

| SUNWAY | 3.470 |

| VS | 0.930 |

| YINSON-WA | 0.350 |

Comments